Donald Trump’s announcements on 2 April following “Liberation Day” hit the markets hard, especially the dollar and US treasuries. In times of ongoing uncertainty, a sound analysis is needed to assess the impact on the hospitality industry and the hotel sector in general.

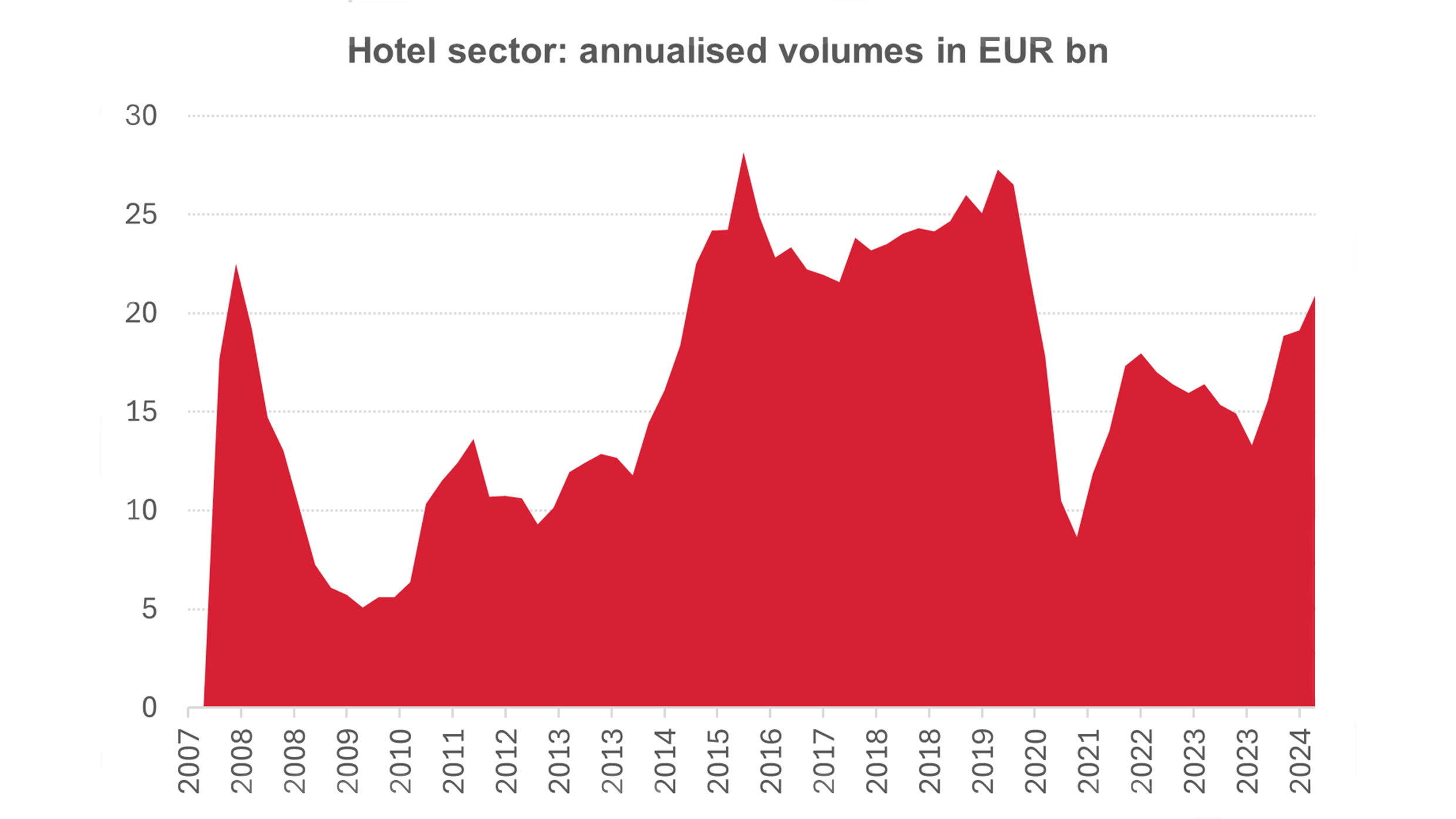

As a reminder, in 2024 transaction volumes in the European hotel sector amounted to EUR 20 billion compared with EUR 13 billion in 2023, an increase of 25% compared with their long-term average since 2008. Unsurprisingly, the most successful geographical areas are France, Spain and Italy (34% of hotel investment in 2024) thanks to various popular destinations, particularly since the acceleration of inter-European travel.

