The Paris office market has often acted as a safe haven for investors. With rising inflation and interest rates, on what strengths can the Parisian market rely on? And where are the risks?

Inflation, rising interest rates and a surge in energy prices have taken their toll on domestic demand such as households’ purchasing power or companies’ solvency, suggesting with an increasing probability that the US and the Eurozone might be heading for a recession. Europe is the most vulnerable given both the nasty spike in gas prices as well as the potential shortage of gas. The ECB is caught between a rock and a hard place – between taming inflation and securing the Eurozone stability. A mild recession in Europe would avoid property markets to behave like in 2008, when they were hit hard in terms of capital value falls.

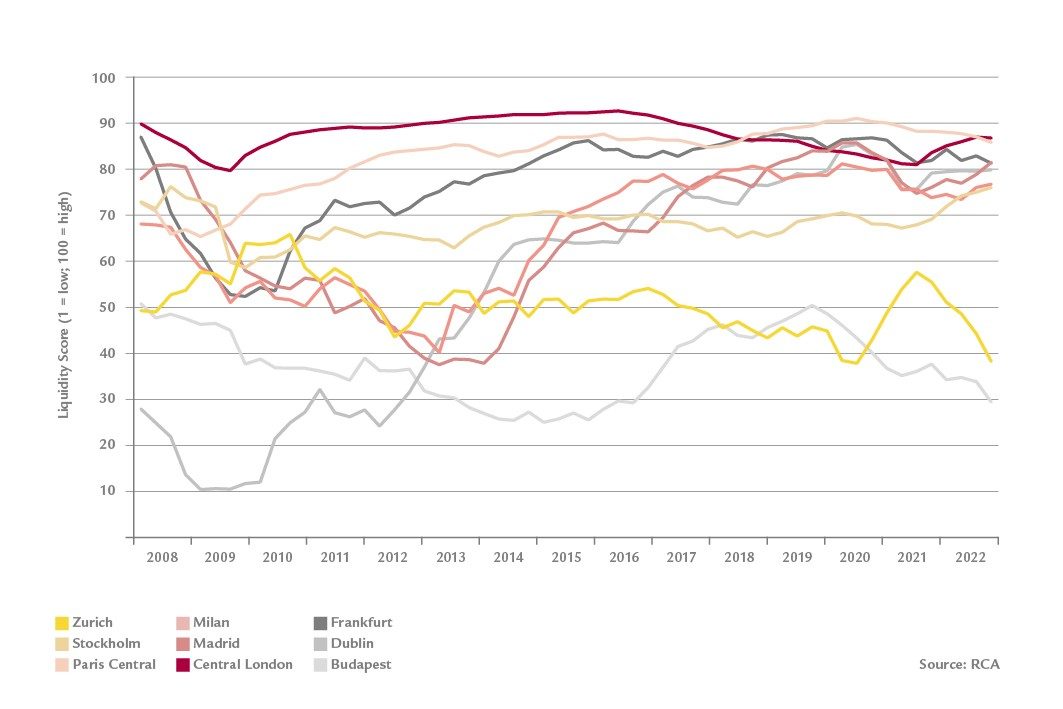

Less liquidity and more volatility to take toll on commercial property markets

So far, interest rises1 have already pressured risk premium across Europe as well as risk premium across asset classes. In the European REIT (Real Estate Investment Trust) spectrum, the falling share prices in the office, logistics, retail, and residential asset classes suggest a knock-on effect on the direct investment market across sectors in the coming quarters. In Q2 2022, risk premiums on prime office buildings were around their long-term trends for most European countries including Paris. The trajectory of the risk premium in Q3 2022 will be key for the speed of the price-discovery process. However, as less liquidity and more volatility are expected to take their toll on the property markets, risk premiums are expected to increase, implying an outward yield shift across the board. The magnitude will not be similar across markets and sectors in Europe, given differences in market fundamentals and liquidity. In such a context, the question arises: Will Paris remain a good allocation investment for long-term investors?

Paris city with highest rental growth trend per annum

For many years, Paris city has relentlessly been considered a safe haven investment, being more defensive in market downswings or economic downturn and outperforming in the recovery phase of the cycle. Since the recovery in 2014 following the aftermath of the Global Financial Crisis, Paris city has provided healthy total returns, outperforming the French office market, any other submarkets in the Paris region, in terms of total returns. Apart from a higher capital growth driven by a strong cap-rate compression, Paris city has provided the highest rental growth trend per annum which was fed through attractive net operating income growth and dividends for investors. The engine of such a rental value growth has been driven by innovation and productivity growth of the Parisian tenant landscape as the economic base of the capital was catching up in terms of digitalization, robotization and other technologies. As long as rental value growth mitigates the rise in the discount rate, Parisian office market will continue to remain a core allocation within real estate portfolios.

Paris office market more resilient than European peers

This was also the case from 1974 to 1982, when inflation was high, at an average of 11.5%, with high levels of interest rates. Despite that, Paris real estate has offered attractive real returns in both the residential and office asset classes, from long-term investor’s memory. Of course, cycles as well as outcomes are different now. Even so, in the current global downward phase of the cycle, the Paris office market may show stronger resilience than peer markets in Europe. Such a statement, however, relies on both macroeconomic and property fundamentals. The following five points underline this:

- France is less dependent on Russian gas than peers in the euro area such as Germany and Italy.

- France is not an industrial export-led country compared to peers, and benefits from a diversified economic profile: it is thus less vulnerable to the global economic headwinds from both the US and Asia. As such, there are fewer downside risks related to shortage and output growth potential for both 2022 and 2023.

- Inflation in France is set to be lower than in the Eurozone ,given the price cap decided on by the French government. French companies should be in a better shape than peers in terms of competitiveness and margins.

- Paris city has reinforced its polarization since the end of the Covid-19 pandemic; the capital is more resilient to remote work than outer suburbs and peer European capitals. Price-setter companies located within the capital might continue their business as usual while price-taker companies might feel the chill of increasing production costs: thus, discrimination among tenants to secure stable income streams will remain the cornerstone in the underwriting process.

- The supply shortage has usually been a buffer to avoid a sharp contraction in market rental value and this time, it is no different.

Paris will not lose its sparkle

There might be some headwinds to such economic and property statements. The losses driven by the equity and bond markets have impacted the denominator effect which can generate portfolio rebalancing or allocation adjustments like elsewhere. Some institutional investors might have to reduce their exposure to property and Paris. This could create opportunities to buy but it could also mean less capital inflows towards the Paris office market, as well as downward pressures on prices. But at the end of the day, over the mid- to long-term, Paris will not lose its sparkle.

1 At the Jackson Hole conference, ECB officials warned that monetary policy could remain tight for an extended period.

2 5.2% in 2022 and 2.9% in 2023 compared to 7.7% in the Eurozone in 2022 and 3.4% in 2023 according to Swiss Life Asset Managers Perspectives (August 2022).

Liquidity store, a measure of transactions on the investment market

Image Sources: Swiss Life AM, Assembly/Mark/Kreation

Find out more here about the real estate use classes in which Swiss Life Asset Managers is invested.