On 26 July 2012, about ten years ago, Mario Draghi, the then new President of the European Central Bank, gave a memorable speech. He made the famous promise that his ECB would do anything to save the euro.

“Whatever it takes” has since become a popular saying.

Even if everything is topsy-turvy again in Rome, the southern countries of the eurozone are still benefiting from this promise. The interest rate on a 10-year Italian government bond was 6.5% in July 2012, whereas today the Italian Minister of Finance has to pay 3.3% interest if he borrows funds for 10 years.

Despite all the prophecies of doom, the number of countries participating in the European Monetary Union has increased by two in the past decade, and Croatia is expected to join the eurozone next year as the 20th country.

So did Mario Draghi open the door to a success story ten years ago? And how will the history of monetary policy continue? In the following, five theses on the future behaviour of central banks are discussed.

1. The creativity of central banks should never be underestimated

Robert Musil, the great Austrian author of the “The Man without Qualities”, also dealt with experimental psychology. In March 1937, he was invited to give a lecture entitled "On Stupidity". In it, he discussed a statement by someone he called an “imbecile”, taken from a psychiatric textbook published in 1913:

“One not entirely intelligent young woman considered it a bad joke to expect her to hand over her savings to a fund that bears interest: no one would be so stupid as to pay to have his money kept!"

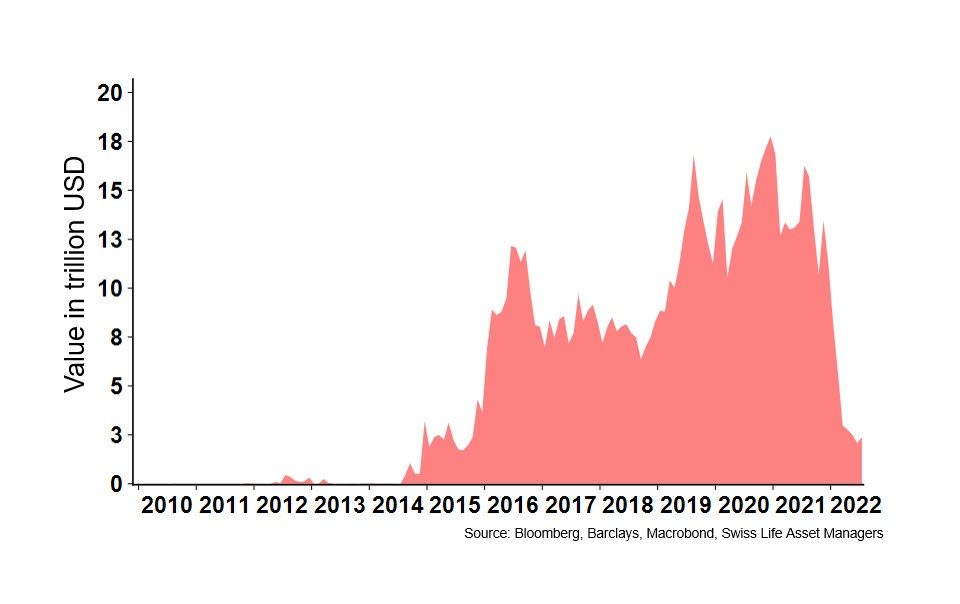

Musil thus gave us probably one of the oldest references to the possibility of negative interest rates. Over 100 years ago, what only seemed possible and correct to a “crazy person” – that she would actually have to pay to park her money at a savings bank – has become part of everyday life thanks to the creativity of the central banks. In the meantime, the volume of negative-interest bonds amounted to just under USD 18 000 billion.

Diagram 1: Outstanding bonds with negative yields

Even before the introduction of negative interest rates, however, the central banks were still creative as regards the ongoing realignment of monetary policy.

After the stagflation disaster of the 1970s, most central banks gradually distanced themselves from monetary control and instead embraced an inflation target. The provision of liquidity to the financial system should be based on a pre-determined inflation rate.

Overall, the trick worked excellently, also thanks to the disinflationary development following the fall of the Iron Curtain.

