For years, the sharp rise in government debt hardly featured in public discourse. That is no longer the case. The higher interest rates mean that governments around the world are paying the price for their shortcomings.

A glance at the statistics shows the enormous growth in debt. According to the International Monetary Fund (IMF), the government debt-to-GDP ratio in the US rose from 66% to 123% between 2000 and 2023. In the eurozone, the debt ratio grew from 70% to 89% over the same period. However, there are significant differences within Europe.

In the US, strong fiscal stimulus measures have made a significant contribution to the country’s recent economic dominance. For many years this was not a problem for investors in government bonds, as the low interest rate environment artificially favoured debt sustainability. In addition, the expansionary approach of central banks, which bought up government bonds in large quantities, led to high demand and low refinancing costs – irrespective of the national budget’s actual state of health.

Rising interest burden and diverging public finances

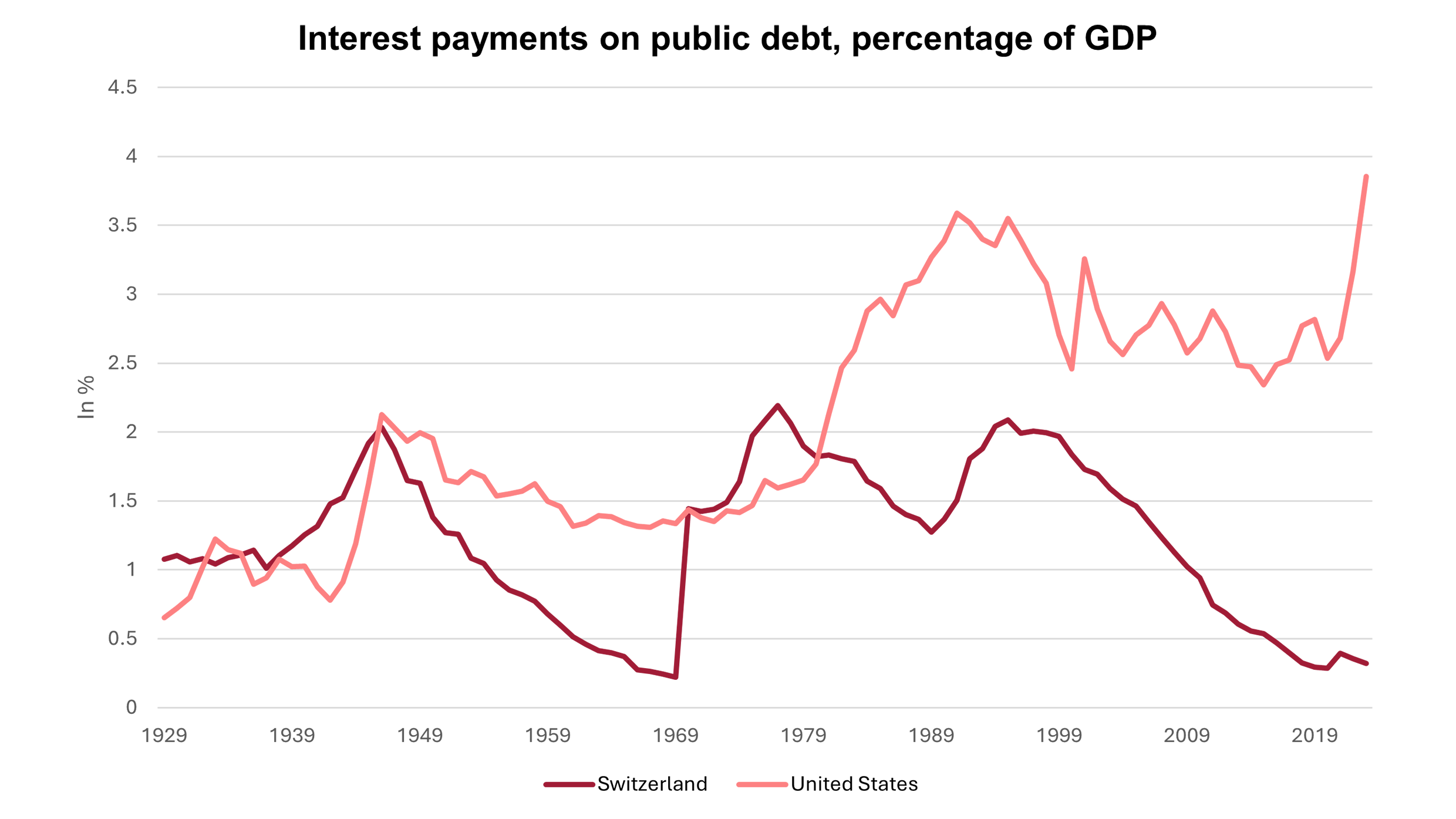

The sharp rise in inflation following the coronavirus pandemic led to higher interest rates and a contraction in central bank balance sheets. As a result, the global focus has once again shifted to the risks posed by overstretched public finances. The higher interest burden increases the risk of over-indebtedness. In 2023, according to the IMF, the US spent 3.86% of its GDP on interest payments. By contrast, Switzerland benefits from low levels of debt and lower interest rates. In the same year, it spent only 0.32% of its GDP on interest payments.

Source: International Monetary Fund (IMF)

Growing divergences are increasingly forcing investors in global government bonds to analyse national budgets even more carefully and diversify more broadly. These differences are reflected in corresponding risk premiums and yield curves of varying steepness. In-depth analysis and active positioning of the portfolios – taking into account the aforementioned factors – makes it possible to generate higher returns in comparison with traditional government bond indices.

Emerging markets can be an interesting alternative in this context, as they often have a lower debt ratio. At the same time, the question arises as to the appropriate “risk-free” reference yield. Negative swap spreads, i.e. the difference between the swap interest rate and the government bond yield, are a global phenomenon. They reflect the growing supply of government bonds and the associated risks – a trend that in all likelihood has not yet been exhausted.

Targeted investments or fiscal risk?

The key question here is this: is additional debt being used efficiently and purposefully to promote sustainable growth, or is it merely a form of clientelism? The US currently benefits from its economic dominance. Although the hype around AI and tech may be exaggerated, the lack of attractive and liquid alternatives is keeping demand for USD financial assets high for the time being. This is one of the main reasons why US Treasuries have not experienced any major upheavals so far. While unlikely to change in the short term, this trend entails risks in the medium to long term.

