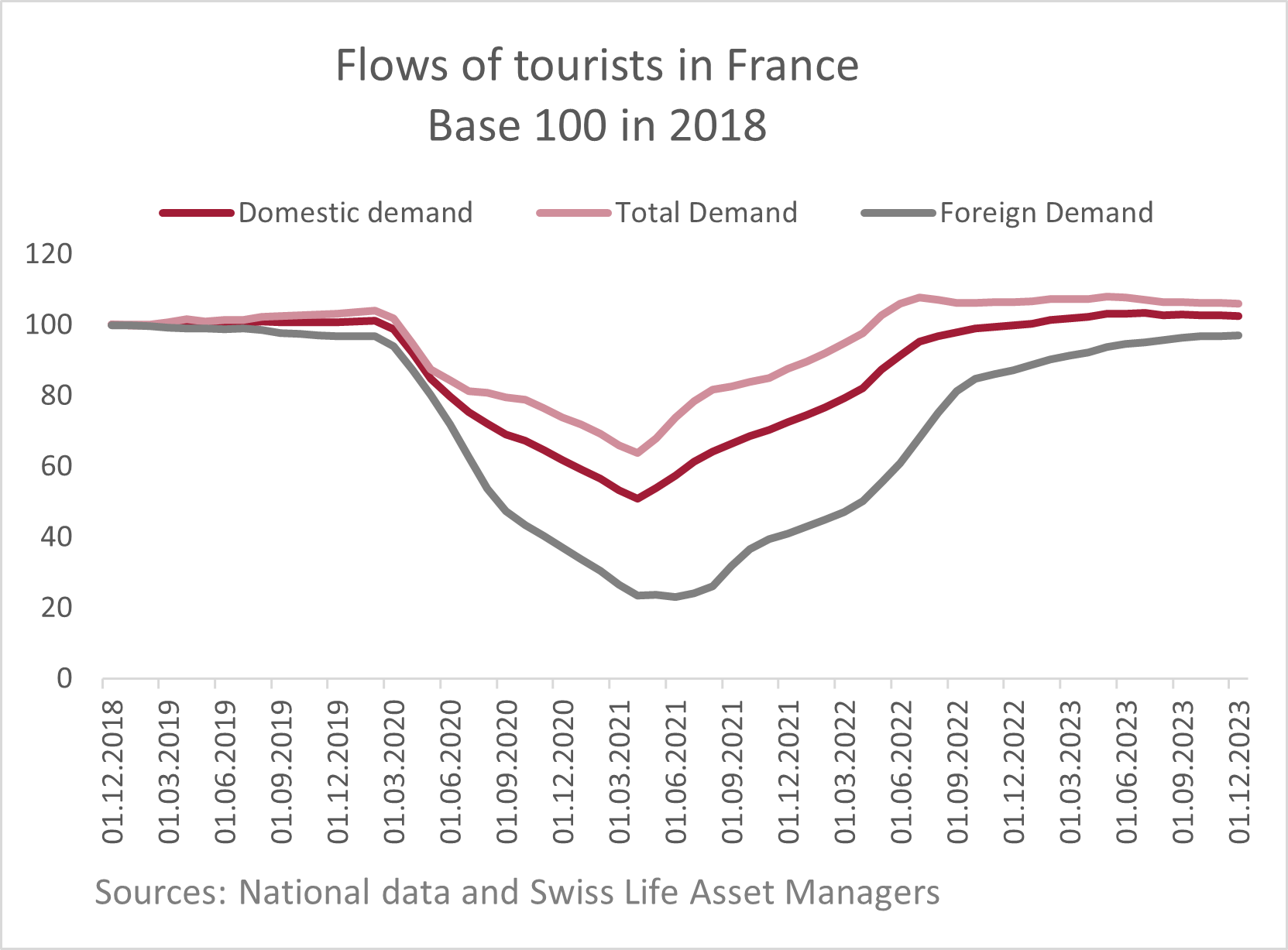

France, one of the world's leading travel destinations, has demonstrated strong resilience since the health crisis by turning headwinds into tailwinds in term of demand expectations. In 2023, the French hospitality sector once again recorded exceptional performances.

