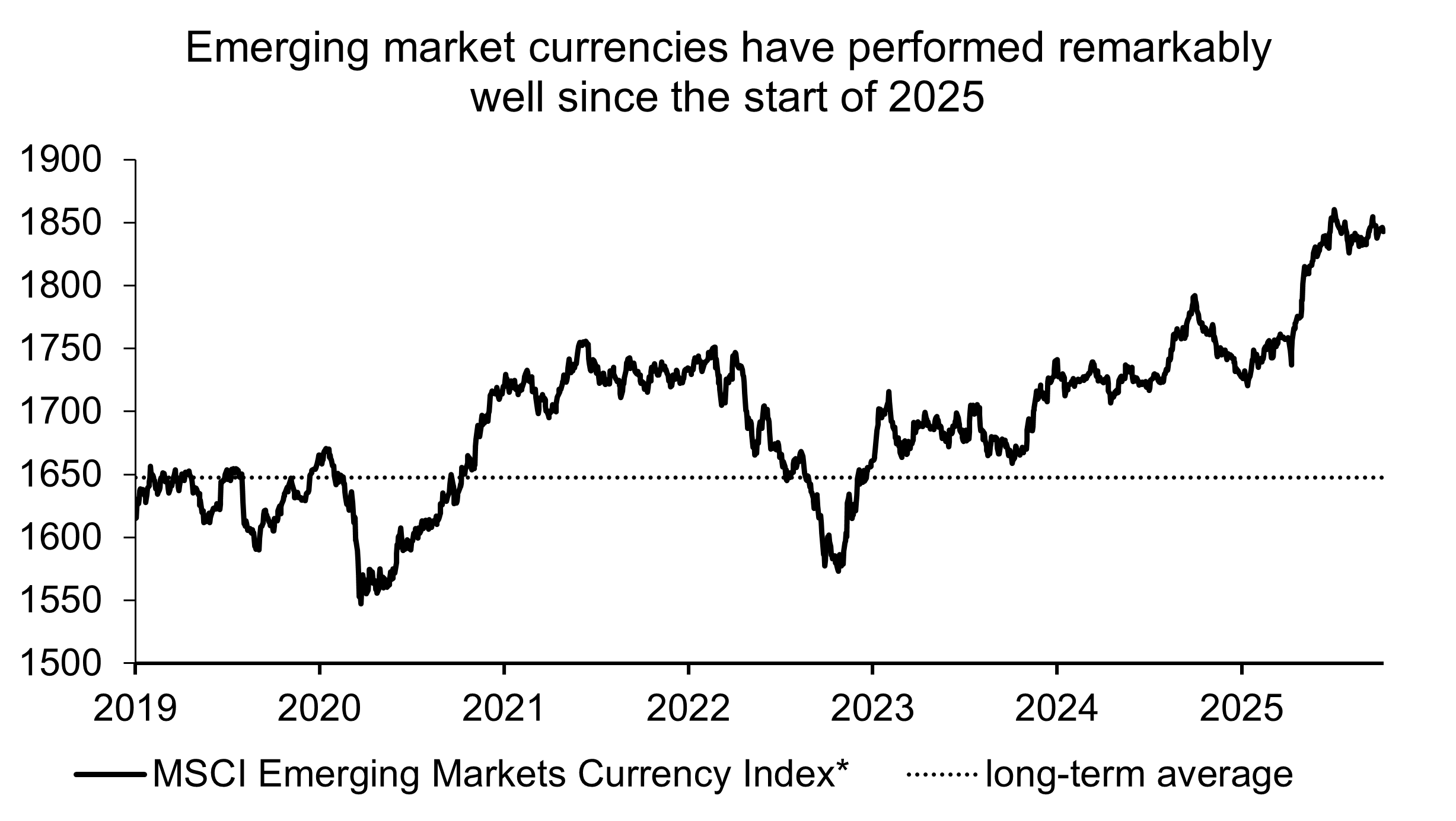

Emerging market currencies have posted strong gains since the beginning of the year, driven by efforts to diversify away from US assets.

In a difficult economic and political environment, emerging markets are showing remarkable resilience — and several factors suggest that this momentum is likely to continue.

First, on the tariff front, most emerging economies have been spared the harshest measures. Countries such as South Korea, Vietnam, Indonesia, the Philippines, Malaysia, and Thailand have negotiated agreements with the United States, reducing the tariffs announced on 2 April. These economies now face duties ranging from 10% to 20%, levels that are generally manageable. Brazil and India have been less fortunate, with rates of 50%. However, Brazil secured exemptions on a large portion of its exports, limiting the economic impact. India, penalised for its imports of Russian oil, faces significantly higher tariffs than its Asian peers, calling into question the potential benefits it could have had of the “China+1” strategy. However, signs of rapprochement between India and China are emerging, which could offset the effects of US tariffs through renewed investment and productivity gains.

Second, the Chinese economy is demonstrating strong resilience. As of August, Chinese exports have increased by 5.9% year-to-date compared to the previous year, despite US tariffs exceeding 40%. The manufacturing sector remains robust, illustrating the country’s successful transition toward technology-driven growth. China is now a global leader in electric vehicles, solar panels and batteries, and holds over 50% of the global market share in chemicals, shipbuilding, industrial robotics, drones and biotechnology.

Third, despite pressure on external demand, domestic demand remains strong. Falling inflation is boosting purchasing power and giving central banks room to ease monetary policy, supporting investments. Emerging market currencies, which have appreciated as part of a diversification away from the dollar, along with the influx of low-cost Chinese goods, should help keep inflation under control.

Finally, in the context of asset diversification away from the United States, emerging markets are seen as an attractive investment opportunity. This is reflected in persistent flows into the asset class and bond spreads tightening to their lowest levels of the year. While valuations appear stretched, a solid macroeconomic backdrop, a weak dollar and strong demand remain supportive factors.

* Measures the total return of a basket of emerging market currencies against the dollar, weighted according to the MSCI EM Equity Index. Includes currency fluctuations and local interest rates.

Sources: Macrobond, Swiss Life Asset Managers. Last data point: 10.10.2025

Further information on Emerging Markets

Perspectives Emerging Markets

Perspectives Emerging Markets offers quarterly updates from our research team, providing in-depth analysis of economic developments, market trends, and investment opportunities in emerging economies.