Forecasts for 2024 continue to look rather positive, despite geopolitical uncertainties remaining high. Daniel Rempfler, Head Rates & Emerging Markets, Matthias Vögeli, Head Treasury, FX & Rates Derivatives, and Damian Künzi, Head Macroeconomic Research, provide an overview of the latest figures and developments on the Swiss financial market.

The Swiss inflation outlook is even brighter than before following the latest downside surprise in January. In particular, it seems that the VAT increase that took effect on 1 January 2024 has hardly been passed on to end consumers so far. The strong franc and falling prices at producer and import levels suggest there will be a further decline in consumer goods inflation. Rents remain the main price driver in 2024. Swiss Life Asset Managers currently expects the inflation rate to settle in between 1% and 1.5% during the course of 2024.

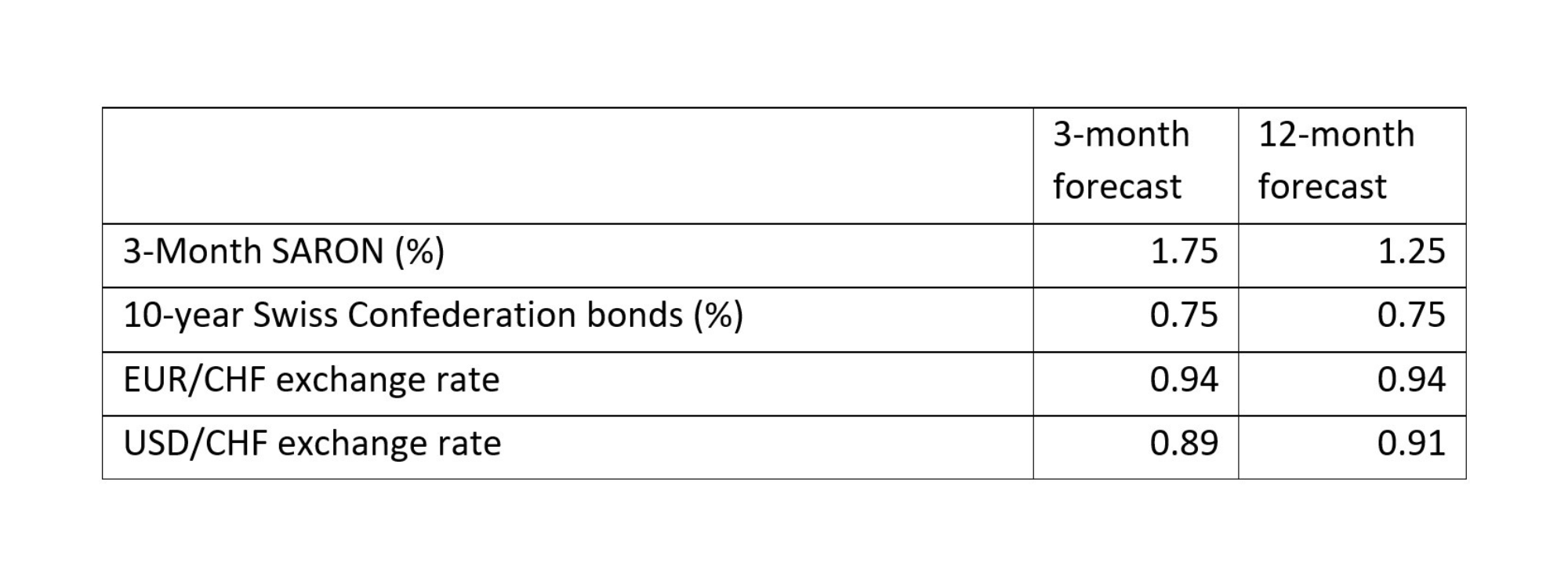

SNB rate cuts expected earlier

Following the surprisingly low inflation figures in January, the probability of an initial interest rate cut by the Swiss National Bank (SNB) at its next meeting in March has already increased. In light of this, we will review our previous forecast, which assumed two interest rate hikes by the SNB in September and December 2024, in the next few days at the upcoming Investment Committee. The forecasts for the three-month SARON could also be revised downwards. With regard to 10-year Swiss Confederation rates, our forecast of a slight decline to 0.75% by the end of the year remains unchanged, partly because interest rates in Switzerland fell considerably more than in the rest of Europe and the US last year.

SNB Chairman Thomas Jordan recently made several comments on the strength of the Swiss franc and the negative impact this is having on economic growth in Switzerland. In this context, he also made express mention of possible interventions on the foreign exchange market to weaken the Swiss franc. The increase in commercial banks’ demand deposits at the SNB since the beginning of the year is an indication that the SNB has already sold Swiss francs in the market, which has contributed to the recent weakening of the franc. We consider the relatively significant trade-weighted real weakness of the franc since then, at minus 3%, to be entirely justified given the inflation outlook and the exaggerated strength of the franc at the end of 2023.

Swiss franc exchange rates against euro and US dollar

The EUR/CHF exchange rate is currently close to our year-end forecast at 0.94. However, despite the inflation forecast, we remain sceptical about a further significant EUR/CHF appreciation. Uncertainties regarding the growth and inflation outlook in Europe remain elevated. We see geopolitical risks and the US elections as factors that should support the Swiss franc. Regarding the USD/CHF rate, we remain rather positive with our 0.91 forecast, not least due to the expected divergence in key rates and the correspondingly high FX hedging costs.