An altered UK economy means property investment strategies need to be reassessed. Amid rising interest rates and structural change, a more active asset management strategy is needed.

For the last decade, the markets have been operating in an environment of low interest rates, with UK gilt yields suppressed to a level where the risk premium for real estate was historically high. During this time, investors justified increased allocations to property – and other real assets – on account of its “bond-like” characteristics but higher relative income yields.

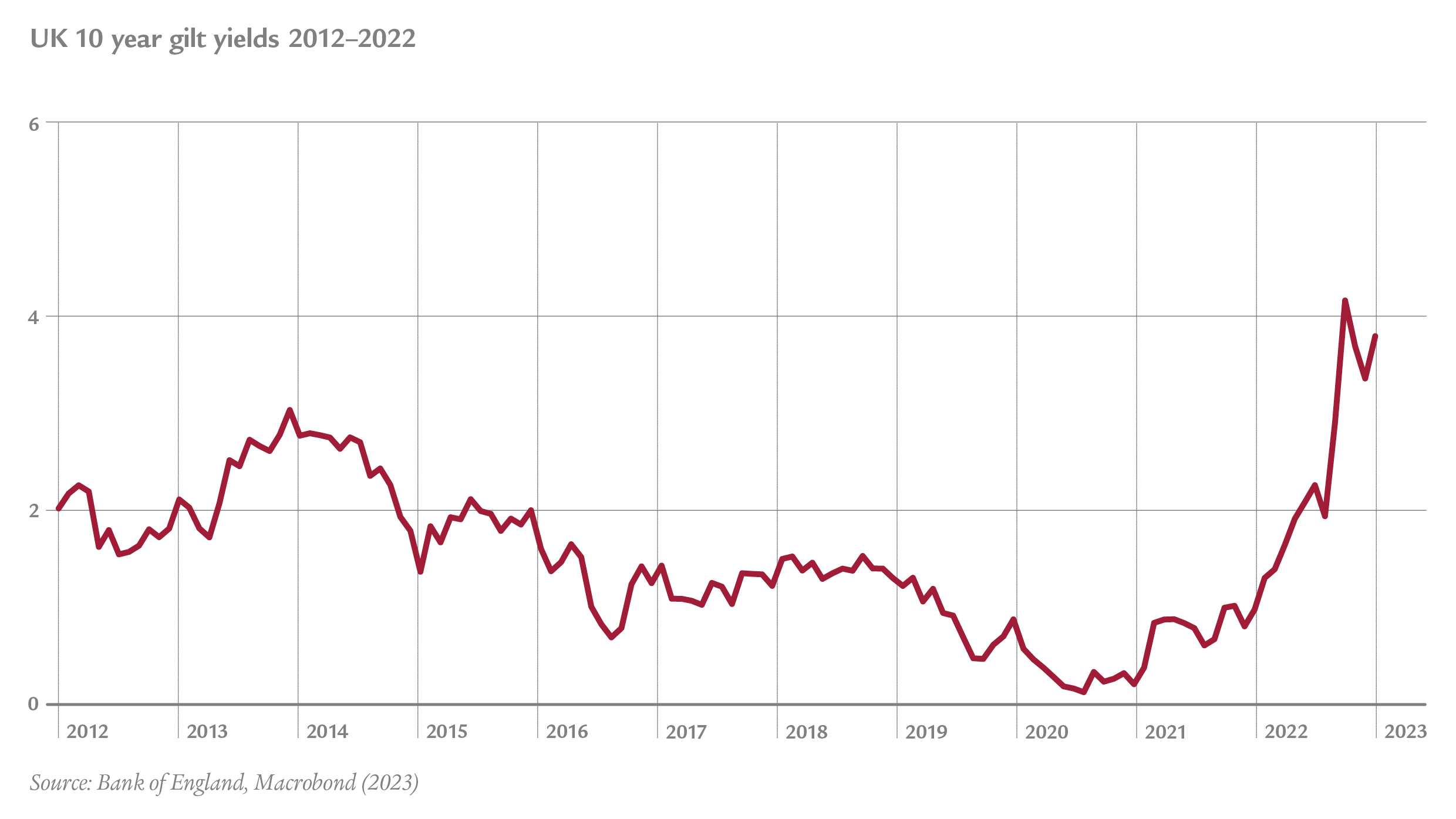

UK 10 year gilt yields 2012 - 2022

UK 10 year gilt yields have risen sharply over 2022

UK real estate reacts to macro-economic conditions

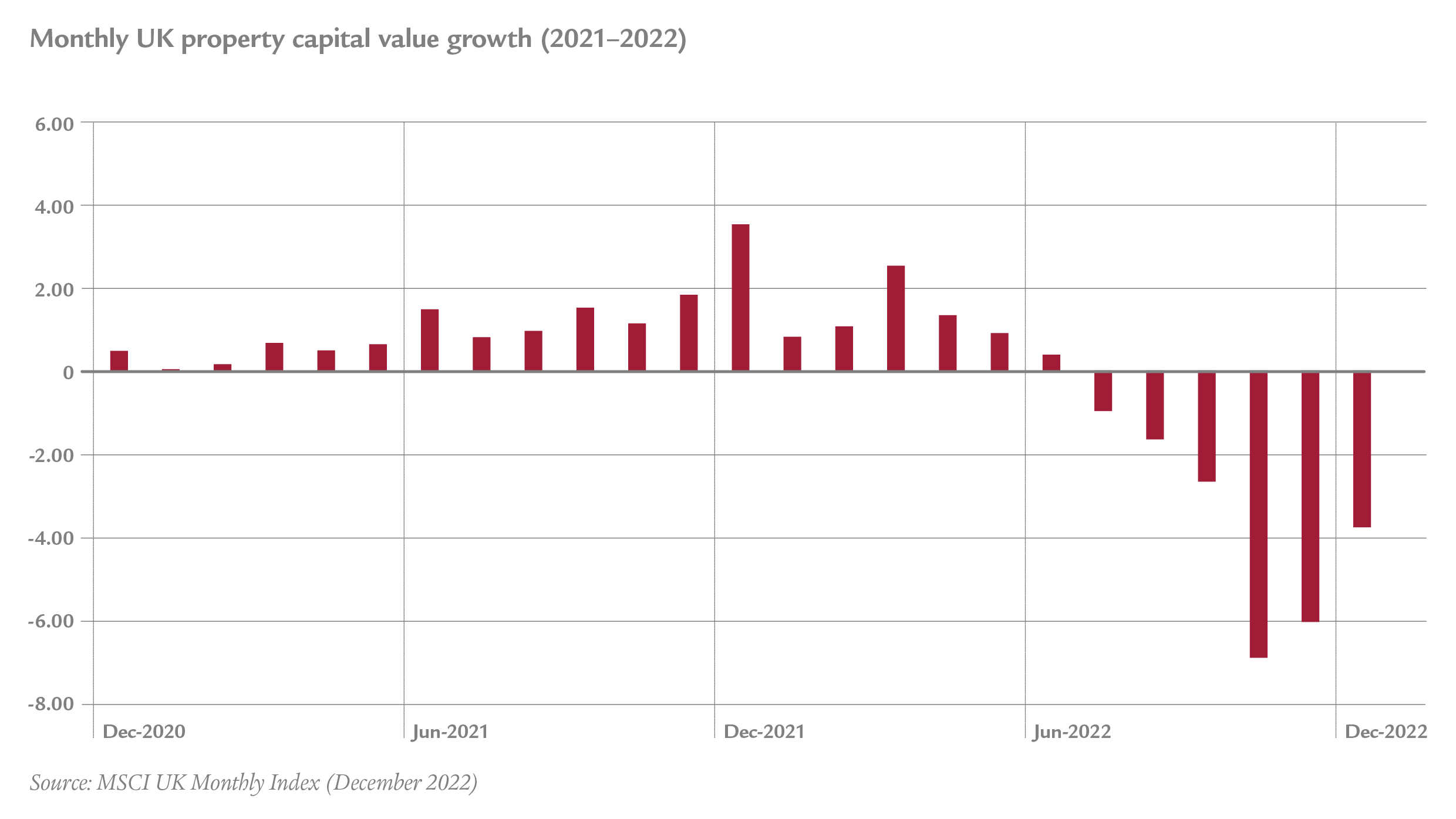

Recent macro-economic developments have caused a shift in this operating environment. As 10-year gilt yields rose, from 1.01% in January 2022 to 3.80% as at 30 December 2022, it became clear that a correction in property pricing was required to bring the risk premium back to a level closer to the long-run average yield gap. The response from the market has been rapid and capital values fell over the second half of 2022. These falls have been sharper than other markets as the UK market is more dynamic. However, this also means that there is potential for a stronger recovery once the recession and monetary tightening have ended.

Monthly UK property capital value growth (2021-2022)

UK capital values have fallen over the second half of 2022

A new era demands a new approach

As interest rates are expected to move sideways in the coming quarters according to our base case scenario, opportunities are emerging given the shift in pricing. However, in a higher interest rate environment the case for property being a bond proxy is no longer compelling. Consequently, the approach to property investment needs to be reassessed. We question the continued relevance of the passive asset management approach that some managers have followed in the past – pursuing lease length and tenant covenant strength without much attention given to the quality and fundamentals of the property or the long-term resilience of the investment that derives from being positively aligned with structural trends.

In our view, investors need to employ more active strategies that enable them to add value in these times of adverse, market-driven movements and to differentiate the sector from other asset classes. We believe that the following strategies may present interesting opportunities over the next 12 months.

