The euro and USD high-yield bond indices continued to perform well in 2024 and have so far achieved a performance of around 7.3% and 7.7% respectively.

The high-yield (HY) bond asset class offers a good performance buffer against interest rate and credit spread volatilities due to its solid interest income (carry) and a yield to maturity1 that is above the ten-year average. Against the backdrop of an uncertain macroeconomic outlook, we prefer the upper tier for HY bonds and focus on the comparatively secure BB rating segment with a mix of selected bonds from the B+/B and BBB categories.

Performance and excess return of HY bonds in 2024 again better than expected

The combination of higher returns and lower credit spreads led to an excess return of 5.4% (USD) and 4.4% (euro) respectively compared to government bonds during the current year. As in 2023, excess returns were thus higher than initially expected, although investors feared a more challenging credit market environment due to low growth, cost inflation and higher finance charges. At the start of the year, therefore, six interest rate cuts by the Fed and ECB were still anticipated for 2024. However, thanks to better-than-expected economic growth, the current market assessment indicates that this number of cuts is unlikely.

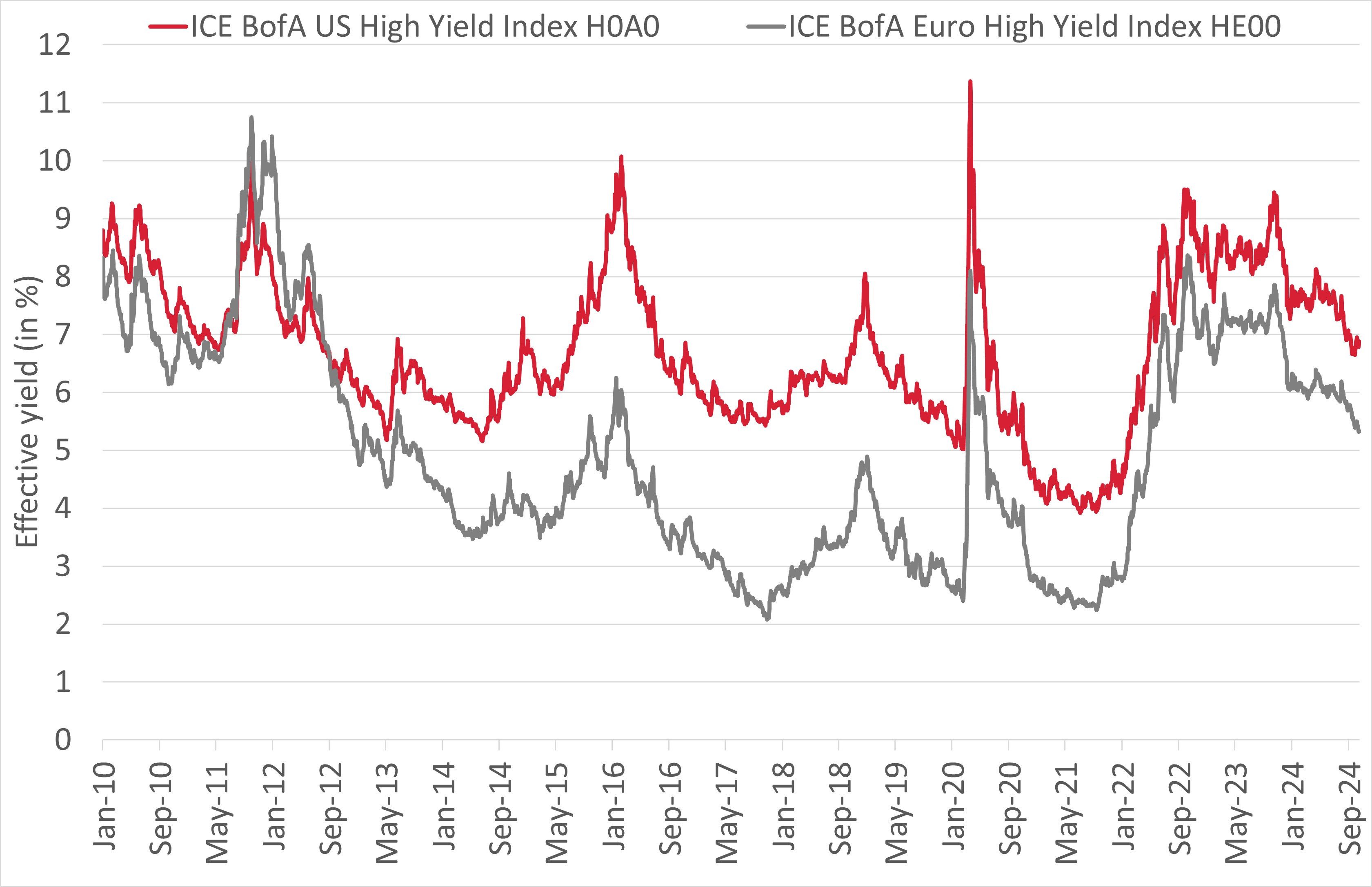

Above-average HY yields to maturity

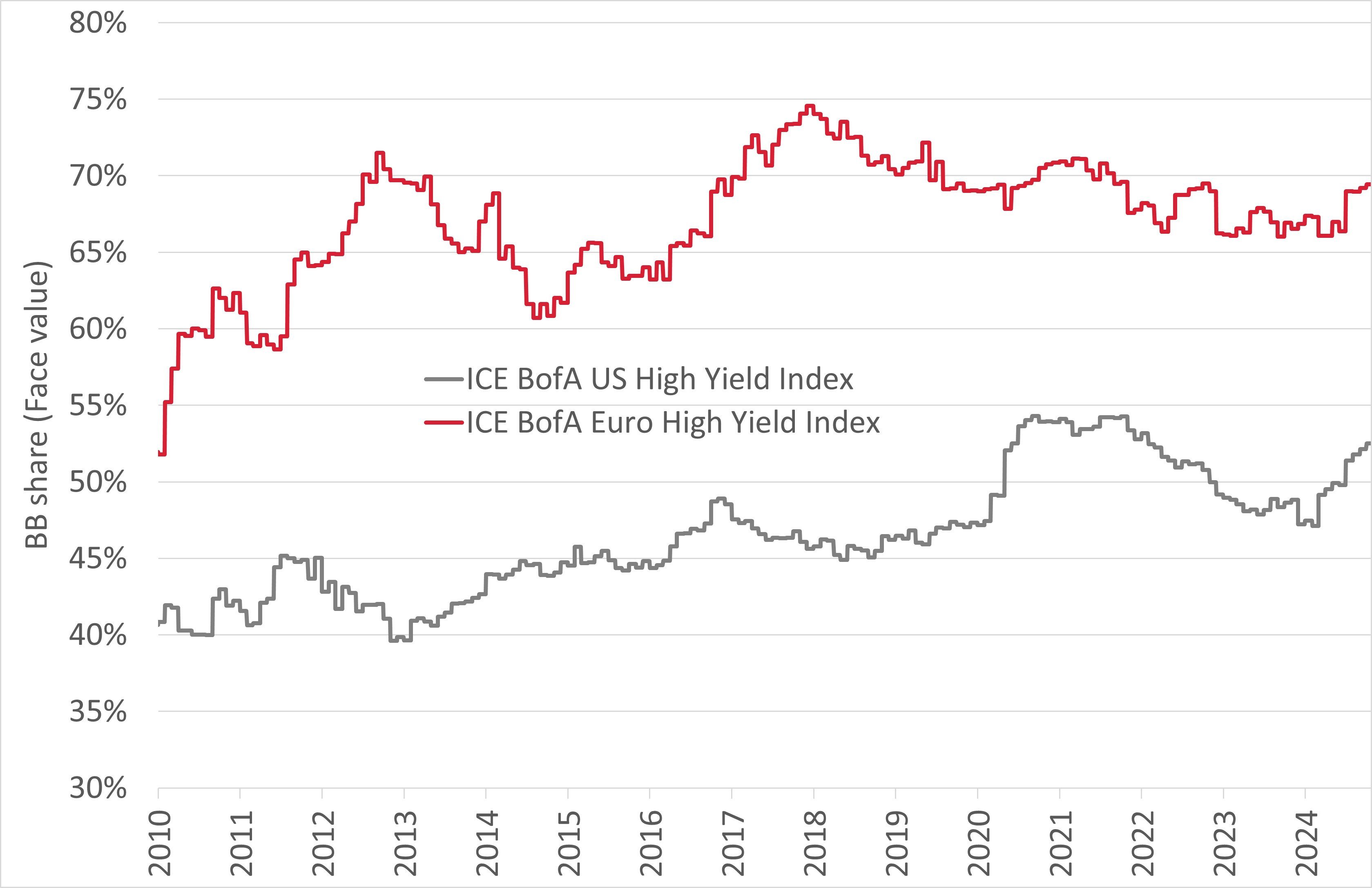

Increase in BB share in HY indices

Lower default rates and reduced credit spreads

Compared to data since March 1999, credit spreads are currently at the low 10th percentile in the USD HY segment and at the slightly higher 20th percentile in the euro HY segment. However, these levels are not unusually low – they are still similar to or even above the levels of 2017 and 2021.

After sub-investment grade default rates rose – in the US since April 2022 and in Europe since February 2022 – shortly after the start of the Russo-Ukrainian war, they have been falling again in the US since May 2024 and in Europe since June 2024. According to the rating agency Moody’s, the current default rate is 5.7% in the US and 3.6% in Europe, which is still above the average of the last two decades of 4.0% and 3.3% respectively. However, the rating agency’s baseline forecast assumes that default rates will fall further to 2.8% in both US and Europe over the next 12 months.

