As the outlook for total returns on European real estate begins to slip, thematic investment strategies can help to build diversified portfolios that achieve long term market outperformance, while remaining in line with ESG and net-zero objectives. Our proprietary European Thematic Cities Index is an important research-driven tool that supports long-term real estate investment strategy decisions.

The current investor sentiment for the built environment has resulted in a polarisation of returns

In the current real estate investment environment, long term institutional investors seek to identify real estate that is positively aligned to future change in order to ensure portfolio resilience. Against this backdrop they have become increasingly focussed on areas of the market strongly aligned to structural changes. This has resulted in significant polarisation in performance between real estate sectors, i.e. strong returns for logistics versus weak returns for shopping centres.

As a guiding principle to navigate increased market uncertainty, Swiss Life Asset Managers applies a thematic investment approach that identifies key overarching themes, the 5 C’s, that will drive real estate performance in an ever-changing world. The 5 C’s are: Change & Disruption, Climate & Environment, Communities & Clustering, Consumers & Lifestyle, and Connectivity. Swiss Life Asset Managers has built on years of expertise applying the 5 C’s to identify opportunities across countries, cities and assets.

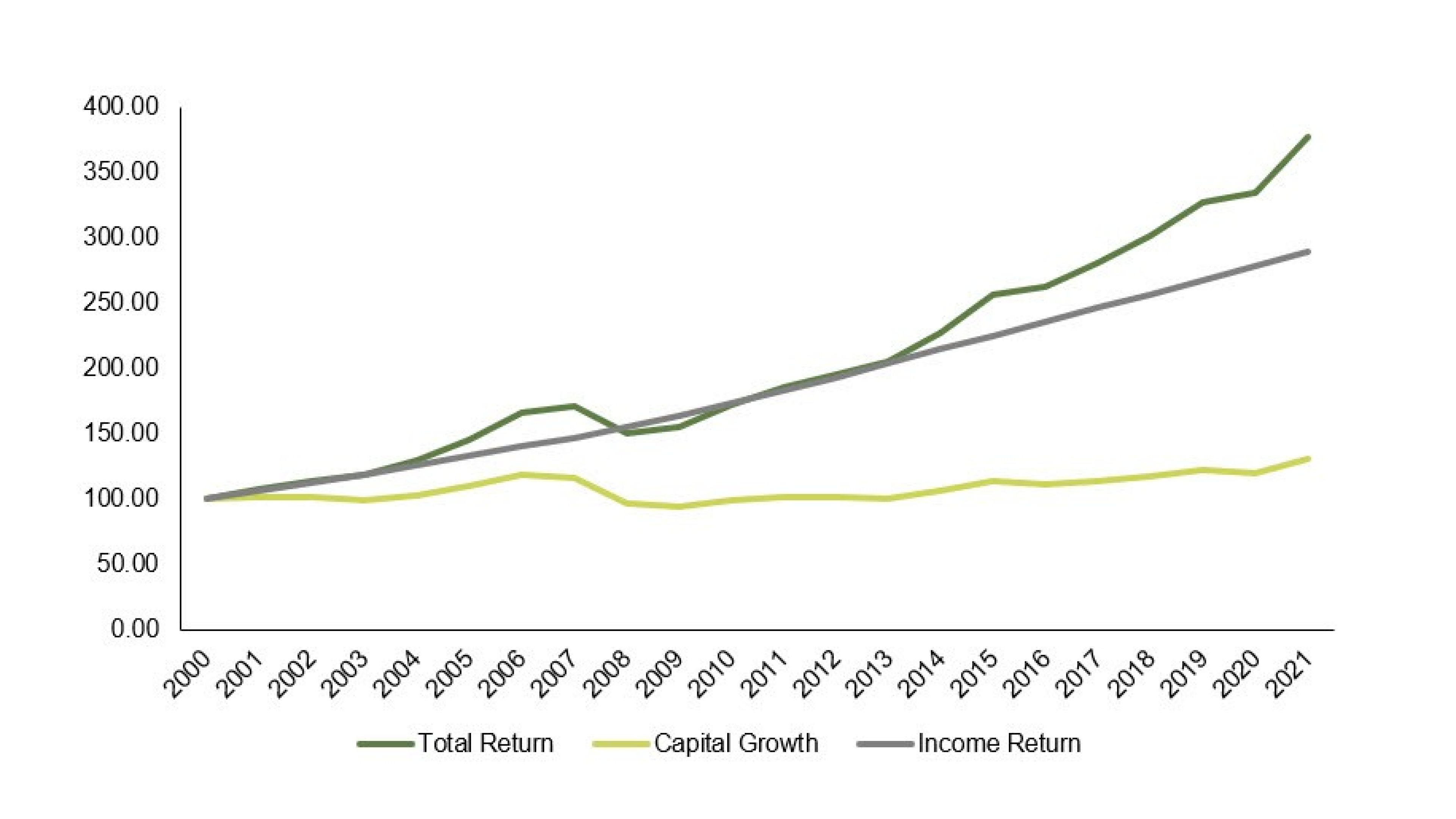

Income is the driving force behind core investment performance over the long run

Core/Core+ open-ended strategies with an unlimited life typically have absolute return objectives in accordance with what investors in core real estate can expect in the long run. According to the MSCI Pan European Index, which is calculated using the performance of over 37,000 assets across Europe, with a capital value of more than €894bn, the long run property-level (gross of management fees and vehicle costs) unlevered total return for European real estate (all property) has been 6.5% p.a. nominal (2001-2021).

