With emerging market economies on track to represent 60% of global GDP this year, a shift is on its way to reshape the world of fixed income. Emerging Markets Investment Grade (EM IG) credit has evolved into a resilient, high-quality asset class built on stronger fundamentals and greater diversification than ever before — a segment, investors can no longer afford to ignore.

Emerging market (EM) credit has demonstrated exceptional performance since 2023, leading the way for the broader EM asset class. EM equities and local currency debt have subsequently caught up in 2025, supported by an increasingly favourable macro environment characterised by:

- Lower US Treasury yields providing a favourable backdrop for EM assets

- Weakening USD reducing pressure on EM external financing

- Fading US exceptionalism narrative creating space for EM differentiation

This environment represents a continuation of broader structural themes that have supported EM as an asset class, while investors have become increasingly sophisticated in their approach to EM fundamentals and asset class selection. Beneath this short-term strength lies a deeper structural evolution that is reshaping the role of EM within the global fixed income markets.

EM Fixed Income is becoming impossible to ignore

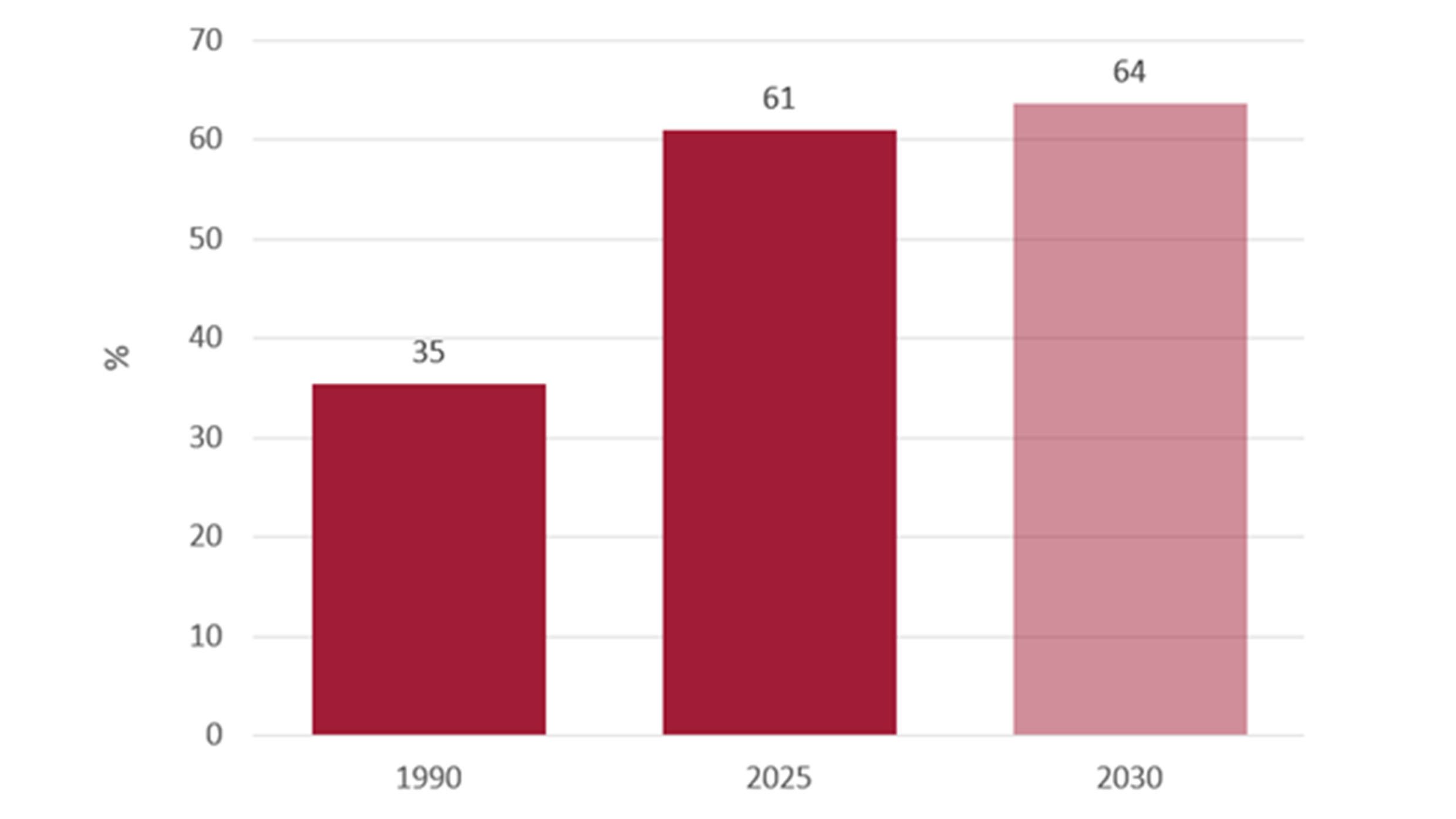

A key structural driver of this shift is the dramatic expansion of EM credit. EM economies are projected to constitute nearly 60% of global GDP by this year, 2026, versus approximately 20% three decades ago. This economic weight is increasingly reflected in fixed income markets, where the EM asset class has grown significantly in both absolute size and relative importance within global bond allocation.

Emerging markets are on the verge of reaching a 60% share of global GDP

Source: Macrobond, Swiss Life Asset Managers; Based on Purchasing Power Parity (PPP) and incl. IMF forecast data for 2030