However, experienced investors still remember an accident in the 1990s: in February 1994, the Federal Reserve unexpectedly raised key interest rates. The NZZ described the ensuing event as a "bloodbath on the bond markets".

To prevent this from happening again, the Fed became the first central bank to subsequently commit itself to “forward guidance”. Since then, the aim has been to gently prepare the financial markets for changes in monetary policy. The economic framework conditions were fine-tuned, for example, in that the Federal Reserve accepted an increase in long-term interest rates or a correction on the stock market simply by communicating monetary policy intentions. Other central banks adopted the idea of “forward guidance” following the events of 2008.

In general, the 2008 financial crisis and the subsequent European debt crisis required a great deal of creativity from central banks. From now on, the sheer limitless expansion of central bank balance sheets, minimum exchange rate limits and, above all, the notorious minus interest rates were key elements of the monetary policy toolbox.

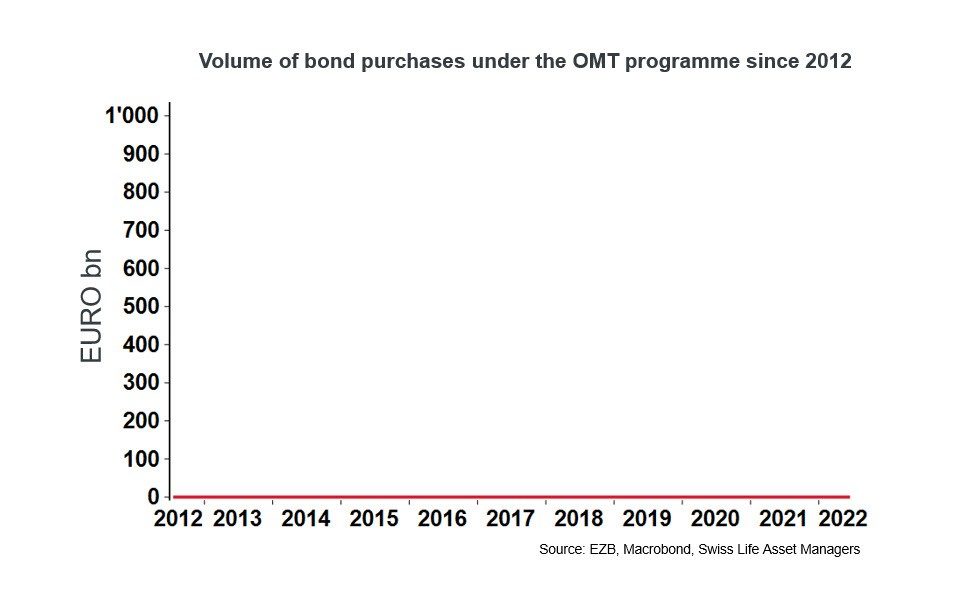

The masterpiece of creativity was achieved by Mario Draghi: in his famous speech in July 2012, he announced – as the only tangible measure – a new monetary policy programme of the ECB, the so-called OMT, or Outright Monetary Transactions. This allows the euro system to make unlimited purchases of short-term bonds from euro area countries.

The following chart shows how many trillions of euros have been committed to this programme since then.

Diagram 2: Funds used by the ECB under the OMT programme

No, there's no error in the chart. In fact, this instrument has not been used so far. However, it can be assumed that the mere announcement of the possibility of unconditional bond purchases had a calming effect on the financial markets in the past. The current President of the European Central Bank, Christine Lagarde, is hoping for a similar effect when a new programme to address the risks of fragmentation (Transmission Protection Instrument, TPI) is announced.

Mario Draghi thus eliminated the debt crisis for at least 10 years, partly as a result of a mere utterance. This is a notable example of creativity on the part of central banks.

