Hybrid bonds from stable issuers with good credit ratings in the industrial and financial sectors that themselves have an investment grade rating and therefore a comparatively low default probability with higher returns are suitable for risk-conscious investors with a longer investment horizon.

Corporate hybrids are equity-like bonds with a fixed coupon and usually have a very long term or no maturity at all. Corporate hybrids are subordinated in the event of insolvency and the agreed coupon payments may be suspended or deferred under certain conditions (coupon deferral risk). Due to their subordinate status, hybrids typically receive a rating two grades lower than the issuer’s senior bonds.

At rating agencies, hybrid bonds are usually classified pro rata as 50% equity and 50% debt when calculating key credit figures. They are reported as equity in the issuer's balance sheet, depending on their configuration. The bonds may also be redeemed early by the issuing company on a predetermined date, often after five years at the earliest. If the bond is not redeemed on this date (“extension risk”), its interest is recalculated using the money market rate applicable at the time, plus a risk premium determined at the time of issue. If the hybrid bond is not redeemed on the stipulated date, it will also no longer count as 50% equity in the calculation of the key credit figures at the S&P rating agency.

Hybrid bonds issued by banks and insurance companies

Banks and insurance companies also issue hybrid bonds, including what are known as Tier 2 bonds, to improve their regulatory capital ratios, rating assessments and balance sheet capital structure. These hybrid bonds are also subordinated. In contrast to corporate hybrids, Tier 2 bonds issued by banks in the EU are not subject to discretionary coupon suspension. Tier 2 bonds can usually be redeemed five years prior to maturity. If they are not redeemed, their regulatory recognition as equity is gradually reduced. In addition, there may be a conversion into equity instruments or a partial or full write-down of the par value if the issuing bank is considered to be at risk of insolvency by the supervisory authorities (“point of non-viability”) or in the event of burden-sharing, i.e. extraordinary support from the public authorities.

Strong growth of asset class and holdings in high-yield indices

From the point of view of issuers, the advantage of hybrid bonds lies on the one hand in the optimisation of capital costs compared to the issuance of equities, and on the other in avoiding the dilution of the shares of existing shareholders or partners. On the investor side, subordinated hybrid bonds are attractive because they are traded with the same default probability, but currently with an approx. 2% higher credit spread than comparable senior corporate bonds. However, it should be borne in mind that this is also associated with higher credit spread volatility.

Over the past decade, the global hybrid bond market (in USD, EUR and GBP; including investment grade bonds) has grown significantly, to a current total outstanding amount of around EUR 900 bn.

