The high-yield bond indices in USD and EUR delivered in year-to-date 2025 a total return¹ of 7.8% and 4.8%, respectively. Considering current low spread levels but elevated macro risks, high-yield bonds in the upper-tier segment are considered an attractive option for buy-and-hold-investors throughout the credit cycle.

2025 was the third year in a row with a positive performance in total return, but also in excess return (above sovereign bonds). During the year, USD High Yield (HY) credit risk premiums (spreads) were more volatile compared to EUR HY as mainly the US tariff headlines in April, August and October, but also recently AI bubble and funding headlines drove spread volatility. The overall spread movement in YTD 2025 was however limited with USD HY spreads staying rather stable and EUR HY spreads slightly widening. Against the backdrop of an uncertain macroeconomic outlook and spread levels at their lows, for HY bonds, the focus is on the comparatively secure BB rating segment with a mix of selected senior secured and unsecured as well as hybrid bonds from the BBB/BBB- and B+/B categories.

Valuation: low spreads, but more attractive in yield and break-even spread

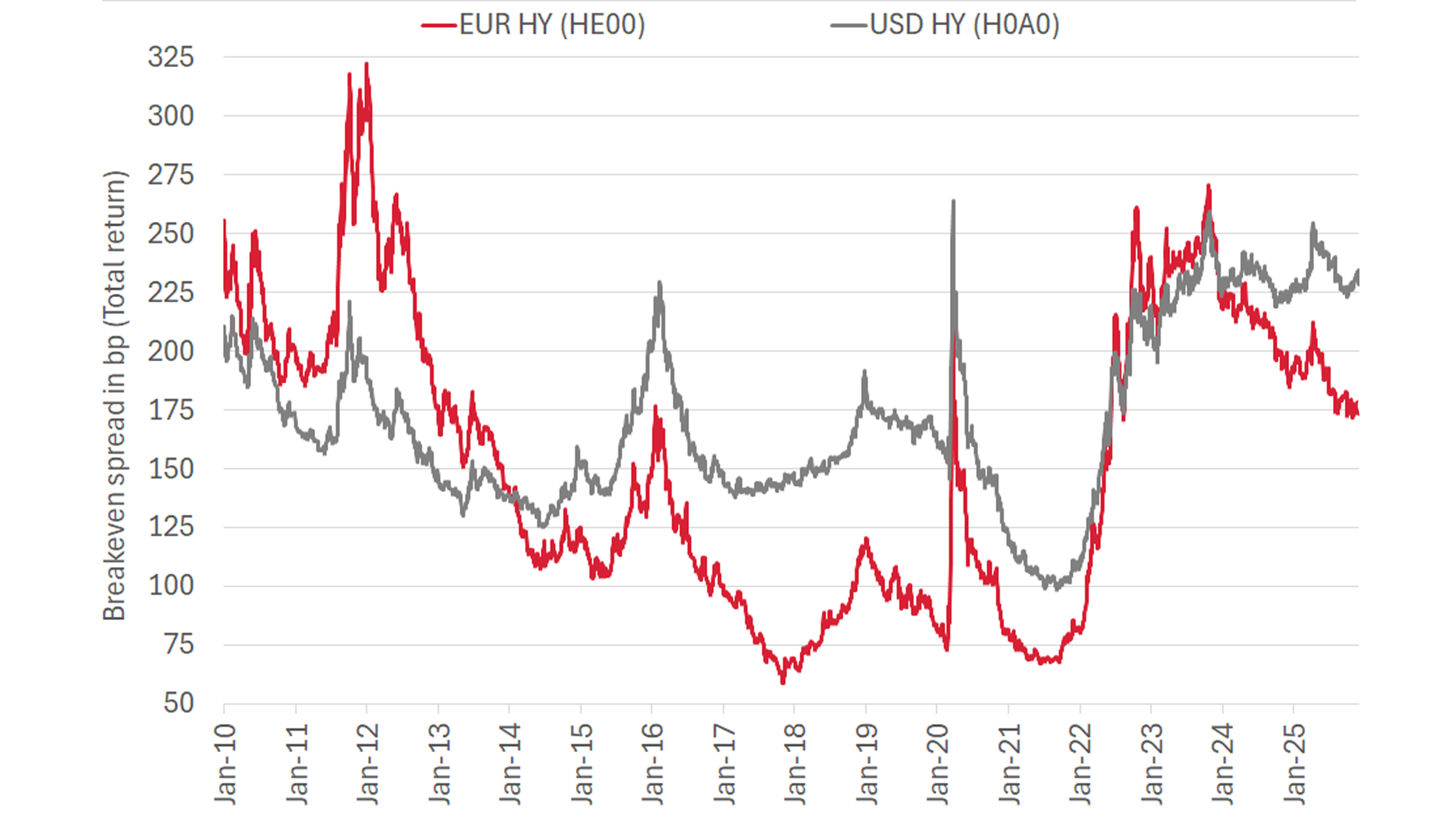

Despite some volatility in credit spreads throughout the year, the current EUR HY and USD HY index spreads are close to their lows (which are usually in the 250-300bp area). As a result, percentiles for credit spreads are in the expensive single-digit area. This is true in the BB, but also single-B categories. However, given the rates increases in 2022, yield levels are still elevated and in the 30-35%-percentile area. In YTD, the overall yield level volatility of USD HY and EUR HY was quite low and ranged in the 6.5-8.5% and 5-6%-area, respectively.

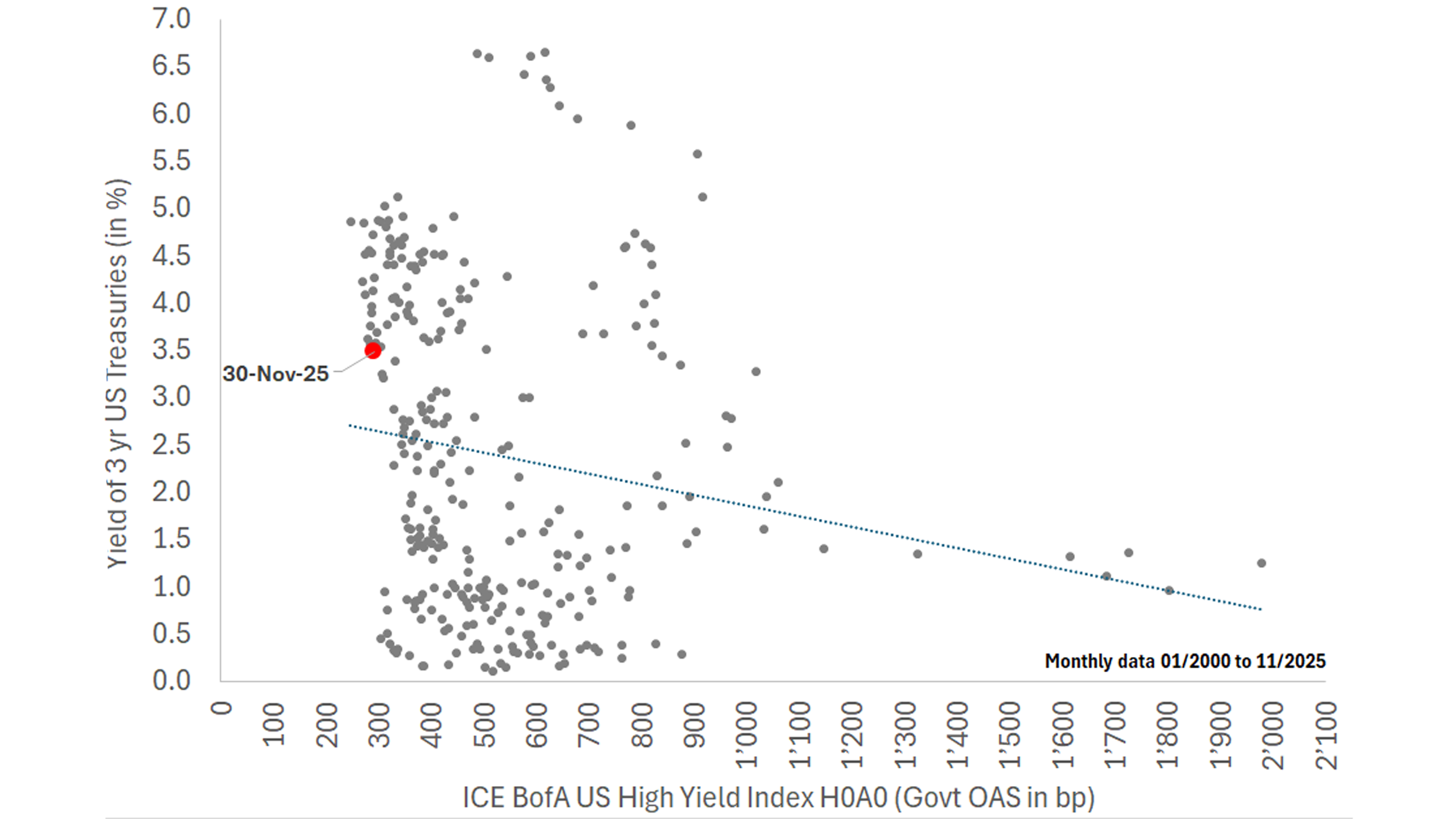

Credit spread at its lows, but break-even-spreads are above their 10-year-average providing some protection for yield volatility

