The EUR and USD high-yield bond indices posted a significantly positive performance in 2023 with a return of more than 12% and a return of more than 8% in 2024. After a successful start to 2025, the tide changed in April. Nevertheless, there are good reasons to continue investing in high-yield bonds in the upper-tier segment.

Currently1 the performance for high-yield bonds (HY) is a positive 1.0% for EUR-HY and 1.4% for USD-HY.2 Moreover, due to the significant rise in credit spreads in March and April, valuation levels now look somewhat more interesting than at the beginning of the year. Percentiles for returns, but now also for credit risk premiums (credit spreads), have risen to around 30 and 20%, respectively. Against the backdrop of an uncertain macroeconomic outlook, for HY bonds we continue to focus on the comparatively secure BB rating segment with a mix of selected bonds from the B+/B and BBB categories.

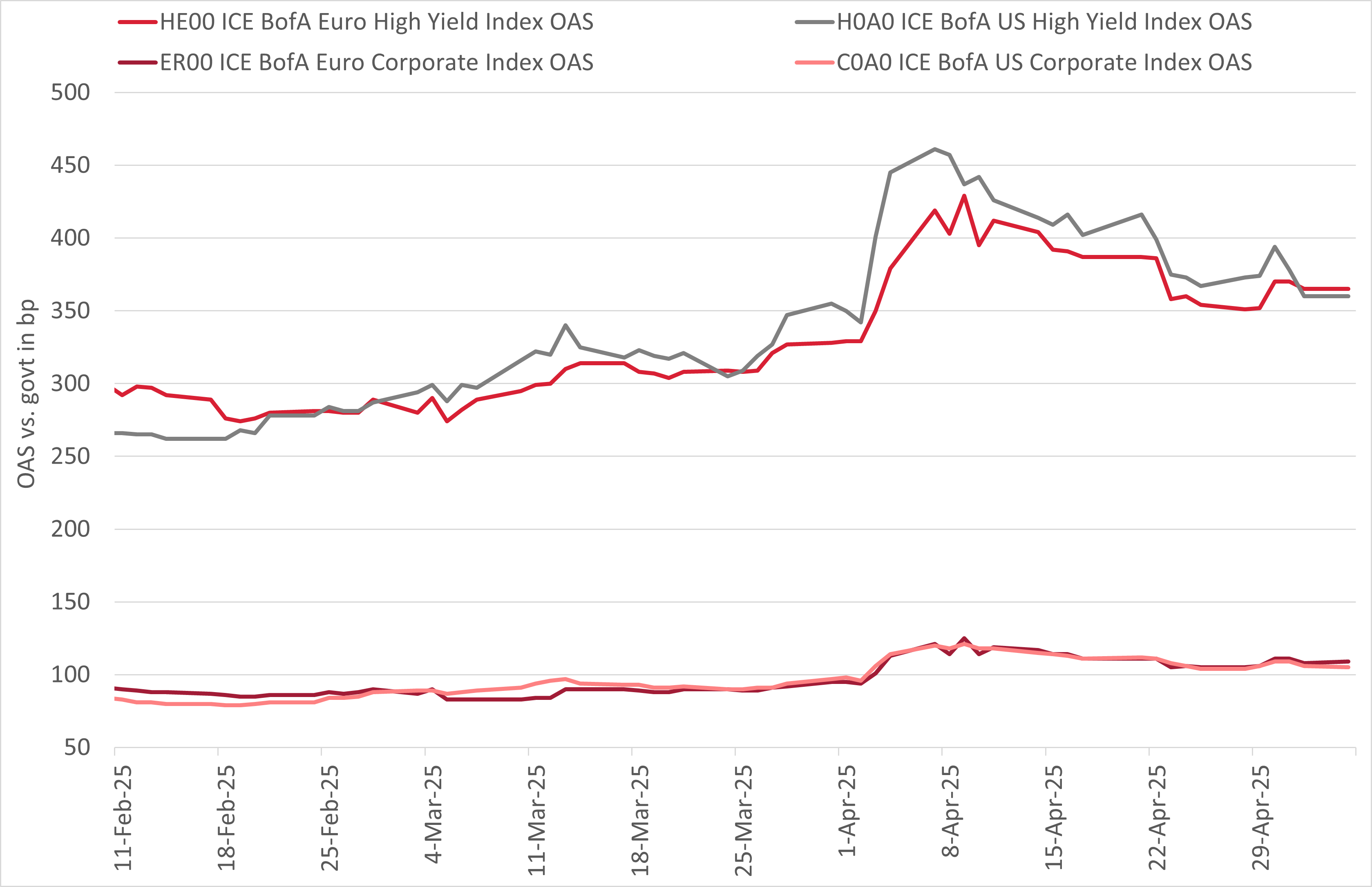

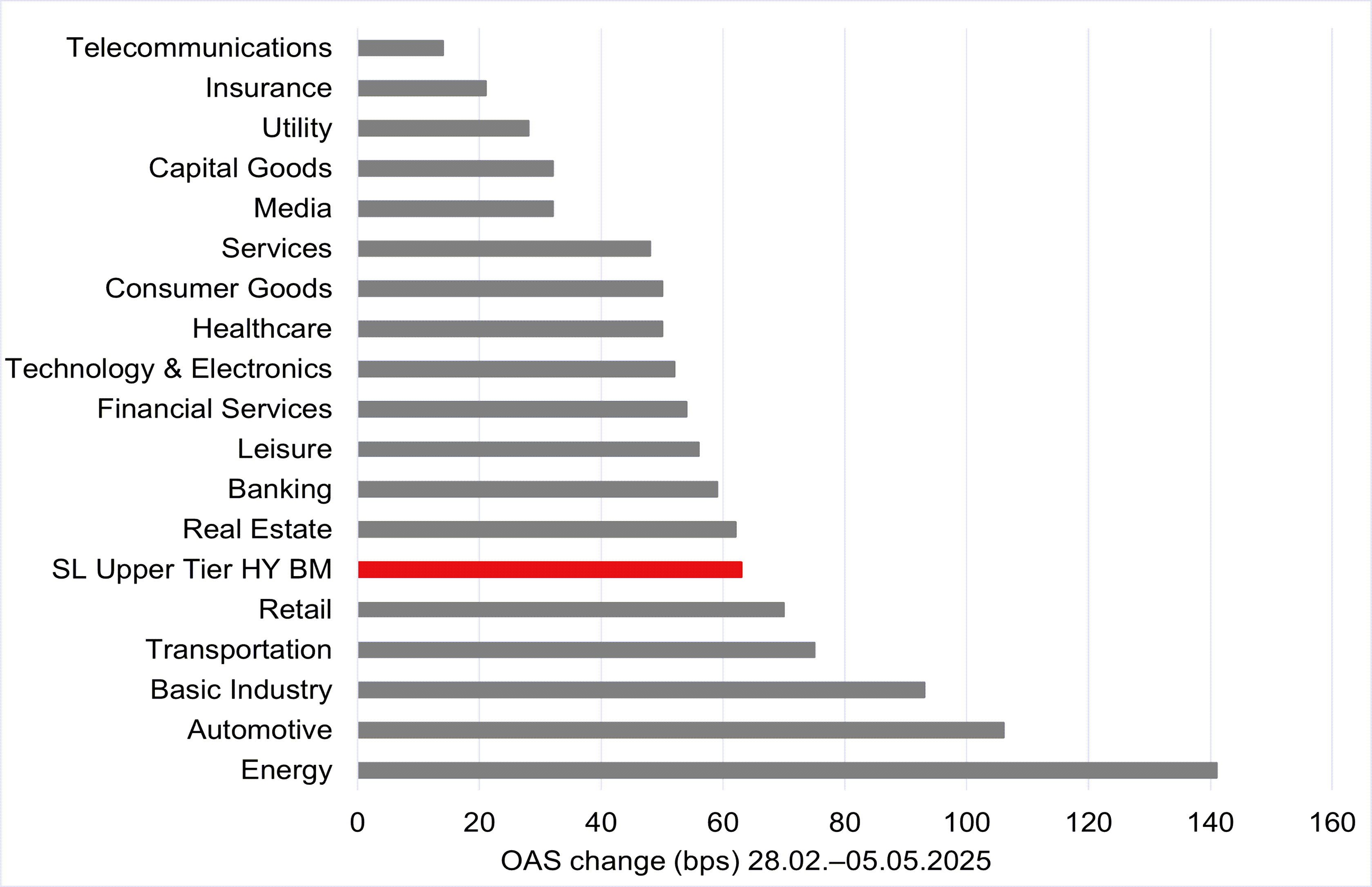

Spread increase due to US tariffs policy

In recent months, the US has imposed import tariffs on almost all countries and on selected sectors such as steel, aluminium or automotive. Some countries responded with counter-tariffs. This has led to expectations of lower growth, higher inflation and an increased probability of recession, especially in the US. This in turn led to a significant increase in credit spreads in this quarter, with spreads widening initially more sharply for USD HY than for EUR HY. Since March, as expected, our benchmark for the upper-tier high-yield segment has seen a stronger widening of spreads in cyclical sectors such as energy, automotive and basic industries as well as in lower credit qualities (B and CCC ratings). On the other hand, BB ratings and defensive sectors such as telecoms, insurance or utilities saw a lesser widening of spreads.

Spread widening after “Liberation Day” on 2 April, especially in cyclical HY sectors

Source: ICE; Note: “Upper Tier High Yield” benchmark mix: 75% BB / 25% B; 50% USD / 50% EUR