With all the creative changes in direction and additions to the toolbox, the central banks do not always take past principles and announcements very seriously. This is what the second thesis addresses:

2. No central banker is interested in “what was said yesterday”

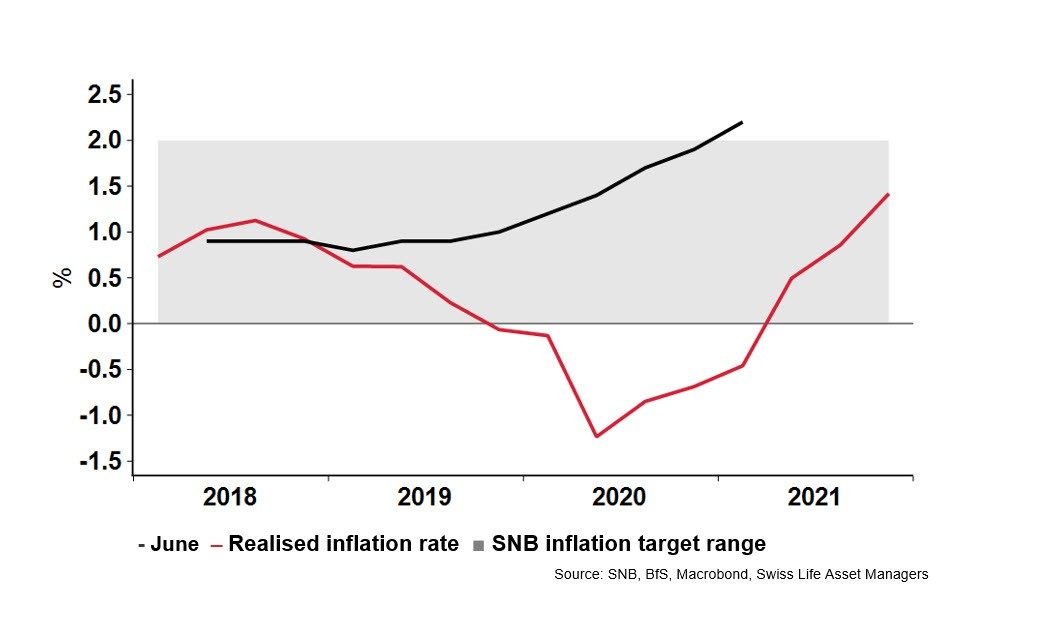

The Swiss National Bank, the ECB and Sweden’s Riksbank regularly publish inflation forecasts. The SNB explicitly calls its forecast a “conditional” inflation forecast and believes that it should materialise over the next three years as long as the bank leaves its key interest rates unchanged.

Diagram 3: SNB conditional inflation forecast

The above chart shows the SNB’s conditional inflation forecast from June 2018. This projection indicated that inflation would rise above 2% in 2020.

The SNB defines price stability as the maintaining of an inflation rate between zero and 2%. According to its own strategy, it should have started to tighten monetary policy slightly between 2018 and 2020. However, this was not of much interest to the SNB as the appreciation of the Swiss franc helped to avoid having to take account of “what was said yesterday”.

Those who look at the red line will say: rightly so. The inflation rate in Switzerland did not rise in the years after 2018: on the contrary, the country has experienced a period of deflation against the backdrop of the pandemic.

“When the facts change, I change my mind. What do you do, sir?” This motto, which is attributed, depending on the source, to John Maynard Keynes or Paul Samuelson, is also used by central bankers. In a more striking way, central banks often go with the flow.

There are other recent examples of central bank pronouncements with a short half-life: In 2014, Thomas Jordan warned of deflation in the event of an appreciation of the Swiss franc, making the minimum exchange rate indispensable. On 15 January 2015, he expected the economy to have exactly the same experience for two years.

Prior to the pandemic, fears increased on the markets that interest rates would not remain low for all eternity.

As inflation gradually approached the 2% target again, the US Federal Reserve announced a shift away from its previous asymmetric inflation target. Rather, higher inflation would not lead to an immediate rise in key interest rates provided that a long-term average inflation rate was significantly below 2%. The current inflation environment has probably already rendered this change of course obsolete again.

Christine Lagarde, for her part, stated in March 2020, i.e. in the midst of the worst phase of the pandemic, that it is not the ECB’s job to lower the risk premium on Italian government bonds. At the latest since the recent debate on the ECB's new anti-fragmentation programme, we have all been reminded that Mario Draghi implicitly made exactly that promise ten years ago.