The forecast of these lower default rates is reflected in the low share of distressed2 issuers currently traded. This metric is usually a good indicator of the default rate for the next 12 months. Their share in the HY universe is currently 6.9% (US) and 8.5% (Europe). Assuming a default rate of around 30% of these issuers within the next 12 months, this roughly confirms Moody’s baseline forecast mentioned above. The media and telecommunications sectors (in the USD HY segment) and the media and real estate sectors (in the euro HY segment) currently account for the highest proportion of distressed issuers.

Several factors support investments in HY bond funds

We believe that a number of technical and fundamental factors make investments in high-yield bond funds less risky than it might seem at first glance. Due to some technical developments, the credit spreads of the HY indices are currently generally somewhat lower than in previous periods.

- As a result of the rise in interest rates since mid-2022, the average price of bonds in the HY indices is still only around 97.

- The share of secured high-yield bonds in the euro and USD HY index has risen significantly in recent years (especially in the USD HY index) to around 30–35%. Global recovery rates for bonds have increased somewhat due to cyclical factors and are currently 61% for senior secured bonds and around 37% for unsecured bonds, according to Moody’s.

- The share of BB bonds in the HY indices, which statistically have a lower default rate than B bonds, is somewhat higher than in the past, especially in USD. The share of BB bonds with an attractive yield by historical comparison is currently 69% for euro HY and 53% for US HY.

From a technical point of view, it is also positive that not only is demand for HY bonds still high due to the historically attractive yield, higher coupon payments and the priced-in prospects of a soft landing for the US economy, but also that the high-yield bond index has contracted since its record size in 2022. This reduction in supply was technically positive for credit spreads. However, we expect the volume of new issues to increase for the purpose of refinancing bond maturities early. Although this could lead to some volatility in credit spreads, the level of net issuance should be around the average of previous years and thus sustainable for the market, as market volume is expected to remain more or less stable. This opens up interesting investment opportunities, as the refinancing issues are often associated with a new issue premium. It is also expected that new names will enter the high-yield market and provide some diversification.

Due to the higher coupons on the bonds issued since 2022, the duration for both euro HY and US HY is significantly below the average of the past ten years. This low duration level usually reduces the impact of spread and interest rate volatility on performance. However, the risk increases as bonds are redeemed early by the issuer and then refinanced at a lower coupon.

Finally, from a fundamental point of view, we still consider key credit figures of US HY issuers to be quite appropriate. Although sales and EBITDA growth rates and key figures such as net debt have weakened in recent quarters, they remain at a high or even higher level compared to their long-term averages.3

Preference for the upper-tier high-yield segment in euros

Uncertainties regarding trends in growth, unemployment and inflation in the US and the eurozone, as well as (geo-)political risks, are likely to lead to continued volatility in interest rates and credit spreads. Nevertheless, we believe that this asset class offers a performance buffer against these market volatilities due to the solid interest income (carry) from coupon payments and the yield to maturity of 6.9% (USD) and 5.3% (euro), which remains above the ten-year average.

The current yield to maturity suggests that this asset class will continue to perform well. Our view is based on the consensus scenario of falling market interest rates and a period of weaker macroeconomic indicators before lower interest rates have their stimulus effect on the US economy. Currently, the Fed and ECB are expected to make four interest rate cuts by the end of June 2025. This scenario is generally positive for high-yield bonds because, firstly, fixed-coupon bond prices can benefit from falling interest rates, secondly, companies and consumers (with a high proportion of variable debt) have a lower interest expense, and thirdly, lower interest rates stimulate economic growth over time.

Due to the aforementioned uncertainties and the now lower credit spreads, we continue to favour the upper-tier segment for high-yield bonds, i.e. the comparatively safer BBs and parts of the B+/B segment. We also value hybrid bonds issued by investment-grade-rated companies, which we view as solid components of HY portfolios. They account for almost 30% of the BB index (in euros). In addition, we are complementing our upper-tier high-yield strategy in USD and euro bonds with selected attractively priced bonds from the BBB rating category. We prefer BBs and Bs in euros, as they offer a higher risk spread on average (compared to government bonds) than BBs and Bs in USD.

Source of illustrations above: ICE, Bloomberg (21. October 2024)

1 All return and performance data in this text is based on local currency.

2 Issuers having at least one bond traded with a credit spread of more than 1000 basis

points are considered to be distressed.

3 Source: J. P. Morgan, data up to Q2 2024, 485 US HY issuers, excluding financials and utilities

Swiss Life Asset Managers is a leading asset manager and provider of investment funds – strategically responsible and with consistently solid performance.

Further information on hybrid bonds

Hybrid bonds as solid components of high-yield portfolios