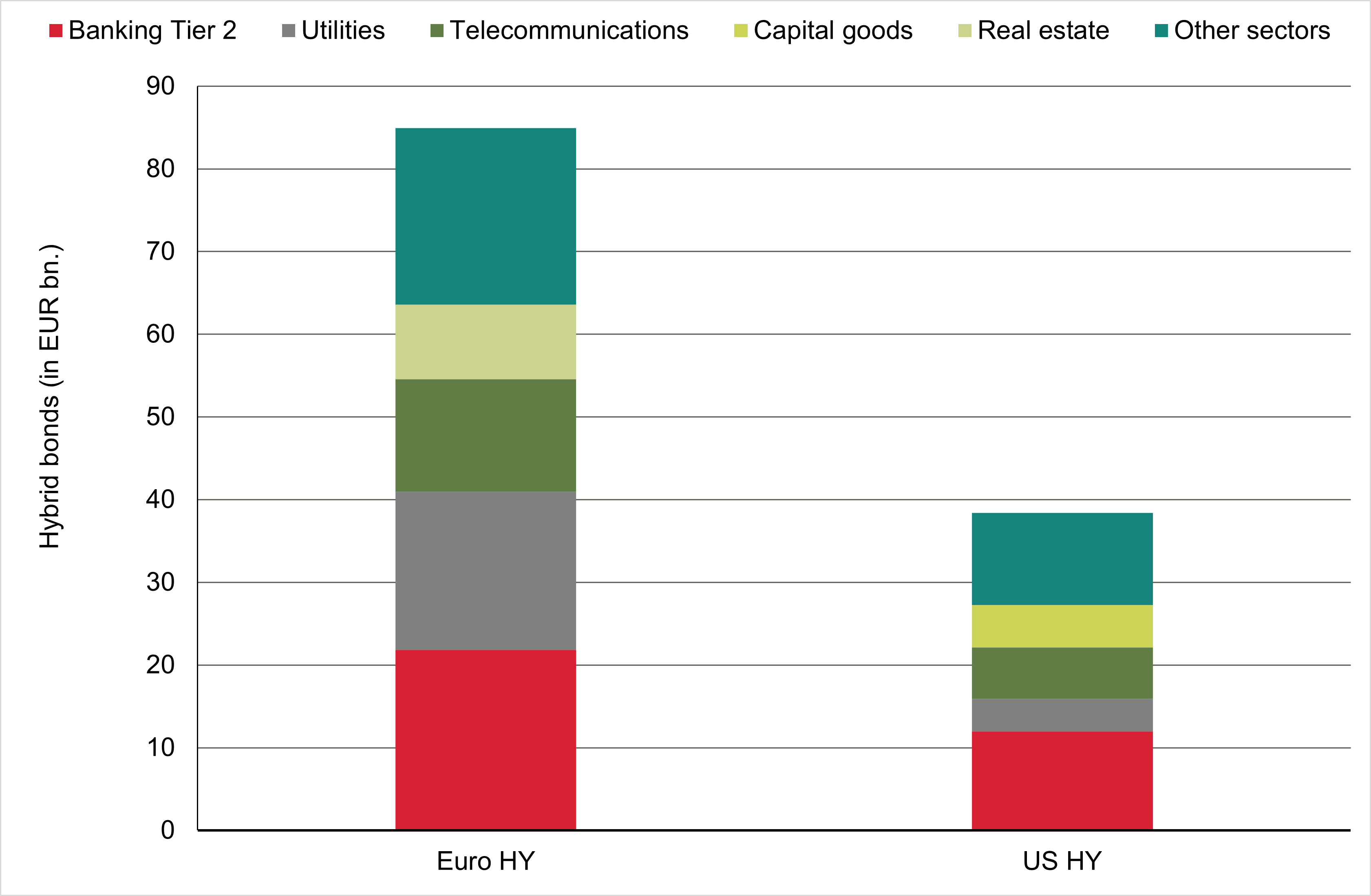

Hybrid bonds in high-yield indices in EUR and USD

Source: Bloomberg data, ICE BofA Indices HE00 and H0A0

Around 20% of the euro-denominated high-yield bond market, i.e. bonds below investment grade, is composed of hybrid bonds. The most important sectors are banks (Tier 2), real estate, telecoms and other utilities, although hybrid bonds issued by companies from other sectors have also increasingly contributed to diversification in recent years. The share of hybrid bonds in the European high-yield market is significantly higher than in the US, where it is only around 3%. Most of the high-yield hybrid bonds are rated BB by the rating agencies.

Hybrid bonds as a key component of high-yield portfolios

Given the heightened uncertainties in the credit market and presumably a further rise in default rates, together with the volatility in interest rates and credit risk premiums, we continue to favour the comparatively safe BBs in the high-yield bond segment, namely those in euros. The current yield of BBs is 7.9% in USD and 6.6% in EUR. We also favour BBs in EUR because their credit risk premium (vs. government bonds) is around 0.7% higher than BBs in USD. In addition, the credit risk premium of BBs in EUR – as opposed to BBs in USD – is currently around 0.6% above its ten-year average. Hybrid bonds represent almost 30% of the BB index in EUR.

The careful selection of sectors and companies is crucial when investing in hybrid bonds. Equally important are the analysis of the documentation for the bonds and the valuation of the differences between subordinated and senior bonds. We consider high-yield hybrid bonds from strong, stable issuers with investment grade rating to be an integral part of high-yield portfolios. From a credit perspective, the main advantages include the very low default probability of the well-known issuers, as they predominantly have an investment grade rating, have known capital structures and credit histories, and are primarily from more defensive sectors. Moreover, cases of extension risk and coupon deferral risk have so far been very rare for corporate hybrids from issuers with investment grade rating.