Examples from Europe show how quickly markets can react to fiscal policy uncertainties. In 2022, Liz Truss was forced to step down as UK Prime Minister after just a few weeks in office because her budget had shaken market confidence due to its lack of credible funding. A similar picture emerged in France last summer, when uncertainties about majorities following the snap election triggered a sell-off of French government bonds and pushed up refinancing costs. In both cases, there was a lack of clear structural reforms that would indicate an attractive growth path.

Having been affordable for years, this clientelism has an expiry date and structural reforms are urgently needed, especially in Europe. There is a certain irony in the fact that the countries once hit hardest by the euro crisis, such as Ireland, Spain and Portugal, but also Greece, are now the new model pupils. The example of Spain illustrates this transformation. Measured in terms of the ten-year yield, the country now has lower refinancing costs than France and, according to Oxford Economics, higher growth potential.

Against this backdrop, Germany’s recently announced plans to raise massive amounts of additional debt seem like a bold experiment. It is true that Germany is in a position in which it can afford to do this, but whether these measures will be enough to challenge US economic supremacy remains to be seen. What is certain, however, is that the decision has ushered in a new era. The markets’ immediate reaction was clear: on the day of the announcement, ten-year yields in Germany saw their sharpest increase since reunification. Bond investors will monitor Germany’s plans closely. If the funds were to be invested in a targeted manner and Europe were to experience a surge in growth as a result, this would be a statement of intent vis-à-vis the United States.

Where now for the US?

Political uncertainties have increased under the second Trump administration, endangering US economic dominance and confidence in its debt sustainability. Unsurprisingly, the new Secretary of the Treasury, Scott Bessent, has recognised this problem. Recent efforts to ease the regulations on banks holding US Treasuries seem to be primarily aimed at attracting additional buyers – and are a way of artificially increasing demand.

The often-cited argument that concerns about debt are dampened by the US dollar’s status as a reserve currency is only partially convincing. This special status is primarily a consequence of the United States’ economic dominance. A structural slowdown in the economy would be problematic for investor confidence. In the medium to long term, therefore, a more cautious fiscal policy is also likely to be unavoidable in the US.

Source: Schweizer Personalvorsorge 05/25