This brings us to the third thesis, namely the independence of monetary policy from the fiscal policy of a country or of the member countries of a monetary union:

3. The blending of monetary and fiscal policy is a fact

The thesis that central banks’ independence is at risk can be measured by the seriousness with which they are tackling the inflationary pressures of the past 12 months.

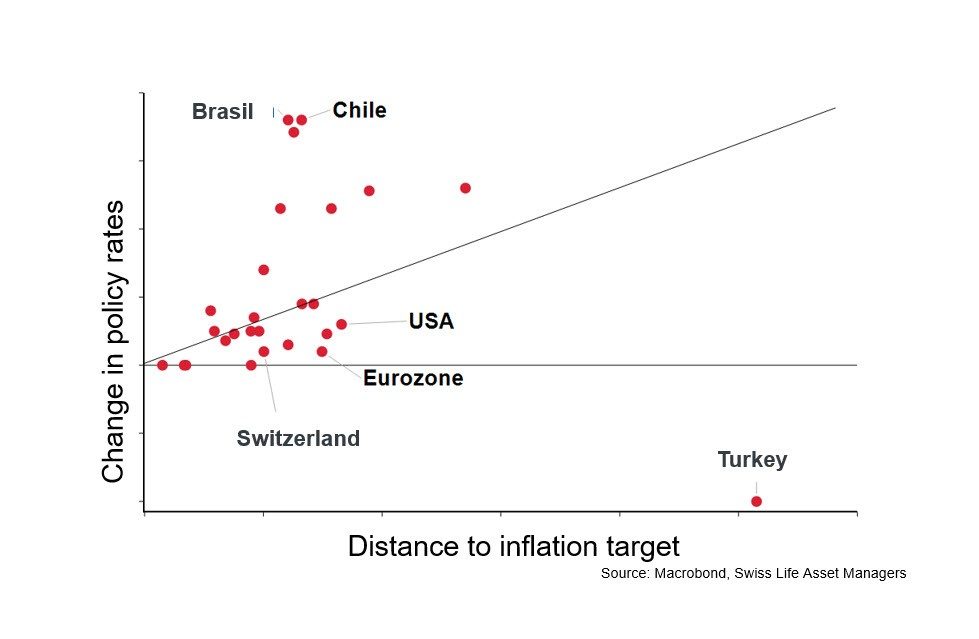

We investigated the behaviour of 27 central banks around the world, all of which have set themselves an inflation target.

If the inflation observed in the diagram below overshoots the target of the respective central bank – i.e. far to the right on the horizontal axis – then the central bank would have to raise its key interest rates significantly.

So, depending on the deviation of inflation from the inflation target, a country’s change in key interest rates might have to follow a line at an angle of 45%.

The result is a diffuse picture. Despite high inflation, a large group of central banks have not yet moved much.

Diagram 4: How are the central banks reacting to the rise in inflation?

It is probably not surprising that Turkey's central bank does not pursue an independent monetary policy. On the other hand, it is perhaps surprising that Brazil's central bank is counteracting inflation so strongly.

The ECB has also budged slightly with the interest rate hike of 21 July 2022. Overall, however, the eurozone, the US and Switzerland have been rather hesitant in fighting inflation.

Thus, the thesis that monetary and fiscal policy are becoming increasingly mixed seems to be borne out, at least for advanced economies.

How did this happen?