Source: Bloomberg (USGG3YR/H15T3Y), ICE Index Platform (latest datapoint: 30. November 2025)

The relatively low duration (interest rate sensitivity) reduces the performance volatility of the HY asset class relative to longer-dated bonds (e.g. in investment grade or sovereign bonds) in case of changes in rates. It can be stated that the current duration of HY is below its 10-year average. As a result, the break-even-spread (i.e. effective yield divided by duration) to keep the total return positive over a 12-month investment horizon, is above its 10-year average. This measure signals a decent performance buffer against market volatilities in yields. The BB share in the EUR HY index is about 70%, and in USD HY about 55%.

Technicals: Significantly higher percentiles in credit spreads and returns

Between 2021 and 2024, demand for USD HY outstripped supply every year. Given the still elevated yield and break-even spread level, the asset class remains attractive for investors. Despite the macro volatility in the US, total supply in YTD for USD HY, i.e. gross new issuance and fallen angels still slightly more than matched the total demand (bond calls & tenders, maturities, rising stars, coupon reinvestment and mutual fund flows). In YTD, net issuance in USD HY was EUR 92bn and in EUR HY it was EUR 4bn.2

Fundamentals: Benign distress ratios and default rate outlook

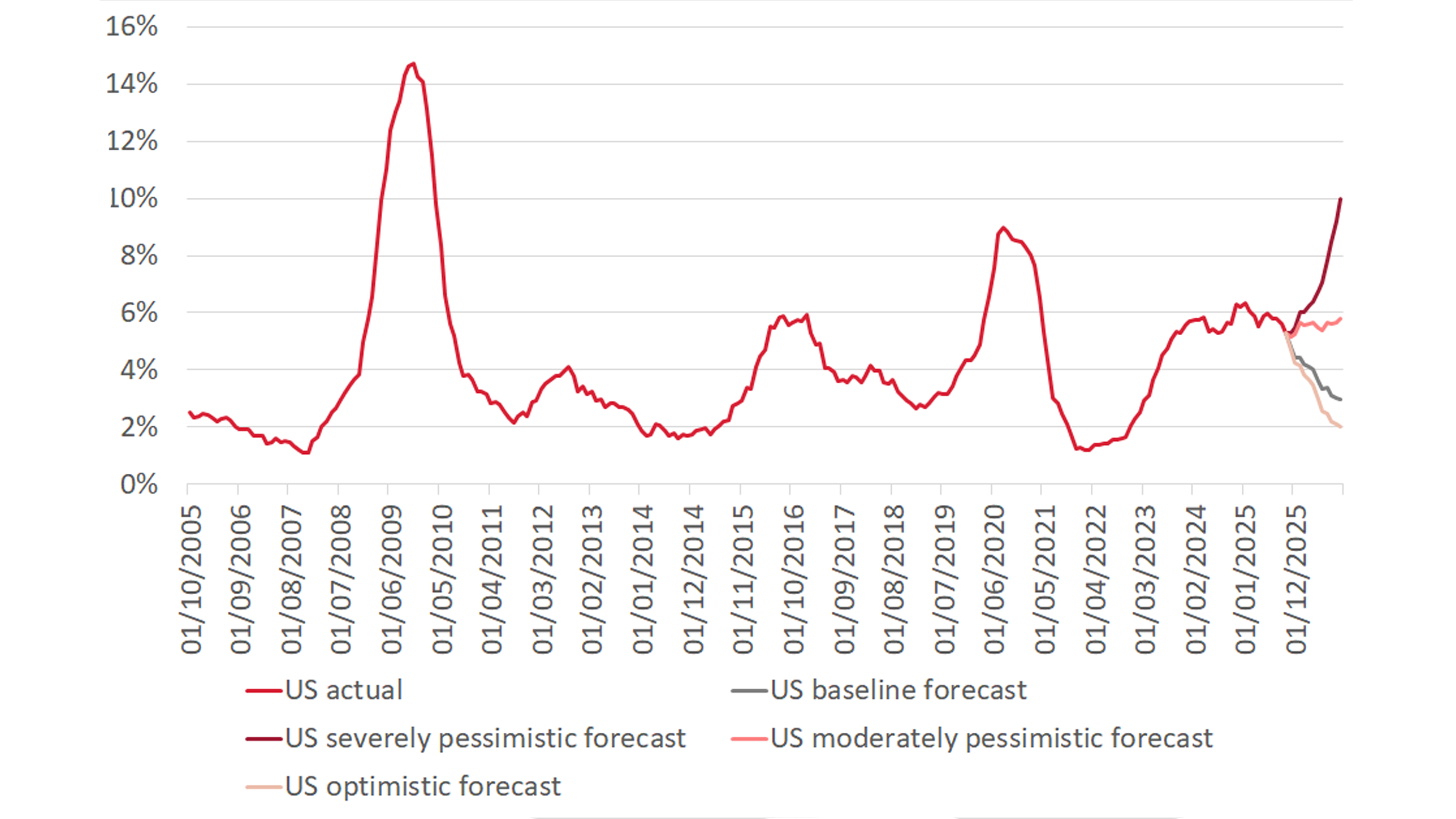

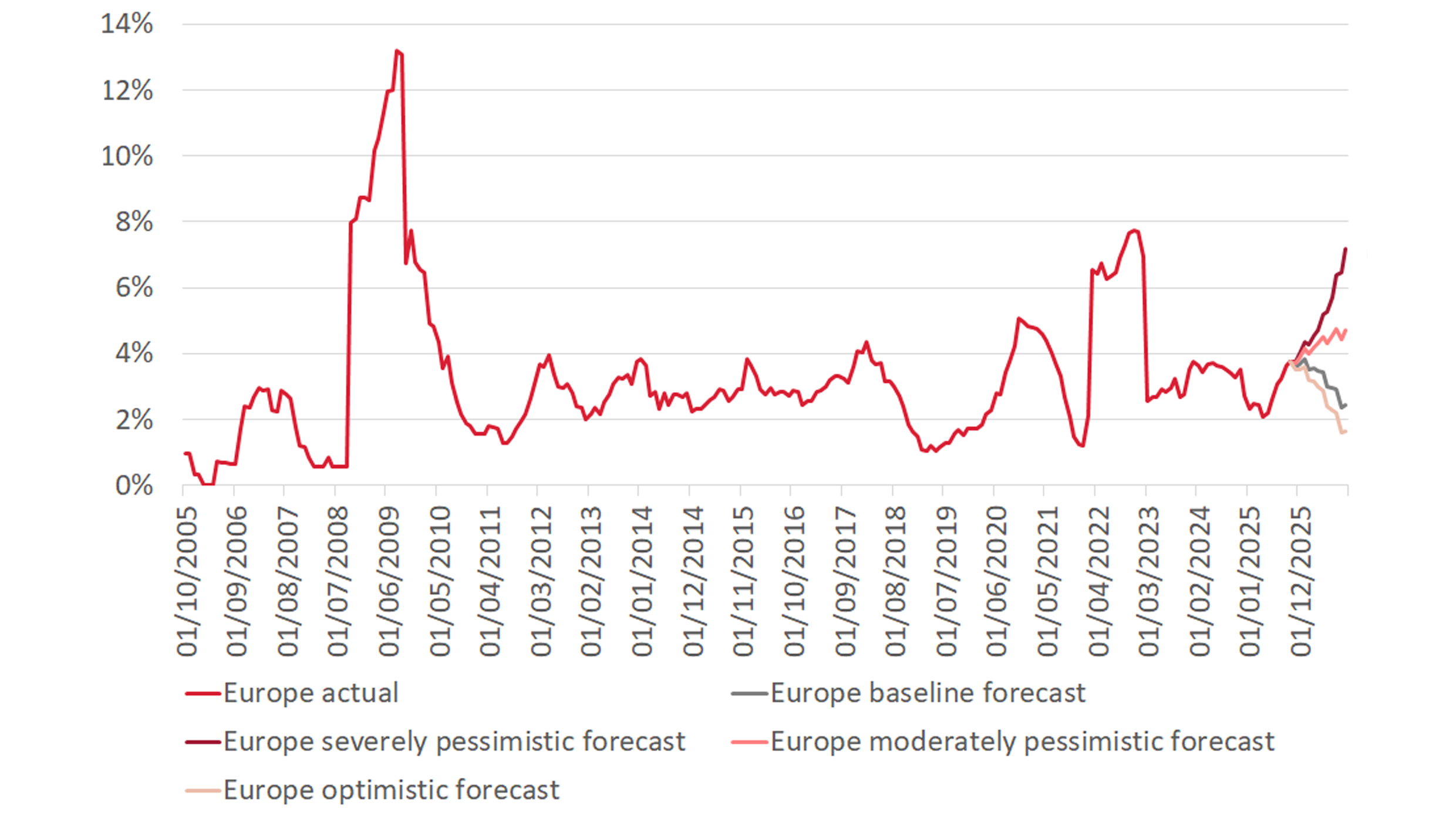

According to rating agency Moody’s, the trailing 12-month default rate ending October 2025 was 5.28% in the US, exceeding the 4.1% average of the last two decades. In Europe, the default rate stood at 3.8%, which is close to the 3.3% average over the past two decades. The latest baseline forecast by Moody’s assumes that default rates in the US will fall to 3.0% and in Europe fall to 2.4% over the next 12 months. Moreover, the 1-year recession risk probability forecast (Source: Bloomberg) remains rather modest: for the US of 30% and for the EU of 20%.

Moody’s baseline forecast for default rates until October 2026: US 3.0% and Europe 2.4%

Source: Moody’s Global October 2025 Default Report (published 15 November 2025)