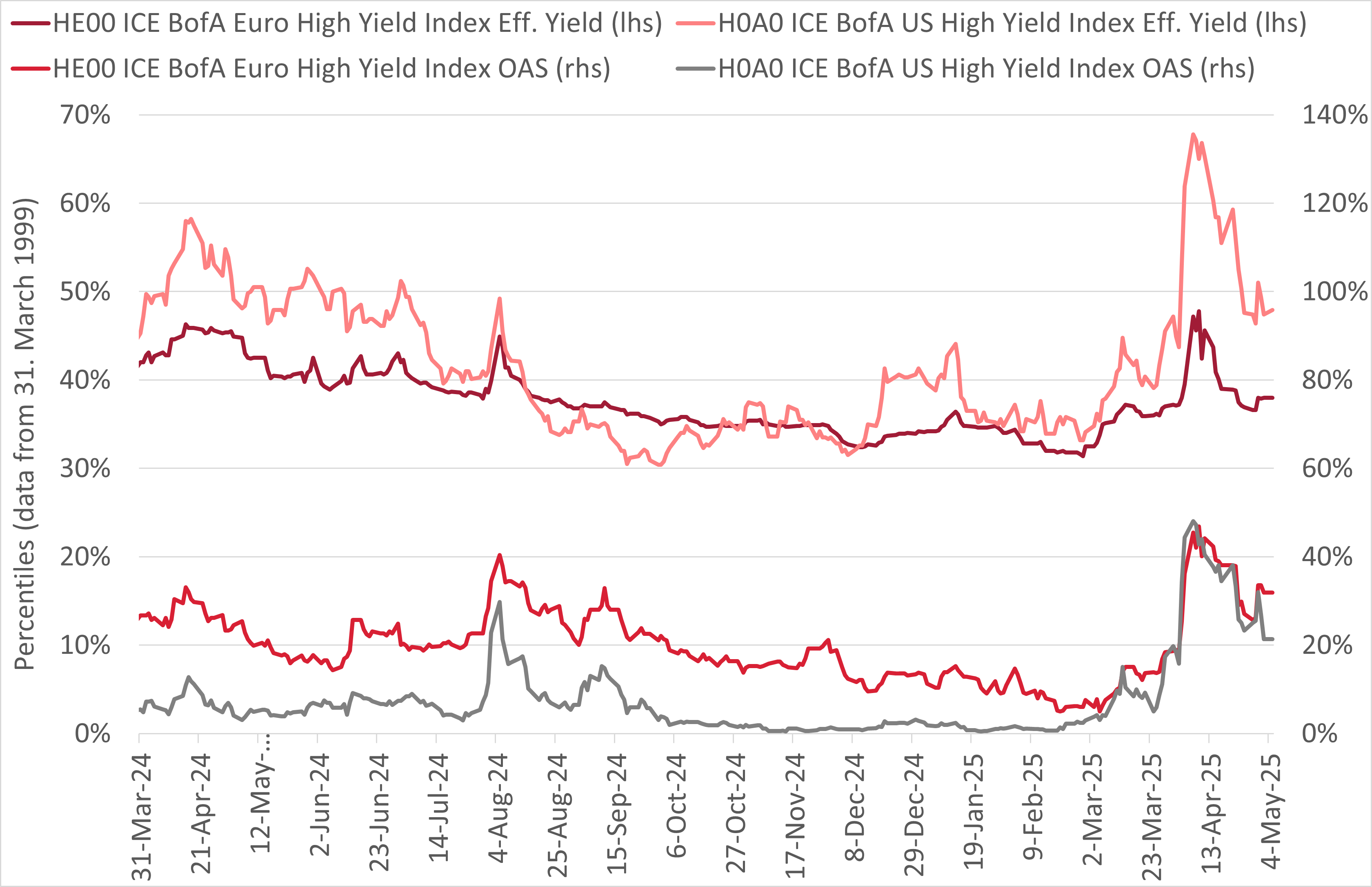

Significantly higher percentiles in credit spreads and returns

Spreads were very tight before they moved higher, especially on USD HY. Before March, the percentiles have been in the overvalued range of 10–15% for EUR HY and as low as 5% for USD HY. The level on credit spread percentiles increased to between 20 and 30% for USD HY and EUR HY, respectively. This makes this asset class more attractive again. By contrast, the percentiles for returns3 have been around 40% for some time now due to the rise in interest rates. With the increase in credit spreads, the 26-year percentile for yields on USD HY has even risen to 50% while the level on EUR HY has remained stable at approximately 40%.

Significant increase in credit spread percentiles (left) – Yield percentiles at elevated level (right)

