How political uncertainties and structural challenges are weighing on government bond markets.

Global government bond markets, once the epitome of stability, are coming under pressure in the summer of 2025. Buyers’ strikes, political uncertainties and dwindling confidence in fiscal management are upsetting the fragile balance between growth and debt. This article focuses on the US and Germany – two markets with different starting points, but facing similar challenges.

USA: crisis of confidence in the bond market

The so-called “Liberation Day” in April marked a turning point. Within a few days, market sentiment had changed dramatically. US Treasury rates soared, which is unusual for an asset class traditionally considered to be safe. This was triggered by various rumours of sell-offs by foreign states, especially China, and later the “Big Beautiful Bill”, which led to talk of potential taxation of US Treasuries.

The nervousness was palpable – and it had a global impact. Serious questions were posed for the first time as to the safe-haven status of US Treasuries. Nevertheless, they are likely to maintain this status for the time being, as the latest data on capital flows to and from the US show that private investors in particular have been selling their Treasuries, while governments such as China have hardly been active. Nevertheless, confidence remains weak and there is a clear trend towards broader diversification. Likewise, Liberation Day has shown that the US government is not immune to upheavals on the bond market. While US Treasuries will likely be back in demand in a real recession scenario, any further loss of confidence could trigger disproportionate market reactions in the current environment.

Germany: confidence despite debt explosion

Germany is continuing to benefit from its low debt-to-GDP ratio and has a degree of fiscal leeway. The announcement that it would massively increase its debt was welcomed as the impetus needed to strengthen its economy and help it transform. The figures recently presented are impressive: for 2025, the Federal Ministry of Finance is planning net borrowing of EUR 81.8 billion for the core budget and EUR 61.3 billion in special funds. By way of comparison, the 2024 budget contained just EUR 33.3 billion.

By 2029, new debt is expected to amount to up to EUR 185.5 billion (of which EUR 126.1 billion is for the core budget). The key factor here is whether these funds are used efficiently or are sunk into structurally ineffective spending. Initial doubts are reasonable.

Solutions: shorten maturities, make regulatory changes

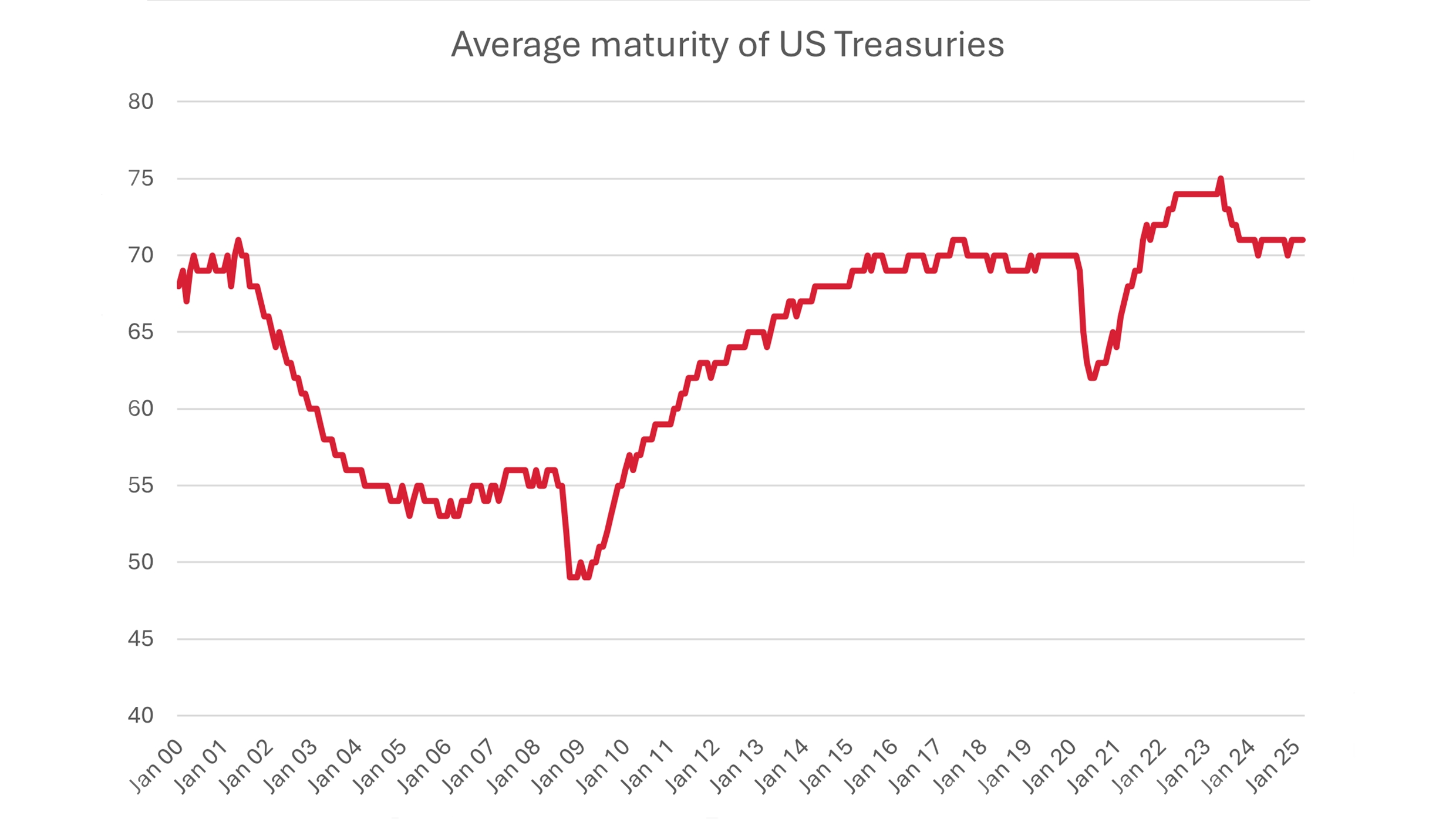

In view of rising refinancing costs and growing political risks, many countries are seeking relief. A common strategy is to shorten the average debt maturity. In the US, it is currently around 71 months – historically it has been closer to 61. Countries such as Japan and the UK have already announced that they will cut back on issues with long maturities over the long term.

Source: US Treasury Department, marketable interest-bearing US Treasuries

Regulatory measures could also help. In the US, there are discussions over the potential reform of the supplementary leverage ratio to make holding US government bonds more attractive for banks. However, the current draft remains vague – so no clear regulatory signal is being sent to the markets.

These measures can relieve pressure in the short to medium term, but they do not solve the structural problem: debt paths that are unsustainable over the long term. Credible strategies to reduce debt ratios remain essential.

In short: confidence remains the hardest of all currencies

As long as confidence holds, the markets will continue to function. But the balance between growth, debt and political credibility has become somewhat delicate. Investors are more selective, global-minded and cautious.

There are also bright spots: Spain, for example, has regained investors’ confidence thanks to its willingness to reform and fiscal discipline, and is being rewarded with lower refinancing costs. This is an important message from the market that can also serve as a guide for other countries.

Opportunities for active management are opening up in an environment of increasing volatility and market complexity. The tactical management of durations, an in-depth understanding of fiscal risks and global diversification are becoming important success factors. At a time when uncertainty is becoming the norm, flexibility is essential.