Green bonds promise environmental impact alongside financial returns. But how can investors be sure those promises hold up? At Swiss Life Asset Managers, green bonds are put through a rigorous ESG review process designed to test credibility, transparency and real-world impact.

Our ESG approach in securities combines product integrity, ESG-integrated credit analysis and active ownership. This is especially visible in green bonds, where we assess not only the use of proceeds, but also the issuer’s broader transition credibility, climate commitments, and relevance for clients’ sustainability preferences.

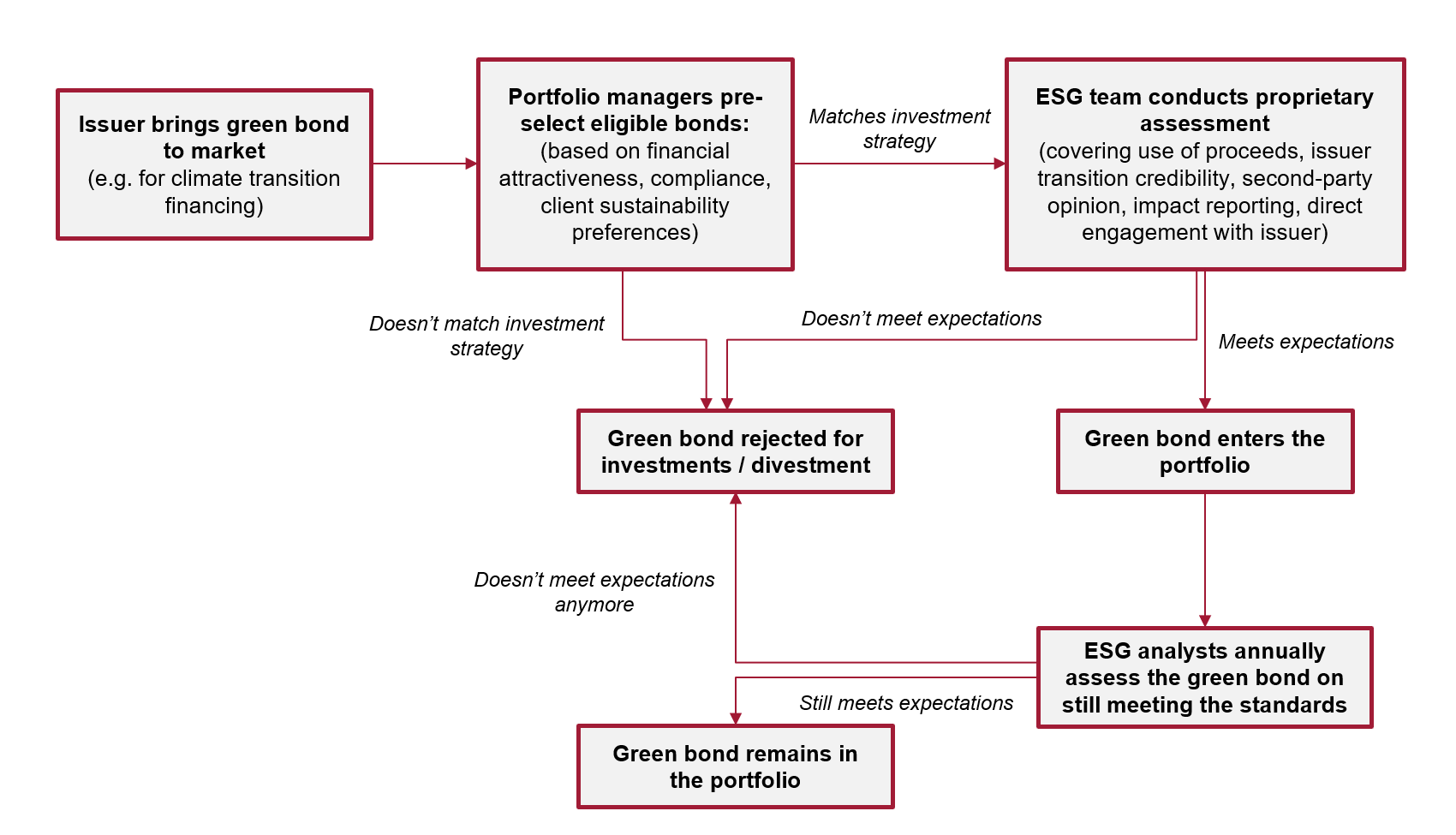

The portfolio managers and the ESG teams of Swiss Life Asset Managers defined a common process for the review of green bonds. Before investing through the dedicated fund, the ESG team systematically analyses instruments that are financially attractive and rulebook-compliant according to the portfolio managers.

This ensures alignment with the client’s preferences while safeguarding product integrity.

The ESG analyst in charge of the review can rely on documents made publicly available by the issuer: green bond framework, second-party opinion, allocation and impact report, if the green bond is older than one year. The ESG analyst may also contact the issuer to obtain additional information on a case-by-case basis.

All assessments are carried out using a proprietary grid analysis to ensure consistency and comparability.

Every green bond goes through the analysis process

Source: Swiss Life Asset Managers, 2026

The objective of the review is clear: to confirm the quality of the green bond, and to determine its eligibility for the portfolio. Since the introduction of this process, the ESG team has analysed more than 400 bonds. Close to 15% of them were not approved.