Source: ICE

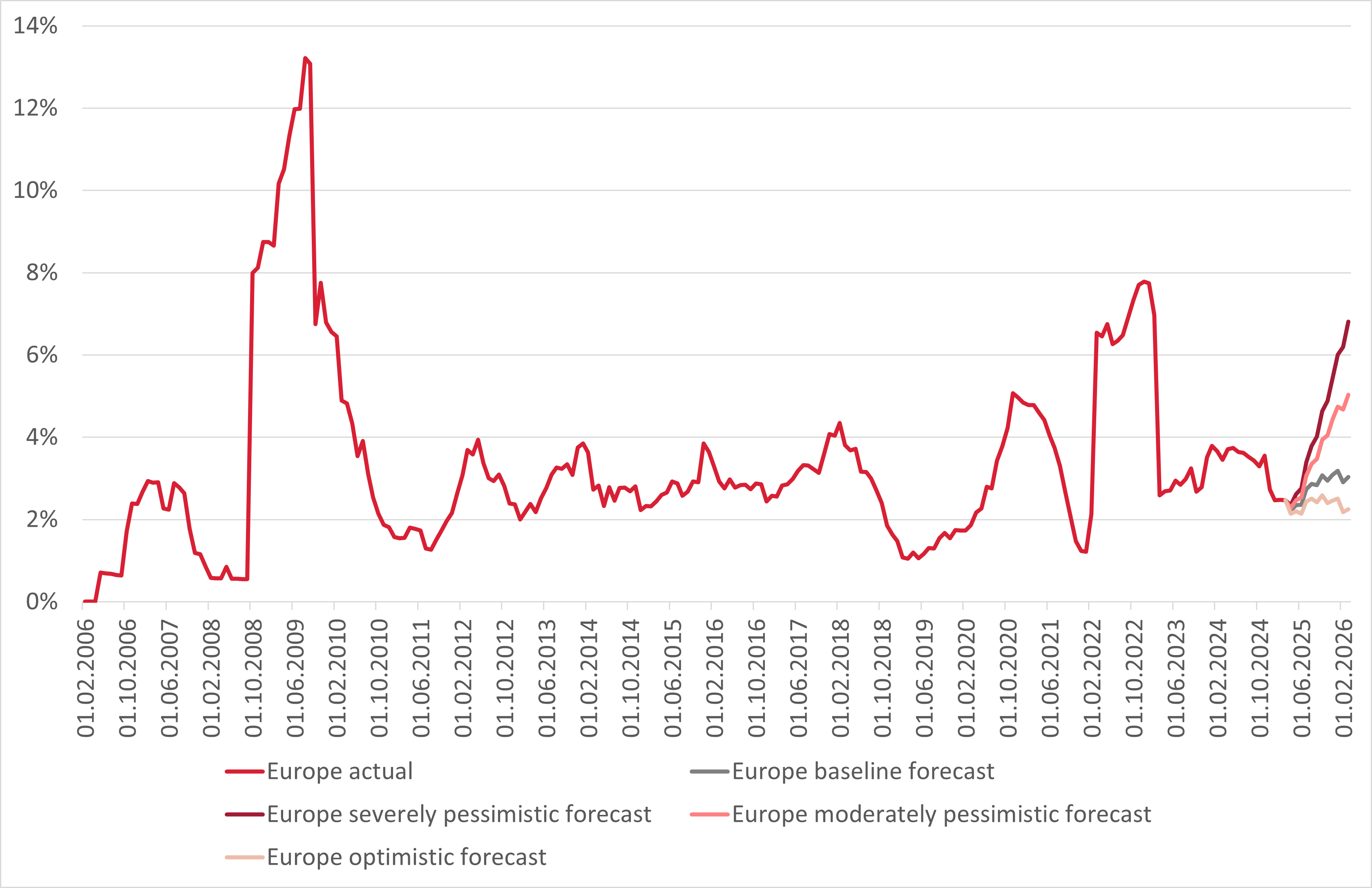

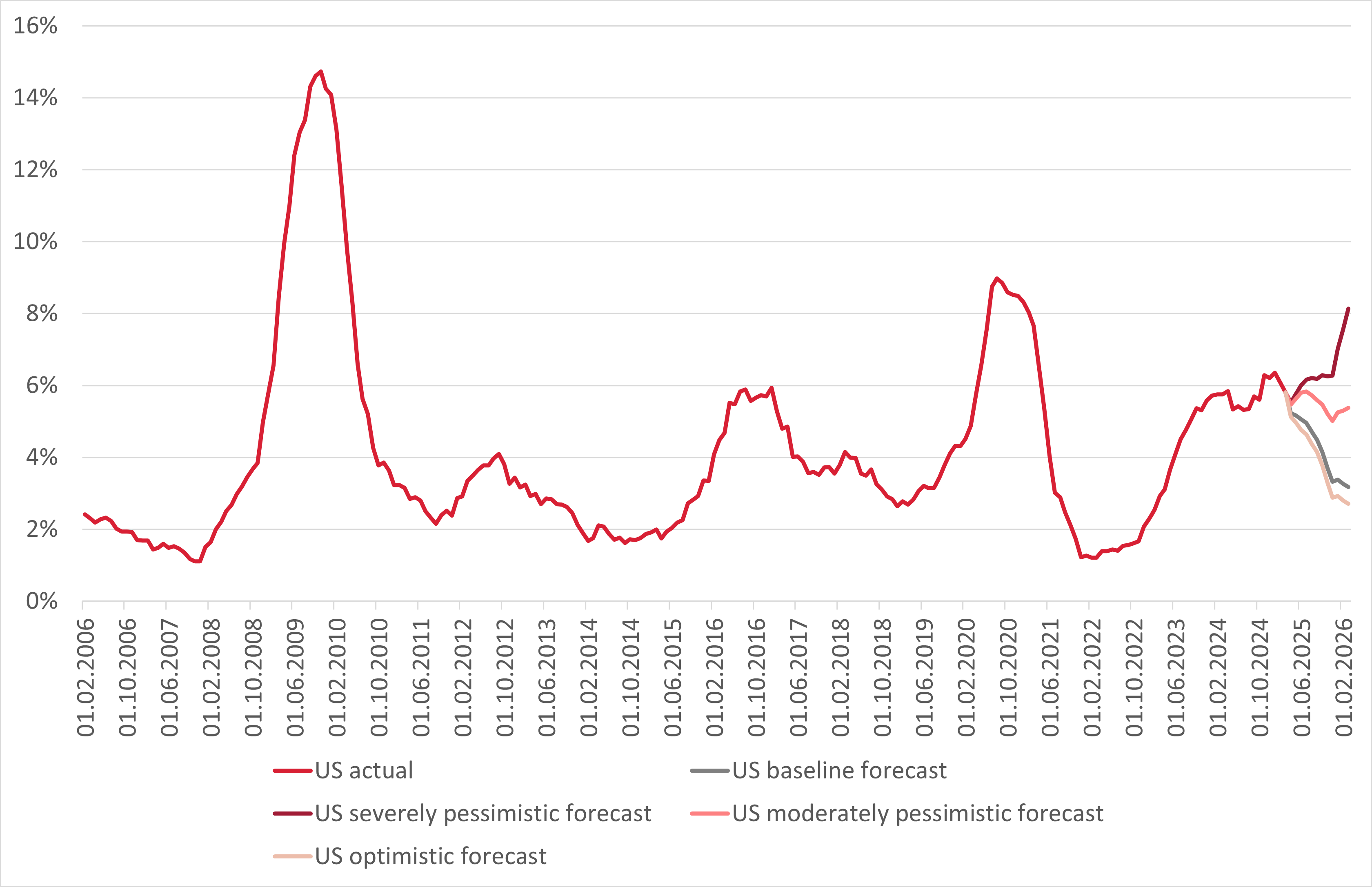

Rising default rates and higher credit spreads

According to the rating agency Moody’s, the current 12-month default rate is 5.8% in the US, which is still above the 4.1% average of the last two decades. In Europe, the default rate was 2.5%, which is below the 3.3% average over the past two decades. The latest baseline forecast by Moody’s (16 April 2025) assumes that default rates in the US will fall to 3.2% over the next 12 months and rise to 3.0% in Europe.

Moody’s baseline forecast for default rates until March 2026: US 3.2% and Europe 3.0%

Source: Moody’s Global March 2025 Default Report (published on 16 April 2025)

The expectation of higher default rates is reflected in the higher share of distressed issuers currently traded. This metric is usually a good indicator of the default rate for the next 12 months. Issuers having at least one bond traded with a credit spread of more than 1000 basis points are considered to be distressed. On 5 May, the share in the high yield universe was 9.1% (US HY) and 8.4% (EUR HY), respectively, compared to only 7.2% (US) and 6.4% (Europe) on 10 March. The highest share of distressed issuers in the USD HY segment was in the media sector; and in the EUR HY segment in the media and technology & electronics sectors. Assuming a default rate of around 30% within 12 months for issuers traded as distressed, the expected default rate for USD HY and EUR HY is somewhat lower than in Moody’s baseline forecast of mid-April.