A hands-on operation

Operational real estate is becoming mainstream. In part, this is due to the attractive income profile and strong structural fundamentals within sectors that typically feature an operational model, such as care homes, residential, or self-storage. However, it is increasingly important across all real estate sectors as investment with operational control can allow for a tailored product that is well aligned with the needs of the end user, making the investment more resilient.

There is already evidence of rapid polarisation in rental values between high quality, service-led spaces and secondary, service-bare products. By adopting an operational model, landlords can increase returns by capturing upside through rental premiums from well-run assets, rather than passing this on to an external provider.

“Living wall” at The Bonhill Building, London

Source: Mayfair Capital

Repositioning to align with structural change

Property assets are physical, meaning investors can drive performance through active management strategies. Against a weak economic backdrop, the risks associated with development remain high, and we anticipate that most investors will shift to a risk-off approach and focus on core investments. Consequently, pricing of poorer quality stock requiring capital expenditure is likely to see a deeper correction.

However, in many areas of the market, structural changes in the UK economy have left a severe shortage of modern stock that meets tenants’ evolving needs. The next 12 months may offer opportunities for investors to take advantage of an overcorrection in pricing for more secondary stock, acquiring assets that can be repositioned into product better aligned with changing tenant demands, which should deliver above average rental growth and strong capital uplift.

Going green

Active management strategies for real estate do not only apply to traditional initiatives, such as physical extensions and refurbishments, but also to opportunities to make a positive ESG impact. This can, for example, be by reducing carbon emissions or pursuing a social value strategy that benefits the community in which the asset is located. We anticipate a continued investor focus on the “green” credentials of an investment and on its tangible environmental or social benefits. With this issue increasingly taking centre stage for tenants as well, an active strategy to pursue these improvements is likely to deliver rewards in the form of greater confidence in achieving stronger and more sustainable income growth.