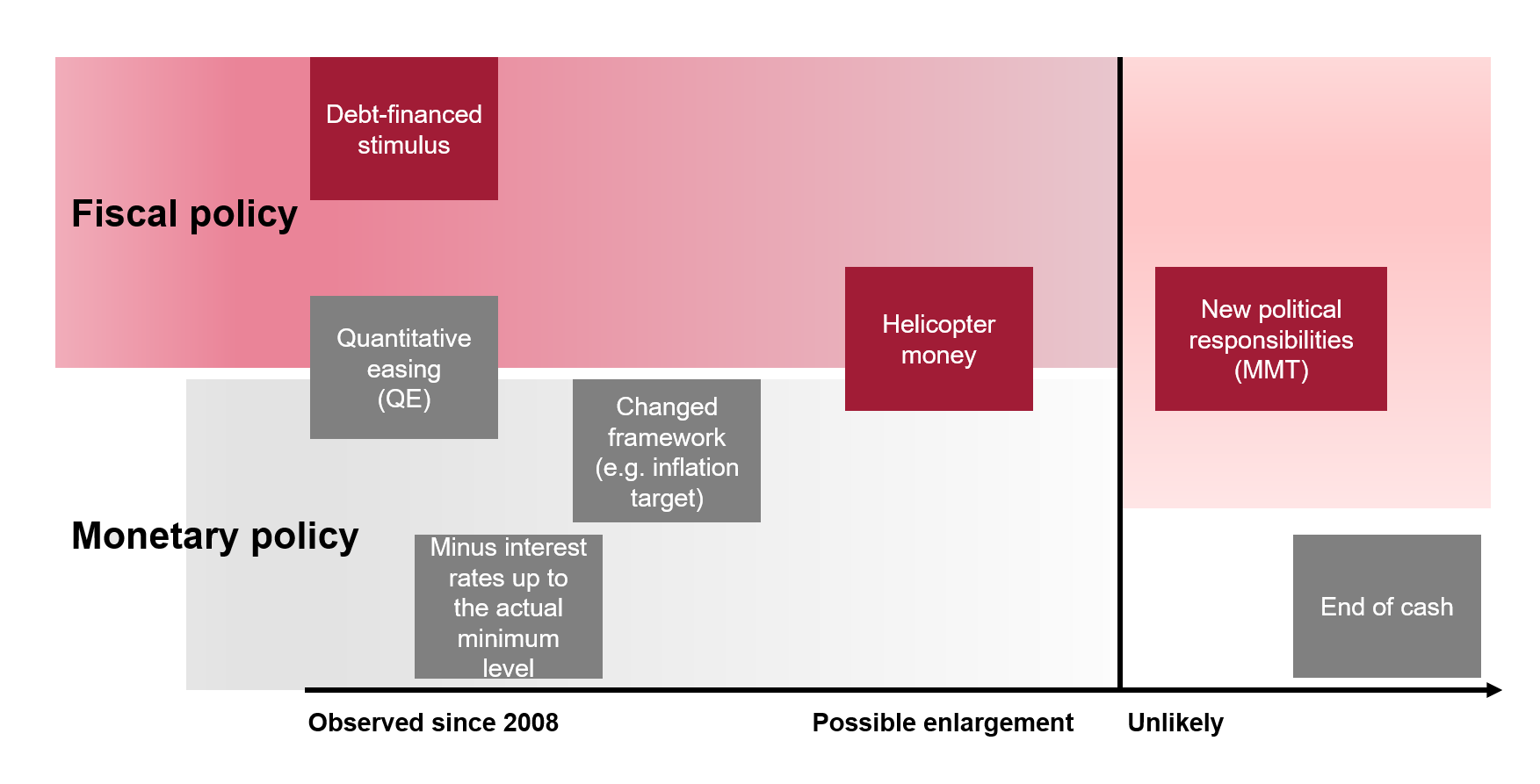

At the latest since the financial crisis of 2008, the demarcation between monetary and fiscal policy has become unclear. The central banks use their balance sheets for unconventional monetary policy measures and thus exert an influence on the interest rate framework along the entire yield curve.

With the quantitative easing of monetary policy, they therefore cap the nominal interest rates at which countries can borrow on the market for a very long time.

Diagram 5: Blending monetary and fiscal policy

With the onset of the pandemic, for example, the Bank of England switched to entering government bonds directly on its balance sheet instead of taking the previous detour via the secondary market. And many central banks also toyed with the possibility of using “helicopter money”.

The central banks thus expose themselves to the accusation of being party to “financial repression”. This refers to a package of regulatory and monetary policy measures designed to ensure that governments find investors for their debt securities and that the interest burden on these debts remains as low as possible – or even negative – in real terms.

But despite all the criticism, it was not only during the subprime crisis in the USA and the debt crisis in Europe that the Fed and the ECB were at times the only bodies capable of acting to prevent the collapse of the financial system or the euro through creative measures. Even when the pandemic broke out, it was again the central banks that communicated economic support measures first – and did so resolutely.