Our view: no change on the horizon in terms of medium and long-term performance of the sector despite the headwinds at the start of 2025.

Hospitality in an era of Trumpism and tariffs

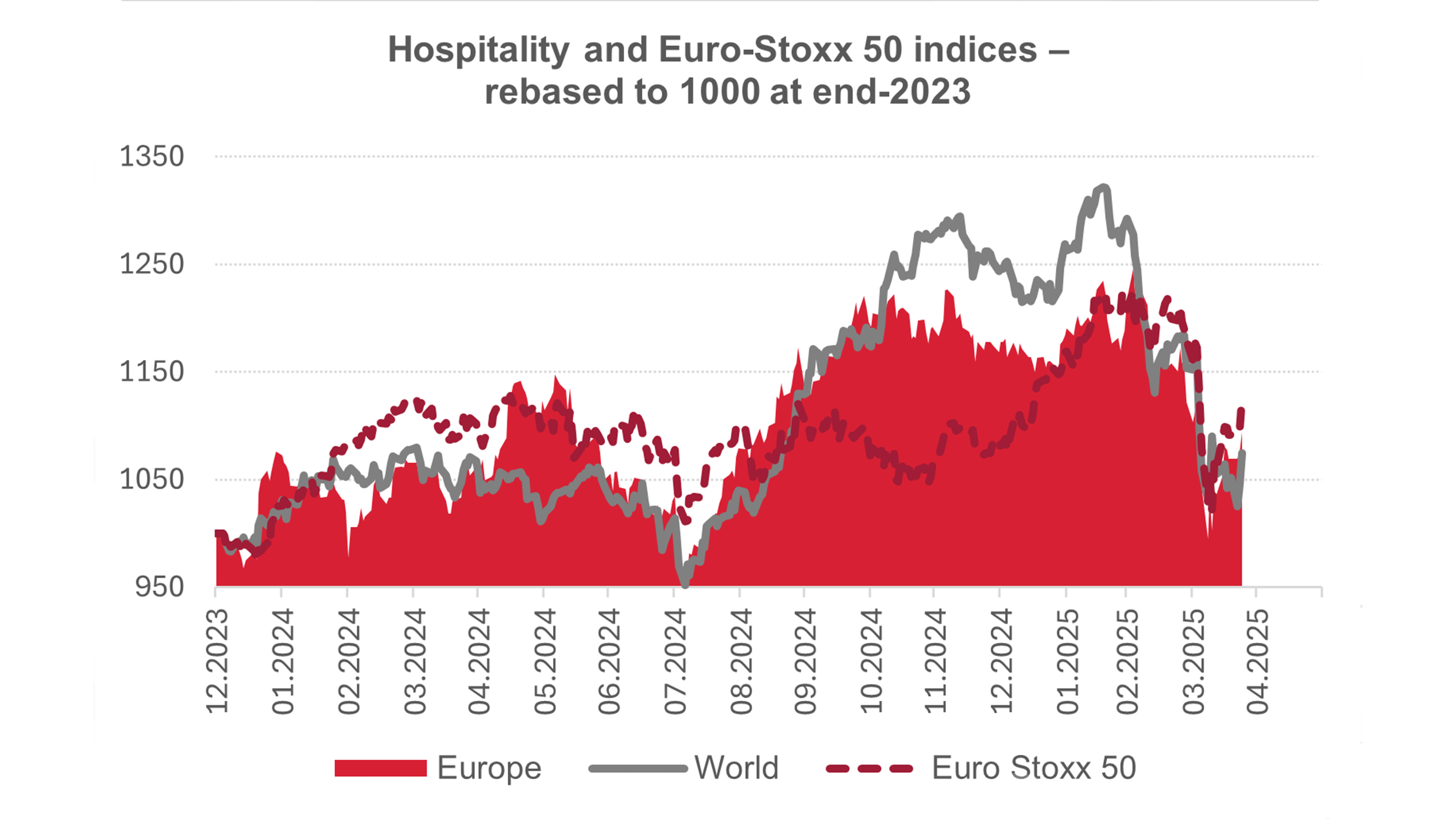

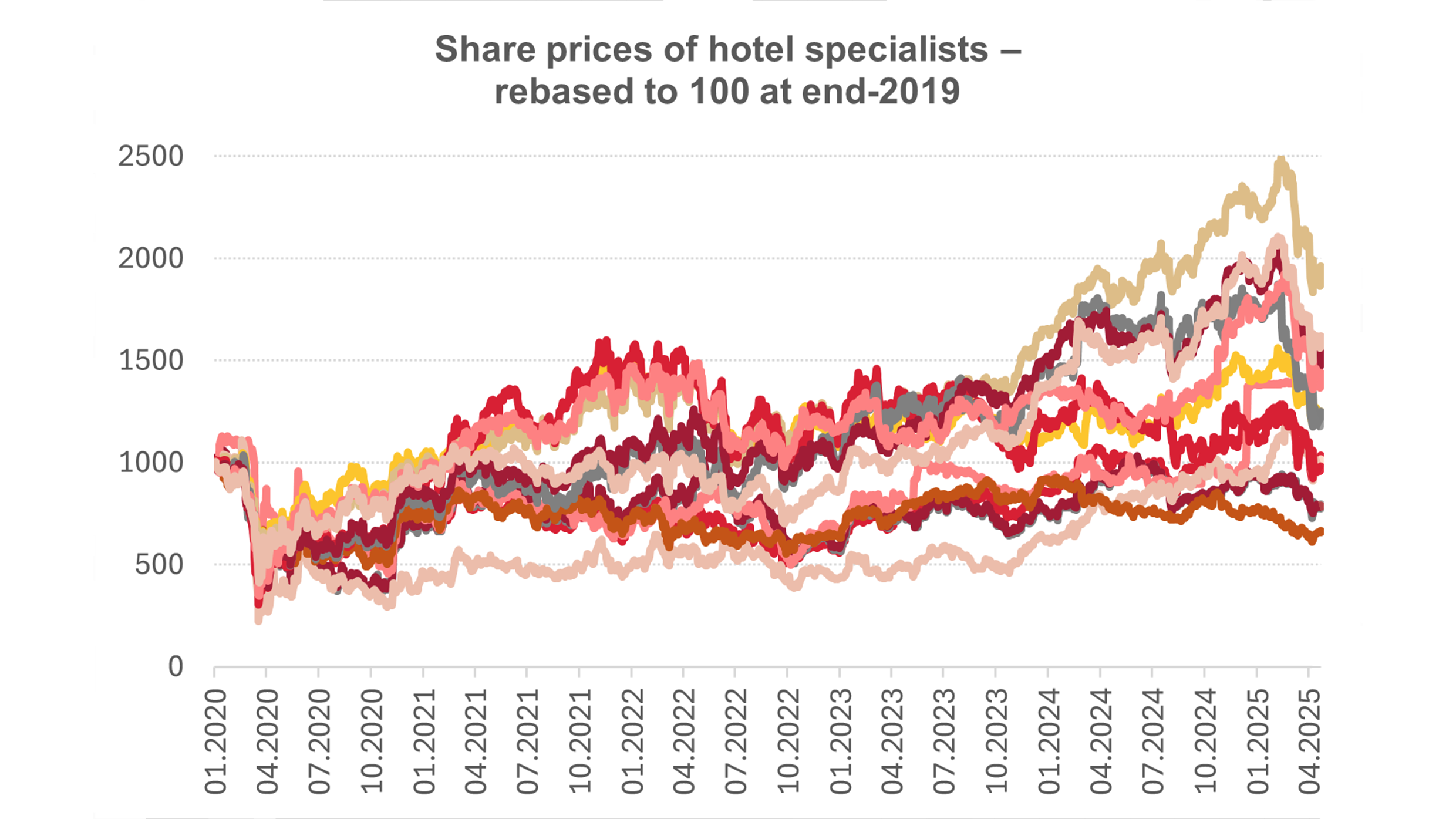

As a reminder, in 2024 the MSCI hospitality index, which is broader than the hotel sector alone, outperformed the Euro Stoxx 50 index (+17.8% versus +8.2%) in view of the good operating results of all specialists. In the hotel segment, European operators – such as Accor, Covivio, Hotelim, Hotel Baverez, Lamp, Mhp, Mélia, Minor and Scandic – saw their share prices rise between 8% and 50%.