Another insightful benchmark is the INREV European Open End Diversified Core Equity Fund Index (“European ODCE Index”) which measures the performance of 16 funds with a gross asset value (GAV) of €46.4bn that invest across Europe and across multiple sectors.1 The Index measures fund performance net of fees and costs and provides transparency and consistency of assessment in the analysis of peer group performance. The Index shows a nominal distributed income return of c. 3.3% p.a. and a nominal total return of 5.6% p.a. over the last 10 years.

European ODCE Index distributed income returns have averaged c. 3.3% in the last 10 years

Source: INREV Open End Diversified Core Equity (ODCE) Fund Index – Index Q2 2022

Real estate remains a core component of institutional investment portfolios. For investors with long-term horizons, income returns have historically been the main drivers of performance. The predominantly index linked income return derived from European real estate remains attractive relative to other assets classes. Nevertheless, the higher inflationary environment requires enhanced focus on tenant covenant strength and careful consideration of legislative and reputational factors.

Income returns have historically been the main drivers of long-term total returns

Source: MSCI European All Property Index December 2021 (Property-Level)

Resilient income returns require disciplined investment and risk-management

Investment managers have a fiduciary duty to adhere to a disciplined investment approach when investing on behalf of third-party clients. Investments should therefore not diverge from pre-agreed risk parameters to ensure investors’ tolerance for risk is respected. Specifically, it is dangerous for managers to respond to higher market prices by moving up the risk curve as this will increase volatility and the risk of future underperformance.

Our view is that when implementing a core/core+ strategy we will not take risks on locations or property fundamentals, but we will take advantage of asset management opportunities to enhance longer-term returns where the portfolio can accommodate it. This controlled risk-taking supports longer-term target returns in excess of average core income returns. We believe our deep networks and in-depth local market intelligence allow Swiss Life Asset Managers to identify mispriced opportunities.

Expected risk parameters of core European diversified real estate

The following must be consistently applied across the business cycle:

- Low to moderate leverage – less than 40% LTV

- Focus on stabilised assets – restrictions on speculative development

- Country and sector diversification to ensure a spread of exposure

- Focus on western Europe and primary markets that offer significant liquidity

- Maximising income diversity and mitigating location/asset/tenant/lease expiry clustering risks

- High quality micro-locations in both established and emerging submarkets

- Long-term income security backed by predominantly strong covenants to generate stable income returns

Investing thematically provides an edge over the competition

A thematic investment strategy is cognisant of structural changes within the economy and ensures that we are investing in assets and locations with enduring occupier appeal that will in turn generate resilient long-term income returns. Adopting a thematic approach, we invest with conviction throughout the market cycle to generate long-term outperformance.

To this end, Swiss Life Asset Managers' European Thematic Cities Index is an important research-driven tool that supports long-term real estate investment strategy decisions. This proprietary index measures European cities against five core themes aligned with major trends shaping a city's real estate market: dynamism, healthiness, networks, cosmopolitanism and accessibility.

Furthermore, the focus on ESG and investors’ net zero pathway is crucial to ensure long-term liquidity in equity and debt markets, while also mitigating risks of capital depreciation. Despite growing awareness, we believe that the market does not yet systematically correctly price ESG considerations due to a lack of data availability, providing opportunities to further identify mispriced assets.

The Alternative Living asset class is an important diversifier in core real estate portfolios

The residential sector is considered thematic as it is underpinned by urbanisation, which is driving strong population growth in thematic cities, and demographic change through the growth in single households across the age spectrum. As a result, the alternative living sector has represented a growing share of core investors’ tactical allocations to real estate in recent years and it is therefore important for a truly diversified strategy to have a substantial long-term allocation to the asset class.

The residential sector offers attractive portfolio diversification benefits. Stability of income is derived from highly granular income, given the large number of underlying tenants and results in low volatility in performance. Residential assets are also seen as efficient liability hedges due to their high correlation with inflation, which also supports long-term value appreciation.

Given the low risk profile of the asset class, we will consider generating above-average returns by investing, where appropriate, in alternative living sectors, including senior living, micro-living and co-living, as well as traditional residential assets in select cities with strong underlying fundamentals where higher yields can be achieved compared to European capital cities.