These exceptional performances were strengthened by both domestic and international demand. According to In-Extenso's data, available last February, the occupancy rate in 2023 increased by 3% compared to 2022 with the average daily rate up by 7%.

Key metrics in a healthy shape

Despite an inflationary and slowing economic environment, many French locations and segments recorded healthy performances. One key metric, accommodation revenue (RevPAR) in France, was up by 10% year-on-year, and more than 19% compared to its 2019 level.

In 2023, performance in terms of average price by type remains positive across segments: a deep dive suggests that disparities in term of performance narrowed compared to 20221. Occupancy rates were also on the rise from their level in 2022, ranging from +1% to +5% with still significant differences between luxury and super-economy hotels. A notable highlight was related to revenues, which continued to rise at a sustained pace: +12% in the high-end and luxury segments compared to +13% in 2022, +11% in the midscale segment against +8%, +7% in the economy segment against +9%. As the cherry on the cake, the super-economy segment recorded an increase of 10% compared to 1% in 2022: such a bounce-back was driven by the rugby effect as well as rising demand from travellers who needed to save money in a tougher environment. More generally, research shows that in recessionary times, the super-economy and the economy segments stay ahead: tourists prefer to spend less on accommodation rather than abstain from travel completely.

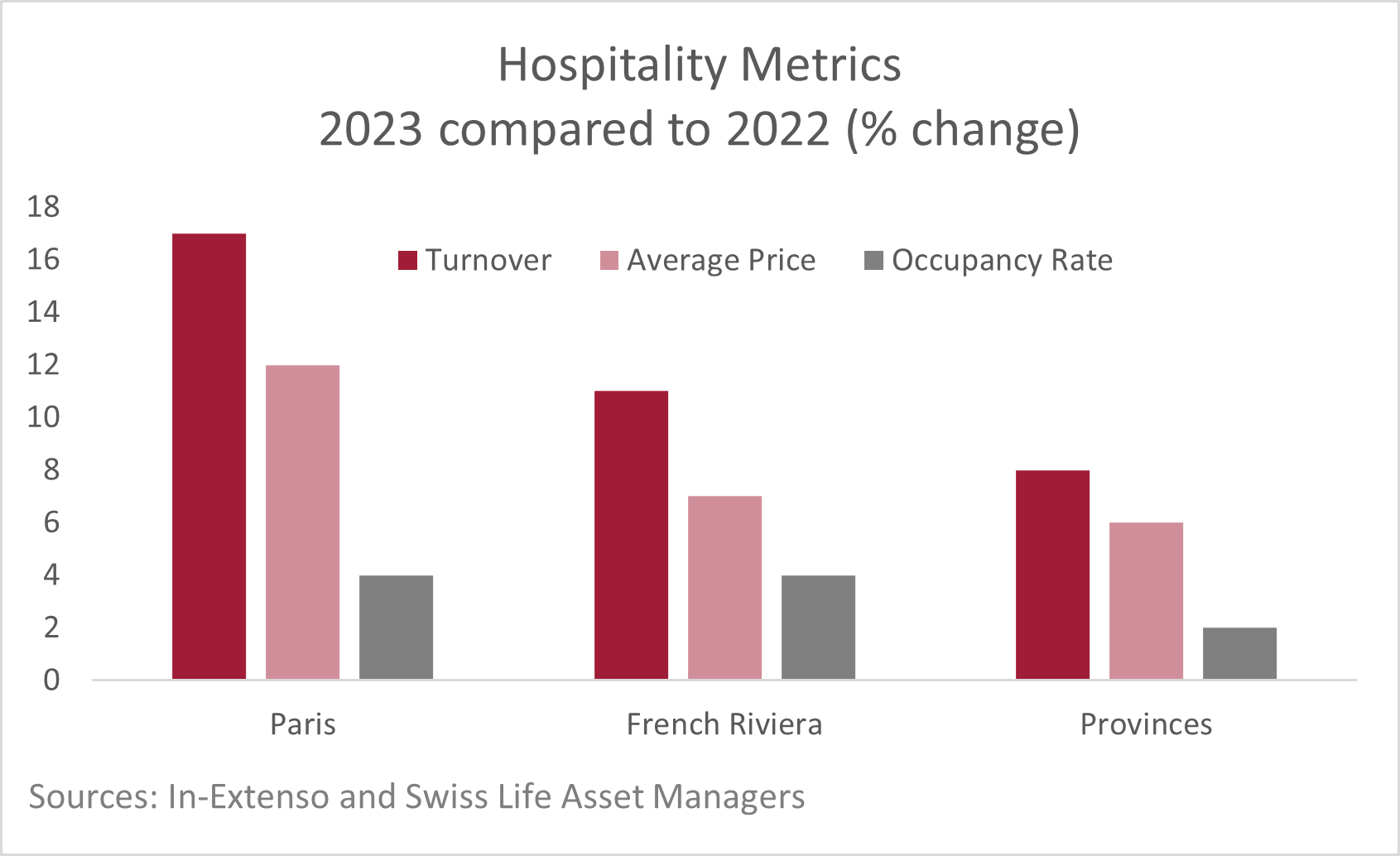

In 2023, the increase in turnover was faster in Paris (+17% against +18%), sustained by both the World Rugby Cup and long weekends for couples. Turnover growth was also notable on the Côte d'Azur (+11% against +18%) as well as in the provinces (+8% against 7%): this was the result of healthy cross-border and international demand. A euro-dollar parity favourable to American tourists usually benefits the high-end and luxury segments: this was also the case in 2023.

Key strategic trends

Beyond such benign figures, it is crucial to understand the trend in order to appraise the sector's potential in the medium and long term. Firstly, the French hotel industry has been very agile in adapting itself to the new requirements of demand, lifestyle, bleisure but also eco-responsibility. Structural changes, including hybrid working, have favoured the sector through more frequent stays, which ultimately improved occupancy rates thanks also to stronger demand from domestic and European travellers. This new behaviour dynamic has smoothed out the traditional seasonal peaks observed in the past. Other major changes, including geopolitical risks and the climate transition, are now encouraging more intra-European tourist flows: France, Spain and Italy are the big winners of such megatrends, although this trio has always been in the champion’s league in terms of arrivals and overnight stays.