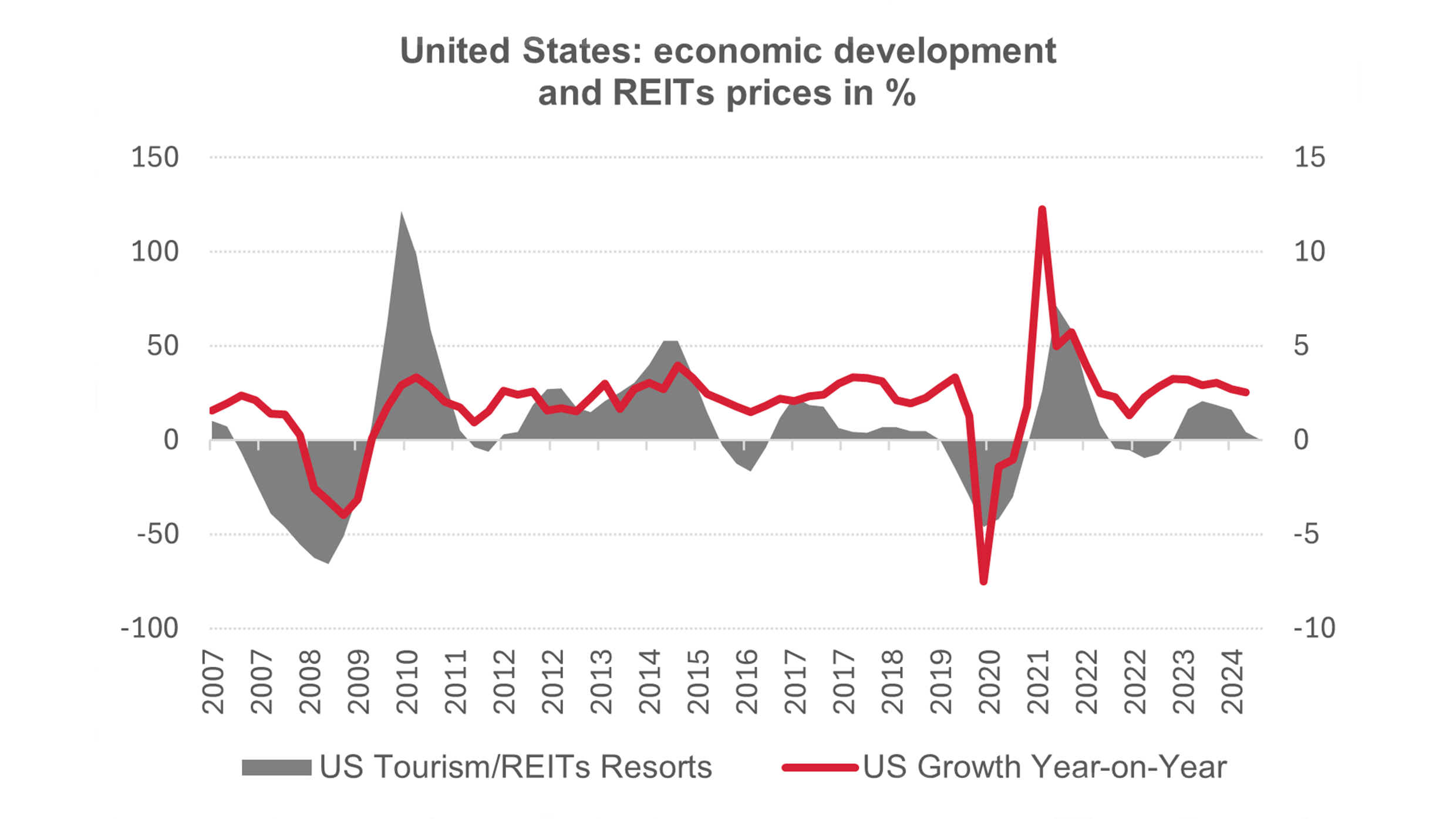

What can we say about the trends that have emerged since the tariff announcements? Admittedly, the US REITs indices recovered after deals were made with the UK and China, but the index is down by almost a third (21.2%) since the beginning of the year, while the European hospitality index is faring much better. This difference in appreciation between Europe and the United States could be explained by investors’ distrust about the potential of US growth in 2025 and its negative impact on tourism in the US in the event of a recession: over a long period there is indeed a correlation of 0.58 between the indices of REITs specialising in leisure and US economic growth.

Our view: the American hotel industry will suffer much more than the European hotel industry from Trump’s tariffs and isolationism, through a slowdown in US growth that will weigh on the purchasing power of US households.

The European hotel industry and the advantage of diversification

In Europe, a few trends are emerging in terms of operators’ share prices: those with predominantly European exposure appear to be more resilient. Investors anticipate that the tariffs imposed by the United States will not directly affect tourism in Europe, given the regionalisation of trade as the analysis below suggests.

Europe is the world’s leading tourist destination with nearly 1.8 billion overnight hotel stays. Structurally, the European hotel industry continues to strike a good balance between domestic (50%) and foreign (50%) tourism, although the distribution by country varies considerably, as shown in the graph below. This foreign demand is characterised by inter-European flows of 33%, which are relatively well diversified between the different regions.

Our view: strength through unity, beyond political boundaries – Europe’s tourism is a single, indivisible entity for European citizens. Europe is the leading destination for Europeans and not just the leading destination for global tourism.

The European hotel industry and American clientele

American tourists account for less than 4% of all non-European tourists in Europe: they are highly concentrated in Italy (19%), Spain (12%), France (11%), Germany (7%), Ireland (6.2%) and to a lesser extent in Greece (5.6%), Portugal (4.6%) and the Netherlands (4%). However, US tourism has grown very strongly over the past two years, with the number of overnight stays much higher than in 2019: +68% in Portugal, +46% in Greece, +27% in Italy, +18% in Spain, +17% in the Netherlands, to name but a few. For these destinations, the risk of a smaller American clientele is very real and the concerns are legitimate.