When green bonds don’t meet expectations

Negative reviews occur when critical criteria are not met. One key focus is the nature of the projects financed through bond proceeds. If some project categories do not show clear environmental benefits,

the green bond can be rejected. To assess these benefits, we usually refer to recognised standards, such

as the Climate Bond Taxonomy and the European Union Taxonomy that was launched in 2021.

This disciplined approach has led us to abstain from specific issuances. For example, a bond aimed at financing the installation of 5G telecommunication networks showed a potentially overall negative

carbon impact under the analysis.

This discipline also extends beyond the initial assessment. After the issuance, we had to divest a few

green bonds in cases where major requirements were no longer met, for example when a significant

portion of proceeds remained unallocated after two or three years or when no external audit of fund allocation was available.

Who passes the assessment?

The impact key performance indicators (KPIs) provided by the issuer are other decisive factors. The

best practices include relevant KPIs – such as CO2 emissions avoided, green electricity produced, or

waste treated – supported by transparent methodologies and third-party verification. The information

about such impacts is helpful for investors in order to compare green bonds and to report to the end

clients.

It further helps us build a better understanding of the climate risks and opportunities of our investments

and assess issuers’ climate transition efforts, which belong to our responsibleinvestment focus areas.

The following companies are examples of good practices that passed our assessment.

Iberdrola

The Spanish utility Iberdrola is one of the largest private issuers of green bonds worldwide.

The company has invested more than 140 billion euros in the energy transition since 2000 in order to support the increasing electrification of the global economy. This commitment remains in place: over

90% of its planned investments for 2025-2028 will be aligned with the European Union Taxonomy.

A substantial part of these investments is financed via the issuance of green bonds.

ABN AMRO

The Dutch bank ABN AMRO has been active in green bond issuances since 2015. The proceeds are

mainly used to finance and/or refinance loans related to green residential buildings. Based on ABN

AMRO’s definition, green residential buildings are houses or apartments with either an EPC energy

label “A” or energy demand at least 10% below the Dutch Nearly Zero Energy Building threshold. The

issuer provides transparent annual allocation and impact reports, including reduction in energy use

and avoided CO2 emissions, which are externally reviewed. Improving the efficiency of buildings is

key to mitigating climate change, as buildings account for around 30% of global energy demand.

Ayvens

Ayvens provides mobility solutions in more than 40 countries, with full-service leasing and fleet management as its main products. The company issued its first green bond in 2018 to finance the development of greener fleets with battery electric vehicles, which produce zero tailpipe emissions during use and accounted for 32% of its total deliveries in Europe in 2025. Ayvens publishes transparent impact KPIs, in particular avoided CO2 emissions.

Supporting transition through disciplined flexibility

The ESG rules may be more flexible for a green bond than a standard bond. While equities or standard

bonds issued by an oil and gas company are typically excluded from impact funds, a green bond issued

by the same company may be eligible. However, only provided they align with a credible transition

strategy and demonstrate a genuine ambition to transform its activities over time.

In this way, investing in green bonds is contributing to the short- and long-term transition of some sectors. Electricity utilities are the most active issuers in the green bond market among corporate bonds – they represented around 15% of all ESG bonds issued in 2025 and certainly more for green bonds only. They

used green bonds to increase renewable capacities and decarbonise their energy production mix.

Q&A

Like any bond, a green bond can be issued by all types of organisations, a corporation, a financial institution or a government, to raise capital from investors to finance its activities. But there is something special for green bonds: the issuer commits to use the proceeds that are raised for specific projects with environmental benefits, e.g., to develop renewable energy power plants, to build new waste management facilities, to create new clean transportation infrastructure or to implement energy efficiency projects.

Green bonds used to enjoy a pricing advantage compared to plain vanilla bonds, called a “greenium”. Driven by a strong investor appetite and a relatively limited volume, this premium gradually faded as issuance increased and pricing converged between bonds. The green bond market became as liquid as the overall bond market. In terms of performance, the green bonds have outperformed the average credit market, based on our recent observations. However, it is not driven by the specificities of green instruments, but more by its market structure. Sectors that are particularly dynamic in issuing green bonds – like financials and utilities – have tended to be rewarded more than standard indices.

Green bonds offer some added value for investors who want to support the transition to a low-carbon economy, via listed markets. By showing demand for such products, investors canencourage issuers to increase their efforts and investments towards environment-friendlyprojects. Compared to standard bonds, green bonds also provide greater transparency, as the useof proceeds is documented in dedicated reports.

Thanks to the Green Bond Principles defined by ICMA in 2014, almost all green bonds now followadvanced practices in terms of design and documentation. Nevertheless, some attention isrequired. Green bonds are often self-declared as “green” by issuers, proceeds are usually onlyearmarked rather than ring-fenced and the quality of audits can vary. It is therefore essential tocheck whether a green bond genuinely delivers environmental benefits and is in line with theissuer’s long-term transition strategy.

Our ESG strategy

Our approach to sustainable finance goes beyond complying with current standards. Where possible, we aim to deliver tangible value through proprietary data insights, measurable climate actions and active engagement.