The expectation of higher default rates is reflected in the increased share of distressed issuers currently traded. This metric is usually a reliable indicator of the default rate for the next 12 months. Issuers having at least one bond traded with a credit spread exceeding 1,000 basis points are distressed. On 5 November, the share in the High Yield universe was 7.7% in the US and 8.1% in Europe, respectively3. The highest concentration of distressed issuers in the USD HY segment was in the media sector; and in the EUR HY segment in the Basic Industry (including Chemicals) and Media sectors. Assuming one-third of distressed issuers default within 12 months for issuers traded as distressed, the expected default rate for USD HY is approximately 2.6% and for EUR HY is around 2.7%.

Positioning – Preference for the upper-tier high-yield segment for buy-and-hold investors through the credit cycle

Uncertainties surrounding US tariff policies, the US job market, the impact of a K-shaped economy in the US, the outlook for AI/Data Centre capex and funding surge, the private credit market outlook and exposures, low real GDP growth outlook in the Eurozone and investment plans and budget constraints as well as (geo-)political risks, are likely to lead to continued volatility in credit risk premiums and interest rates. In the absence of rising recession risk probabilities, central bank monetary policy should have a supportive effect on risky assets like HY. The market currently expects the Fed to cut its rate several times going forward. This scenario is generally positive for high-yield bonds because: First, fixed-coupon bond prices can benefit from falling interest rates; second, companies and consumers (with a high proportion of variable debt) benefit from a lower interest expense; and third, low reduced rates tend to stimulate economic growth over time.