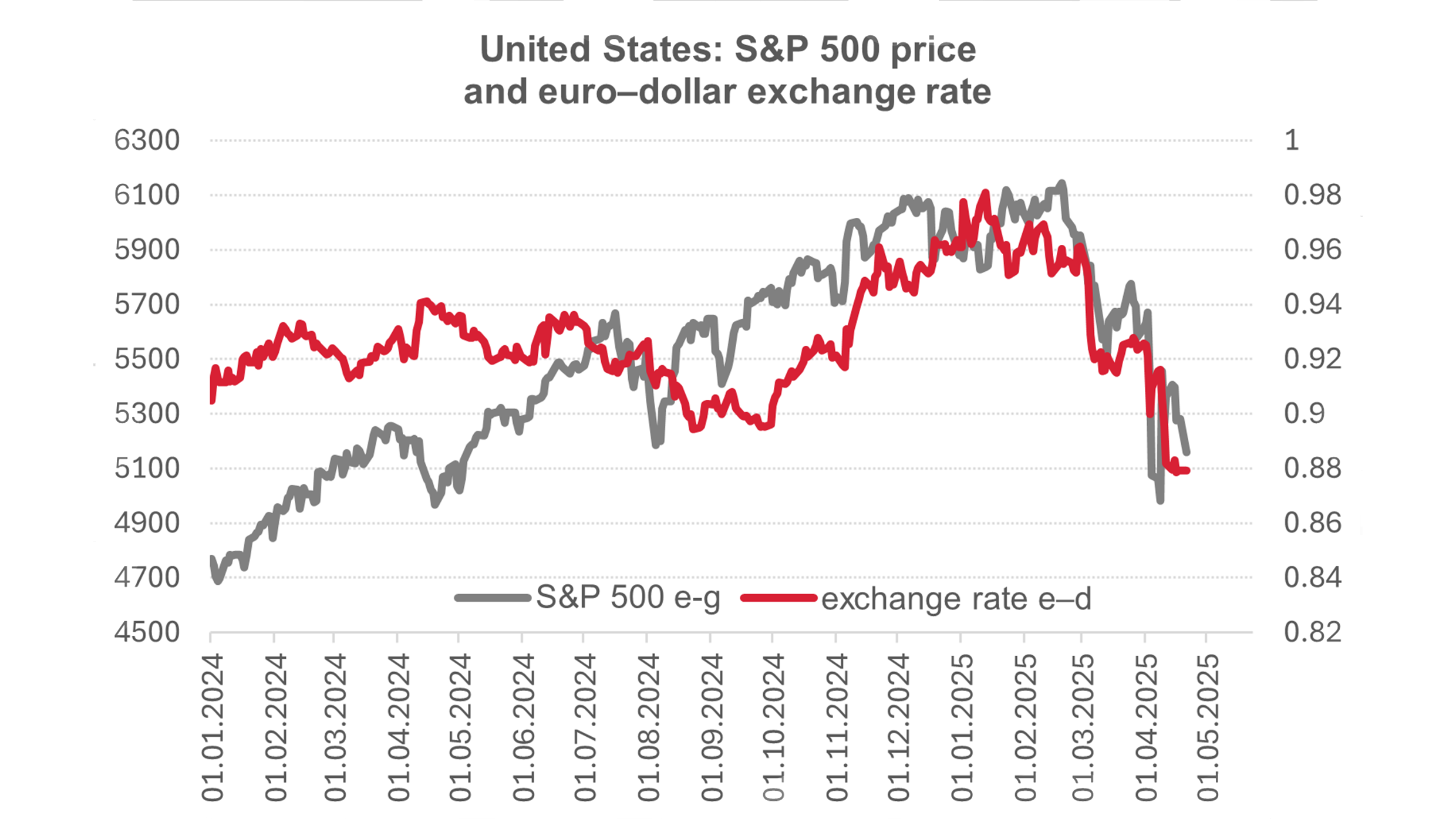

In terms of hotel footfall, leisure stays by Americans are mainly concentrated in rather high-end segments; an analysis of long-term data suggests a positive relationship between growth in stays in Europe and the appreciation of the US dollar against the euro. Moreover, the depreciation of the dollar against the euro

(–10% since January 2025) combined with a decline in the financial wealth of US households (–16% of the S&P 500) would negatively impact occupancy rates of high-end hotels, as suggested by an econometric analysis. More specifically, the exchange rate elasticity of overnight stays is all the greater the higher the reference price of the room or the cost of living: in other words, the high-end hotel segment in France and Italy would be more impacted than the high-end hotel segment in Spain or Portugal. The underlying factor behind this lower price elasticity in Spain and Portugal can be explained by the better value for money offered by these two destinations, beyond accommodation and climate. As for stays in the very high-end segment (“palaces”, luxury five-star hotels and similar classifications), the exchange rate elasticity would be relatively low compared to the average price paid for a suite.

The introduction of tariffs could have a more negative impact on business demand in France and Italy, where trade relations are stronger with the United States.

Our view: the lack of American customers would have a chilling effect on some destinations. However, by adopting a proactive and pragmatic approach, operators could manage their revenue per available room (RevPAR) by lowering their average price and increasing their occupancy rate in 2025, all other things being equal, to capture a more affluent European population.

Sources of the graphs data: RCA, Bloomberg, Swiss Life Asset Managers