On the transaction market, despite a sharp slowdown in volumes as seen in other markets, the appetite for the French hotel market has not dried up. In 2023, institutional investors were keener to acquire small lines rather than portfolios in a context of both product scarcity and the rising cost of financing. A sea change compared to past acquisitions is the strong presence of international investors, sovereign wealth funds and pension funds keen to position themselves in a sector deemed to have solid long-term fundamentals: more intra-European demand, a very diversified offer (in terms of number of keys, ranges, locations) and a more constrained market in terms of pipeline compared to other European countries. The possibility to combine different risk profiles across locations is in line with a diversification strategy.

In total, according to JLL data, EUR 2.2 billion was traded in hotels in France, the same level as in 2022, i.e. 18% of the total volume, EUR 12 billion of transactions, recorded in commercial real estate over the year. In retrospect, such a level is in line with the 10-year average: with the exception of 2020, the year of the pandemic, the lack of products has usually explained the volatility of investment volumes in France.

A new strategy is also observed: management contracts have become increasingly prevalent compared to traditional lease contracts. Investors are aware that such a strategy, which involves sharing a hotel’s trading profit, helps boost overall performance and ensure attractive returns for their overall real estate portfolio. It is obvious that in a context in which interest rates that are remaining higher than in the past decade, the generation of income in addition to indexation will be particularly popular. As a consequence, the premium in capitalisation rates between lease and management contracts has narrowed. Although the rise in cap rates has been noticed, following the rise in long-term interest rates, the average outward yield shift in the sector was much limited compared to more traditional sectors, such as office or logistics.

The Olympic Games are set to make 2024 a new vintage year for hospitality in France. However, this sector is set to become a mainstream asset class given its ability to be an income-producing sector that is highly protected by strong regulation.

1The upscale and luxury markets recorded a new rise in the average daily rate of +7% against +27% compared to the 2019 level; the midscale observed a rise of 8% (against 15% in 2022 compared to 2019): +7% for economy (against 10% in 2022) while the super-economy average daily rate rose by +9% (11% in 2022 compared to 2019).