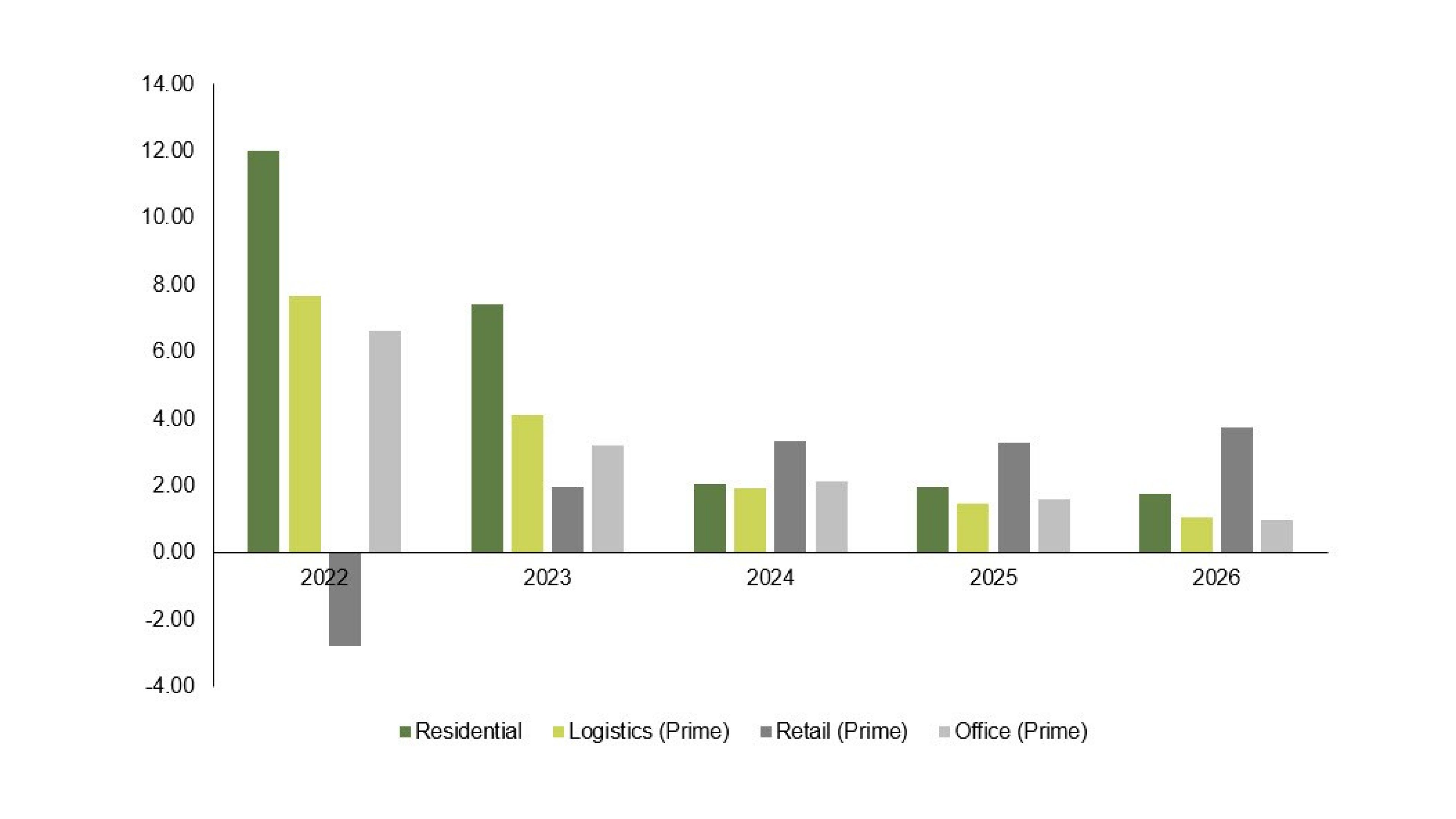

The PMA Total Returns forecasts highlight the expected benefits of incorporating residential real estate in a thematically aligned diversified portfolio, with the sector anticipated to provide more stable performance than logistics and offices over the five-year forecast period.

Source: PMA Forecasts – Total Returns Europe (Main Scenario, June 2022)

Conclusion

Despite the lower return environment, managers of core/core+ strategies must not stray from pre-agreed risk-return parameters and ensure that they construct thematically aligned portfolios to generate sustainable long-term returns. Swiss Life Asset Managers’ substantial pan-European platform with local market expertise and strong research capabilities enables it to take advantage of pricing inefficiencies and asset management opportunities to enhance core/core+ returns where portfolios can accommodate them.

Authors: Tim Munn, Chief Investment Officer, Mayfair Capital and Guillaume Lau, Portfolio Manager, Mayfair Capital

1 INREV Open End Diversified Core Equity (ODCE) Fund Index – Index Q2 2022

By thinking long-term and acting responsibly we develop future-oriented investment solutions.