Against this backdrop of risk factors and spread levels at their lows, Swiss Life Asset Managers continues to favour the high-quality upper-tier segment for high yield bonds and focuses on the comparatively secure BB rating segment with a mix of selected senior secured and unsecured as well as hybrid bonds from the BBB/BBB- and B+/B categories. Swiss Life Asset Managers continues to favour the high-quality hybrid bonds issued by investment grade-rated companies, which are viewed as solid components of HY portfolios. They account for almost 30% of the BB index (in EUR). In addition, Swiss Life Managers enhances upper-tier high-yield strategy in USD and EUR bonds with selected attractively priced bonds from the BBB rating category. Swiss Life Managers prefers BBs and Bs in EUR, as they generally offer higher spreads versus government bonds compared to their USD counterparts.

The benchmark of our upper-tier high-yield strategy (75% BB/25% B and 50% USD/EUR, in USD currency) is currently trading at a yield to maturity of 5.1% (in USD) and generated a total return of 7.6% (in USD) in Ytd. This performance exceeds that of the EUR HY indices (in USD). In addition, single-B’s and CCC’s underperformed in YTD 2025 compared to BB’s in terms of total return. This upper tier HY segment generates higher carry compared to investment-grade indices in times of rather stable earnings environment with limited spread and yield volatility but also offers a lower return volatility, stronger average ratings, and potential outperformance versus broader High-Yield indices in case spreads should widen from their current low levels. Solid risk management, active security selection, and careful credit analysis are essential components for alpha generation above our upper tier HY benchmark, especially in volatile times.

1 In local currency

2 Source:Goldman Sachs 14 November 2025

3 Source: CreditSights

Further information on hybrid bonds

Hybrid bonds as solid components of high-yield portfolios

Hybrid bonds from stable issuers with good credit ratings in the industrial and financial sectors that themselves have an investment grade rating and therefore a comparatively low default probability with higher returns are suitable for risk-conscious investors with a longer investment horizon.

Swiss Life Asset Managers is a leading asset manager and provider of bond funds – assuming strategic responsibility and ensuring sustainable performance.