At the same time, the composition of EM debt highlights the growing significance of hard currency debt. Today, total EM fixed income stands at USD 28.8 trillion, with USD 4.3 trillion in hard‑currency sovereign and corporate debt — a market now larger than the Euro corporate bond market and nearly three times the size of US high-yield. Around 60% of this hard‑currency universe is investment grade, underscoring the depth, maturity, and investability of EM IG bonds. For global investors, EM IG credit is no longer an alternative allocation — it is a systemically important part of global fixed income markets.

EMs show fundamental strength like never before

The resilience of EM fundamentals remains the cornerstone of our positive view. EM debt has outperformed developed market credit on a cumulative basis since 2020, demonstrating remarkable resilience through multiple stress events including COVID-19, the Russia-Ukraine conflict, Middle East geopolitical tensions, and China's real estate crisis.

This outperformance has been particularly pronounced since 2023, with hard currency EM debt — both corporate and sovereign — significantly outpacing global developed market corporate debt while delivering superior risk-adjusted returns. This track record validates the structural improvements in EM credit quality and underscores the asset class's ability to perform through varying market conditions.

A significant development underpinning our positive view has been the broad-based improvement in credit quality across both EM sovereigns and corporates. This trend is clearly visible in rating agency actions, which have shown a decisive shift since 2023. Upgrades represented 56% of all rating actions in 2023, up sharply from just 38% in 2022, and this positive momentum has accelerated further with upgrades accounting for over 60% of rating actions in 2025. This inflection point marks a fundamental shift in the credit trajectory of EM issuers.

Structural strength behind Sovereign Credit

The improvement in sovereign credit quality has been underpinned by tangible fiscal and monetary discipline across EM economies. This is not merely a cyclical phenomenon but reflects deeper structural reforms, strengthened institutional frameworks, and more prudent macroeconomic policy management.

Many EM sovereigns have built stronger fiscal buffers, enhanced monetary policy credibility, and implemented reforms that have fundamentally improved their resilience to external shocks.