There is a downside to the central banks’ success in these crises since 2008: central bankers have fallen victim to their own success. They have been in the spotlight ever since. Their ability to solve economic problems is now seen by some stakeholders as almost infinite. As a result, demands on the central banks have increased.

And so this brings us to the fourth thesis:

4. Monetary policy continues to be misused

My first hypothesis that central banks’ creativity is inexhaustible, and the evidence to date that central banks may have fallen victim to their own success, suggest that we haven’t seen it all yet.

The provisions relating to the European System of Central Banks, annexed to the Treaty on European Union, provide for the following:

“In accordance with Articles 127(1) and 282(2) of the Treaty on the Functioning of the European Union, the primary objective of the European System of Central Banks ESCB shall be to maintain price stability. Without prejudice to the objective of price stability, the ESCB shall support the general economic policies in the Union with a view to contributing to the achievement of the objectives of the Union as set out in Article 3 of the Treaty on European Union.”

It was always envisaged that the ECB should support programmes such as the EU Green Deal to achieve climate neutrality by 2050.

Despite the urgency of the EU’s objective, it seems justified to speak of a misappropriation of the initial monetary policy.

But the SNB is also confronted with ever-changing demands. Influencing the way it manages its balance sheet is still comparatively harmless. More problematic are ideas such as creating a sovereign wealth fund with SNB funds or the proposals that the pension system should be restructured with SNB funds.

While an unlimited money press may seem attractive to solve otherwise complex political problems, policymakers must ensure that central banks continue to fulfil their initial mandate. Our monetary system is based on a credible, effective (and sometimes creative) monetary policy aimed at price stability. As long as this remains so, I can present my fifth and final thesis:

5. The only digital money with a future is the “central bank coin”

One device from the toolbox of financial repression is the prohibition of flight from the regulated FIAT monetary system. This will prevent the emergence of a parallel currency. In the last century, between 1933 and 1974, US citizens were forbidden to hold physical gold. From 1961 onwards, the prohibition also applied to the possession of gold abroad.

While the focus in the last century was on this physical currency substitute, today the focus is on digital competitor products.

Cryptocurrencies, especially Bitcoin, are often promoted on the grounds that they offer security against high inflation and, more so, against the collapse of the central bank monetary system, which is purportedly built on sand. Whether they really do this is doubtful, particularly based on the experience of the first half of 2022. It is not a question of whether the rules of a private currency are more transparent or more democratic than the rules of the currency that is protected by our traditional currency guardians. I'm getting at something else. If my fifth thesis is correct, central banks and supervisory authorities will do two things with regard to digital currencies in the coming years:

Firstly, they will continue to push the regulation of crypto money. Let's look at India: there, every transaction involving a cryptocurrency is fed back into the regular financial system subject to 30% tax. The instruments of financial repression remain as effective in the crypto age as they were when holding gold was forbidden.

Secondly, work continues on the introduction of the digital central bank coin. The central banks have also recognised that the future belongs to digital money. Hundreds of millions of people do not have access to a bank account. For them, digital applications are a way of participating in a financial system, including access to loans. Now central banks are testing the issue of digital central bank money.

Projects in China and Sweden are already far advanced.

These applications are very likely to make use of blockchain technology. As with previous quantum leaps in technology, a distinction must be made between the infrastructure and the ways in which it is used. With the railways and the Internet, the infrastructure came to stay. Nevertheless, many pioneers who built the tracks and created the World Wide Web have gone bankrupt. Similar things will be said in the future about the blockchain and the first forms of digital currency.

So maybe everyone is right: those who consider the days of cash to be numbered, as well as those who consider the Bitcoin worthless.

In any event – and this concludes the first hypothesis – we should never underestimate the creativity of central banks when it comes to digital money.

Finally, I would like to take a look back to ten years ago and come back to Mario Draghi's speech in London.

Yes, it’s true that we all remember the promise "Whatever it takes". However, from today's perspective, and in the debate about the future behaviour of central banks, what Mario Draghi said in the next sentence is possibly even more important. He added the following words to his promise: "And believe me, it will be enough."