Preference for the upper-tier high-yield segment

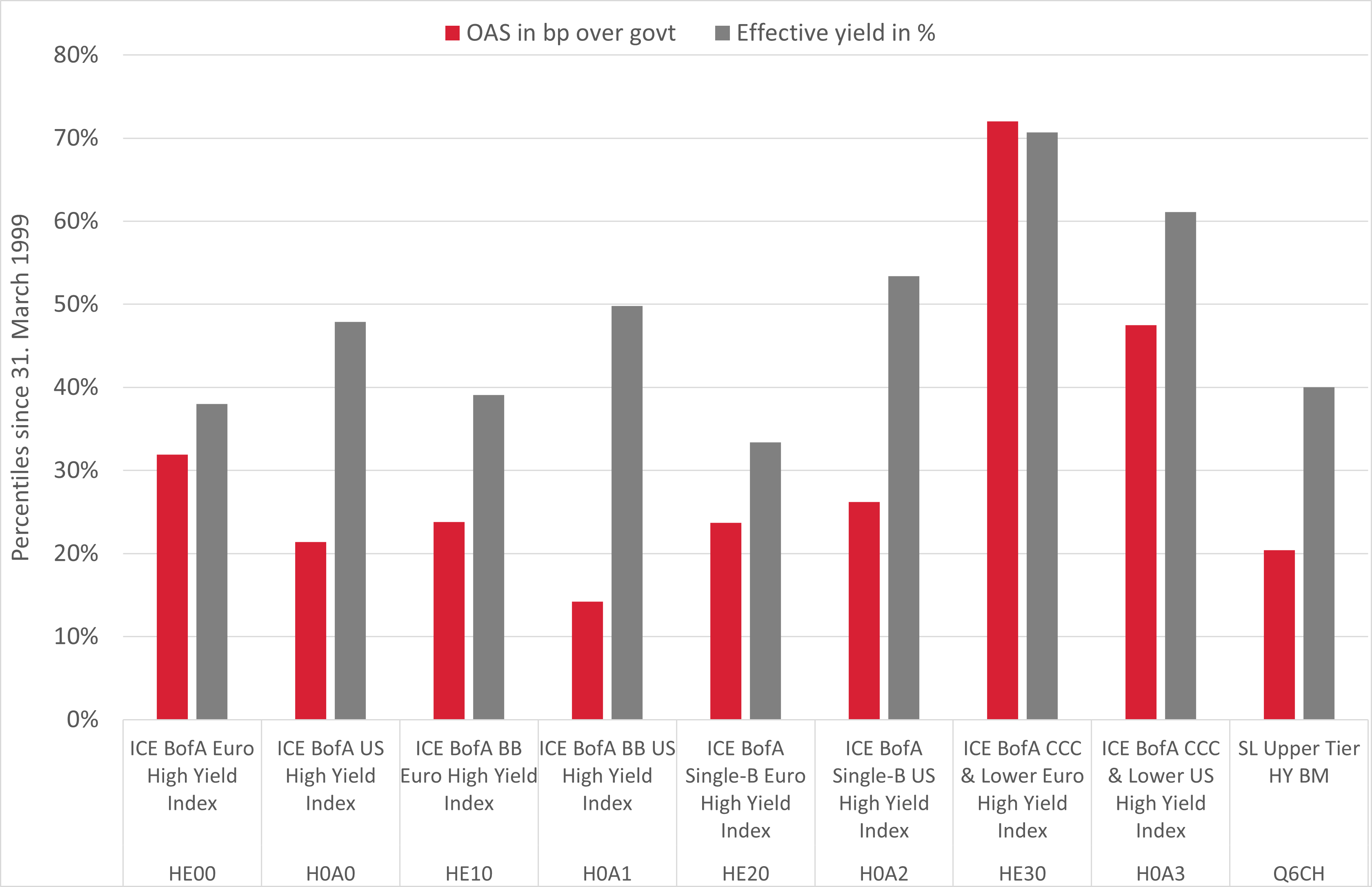

Uncertainties regarding trends in growth, unemployment and inflation in the US and the eurozone, as well as (geo-)political risks, are likely to lead to continued volatility in interest rates and credit risk premiums. Against this backdrop, we continue to favour the high-quality upper-tier segment for high yield bonds and are focusing on the comparatively secure BB rating segment. The benchmark of our upper-tier high-yield strategy is currently trading at a yield to maturity of 5.8%. Solid risk management, a clear focus on active security selection and careful credit analysis are essential components for good performance in this asset class, especially in volatile times.

The monetary policy measures by the central banks could have a supportive effect: the Fed and ECB are expected to make several interest rate cuts by the end of December 2025. This scenario is generally positive for high-yield bonds because, firstly, fixed-coupon bond prices can benefit from falling interest rates, secondly, companies and consumers (with a high proportion of variable debt) have a lower interest expense, and thirdly, lower interest rates stimulate economic growth over time.

Due to the aforementioned uncertainties, we continue to favour the upper-tier segment for high-yield bonds, i.e. the comparatively safer BBs and parts of the B+/B segment. We also value hybrid bonds issued by investment grade-rated companies, which we view as solid components of HY portfolios. They account for almost 30% of the BB index (in EUR). In addition, we are complementing our upper-tier high-yield strategy in USD and EUR bonds with selected attractively priced bonds from the BBB rating category. We prefer BBs and Bs in EUR, as they offer a higher risk spread on average (compared to government bonds) than BBs and Bs in USD.

1 As at 5 May 2025

2 All return and performance data in this text is based on local currency.

3 Calculation basis: Data from 31 March 1999

Swiss Life Asset Managers is a leading asset manager and provider of bond funds – assuming strategic responsibility and ensuring sustainable performance.