EM IG Corporates pull ahead

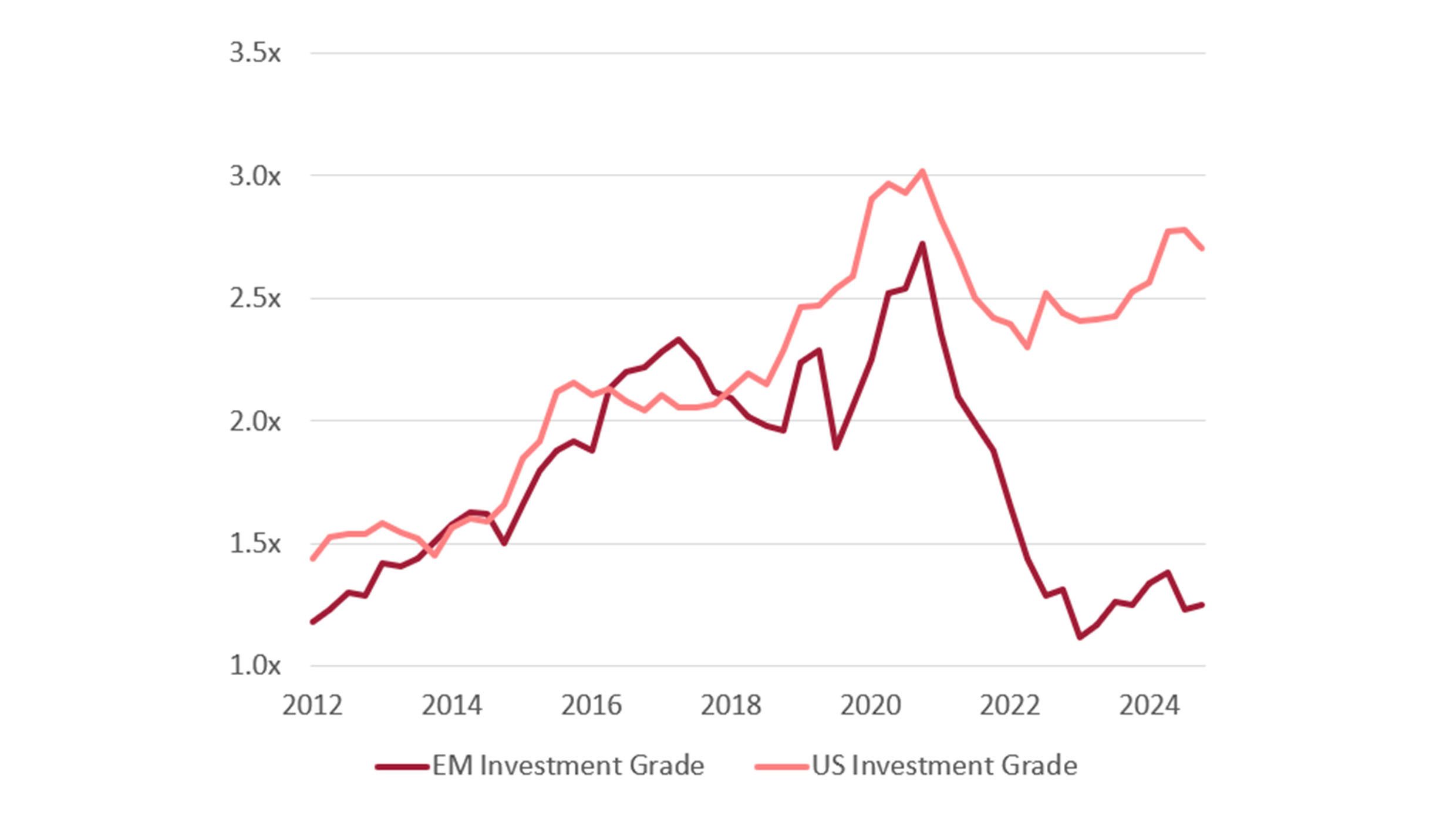

EM IG corporate issuers have demonstrated even more pronounced credit quality improvements, particularly when compared to their developed market counterparts. Since 2013, EM IG corporate leverage ratios have improved markedly, while developed market corporate leverage has deteriorated over the same period — creating a particularly striking divergence.

The leverage ratio of EM IG corporate bonds has fallen significantly since 2013

Source: BofA, Swiss Life Asset Managers; Data as of 30.6.2025; Net leverage – Net debt / EBITDA last 12 months

Today, EM IG corporate issuers consistently demonstrate lower leverage ratios compared to developed market peers. This corporate deleveraging trend, combined with generally stronger cash flow generation, has created a compelling credit profile that increasingly rivals or surpasses many developed market corporates.

Reassessing EM risk: valuation convergence and changing market perceptions

Valuations have tightened considerably in recent years, reflecting the strong performance of EM credit. However, all-in yields remain attractive to offer compelling income opportunities. We see the compression in EM credit spreads not as a technical rally but as a fundamental convergence toward developed market credit, supported by broad-based improvements in EM sovereign and corporate quality.

This convergence is unfolding while developed markets face rising political instability, fiscal de-anchoring, and weakening institutional frameworks – factors that challenge the traditional EM vs. DM risk hierarchy.

As perceptions of developed market stability are being reassessed, the relative appeal of EM IG credit strengthens, providing investors with a high‑quality, yield‑enhancing alternative whose risk‑adjusted profile increasingly rivals that of DM credit.

Key risks to monitor

While we maintain a constructive view on EM IG credit, we recognise potential downside scenarios that could pressure the asset class. Potential risks include a stagflation environment and a global recession that would create headwinds across risk assets and pressure weaker credits through deteriorating cash flows.

However, in both scenarios, we expect EM IG bonds to demonstrate relative resilience given sounder fundamentals, stronger balance sheets, and lower leverage ratios versus developed market peers. The structural improvements documented throughout this note position the asset class to weather adverse conditions more effectively than in prior cycles, reinforcing the importance of maintaining a quality focus within EM credit allocations.