Mid and small caps can deliver higher returns than large-cap stocks. An effective way to maximise potential is to employ multi-factor strategies combined with a quantitative investment approach.

In the context of equity investments, investors often come across the terms “mid cap” and “small cap”, which refer to companies with a moderate and a small market capitalisation respectively. One commonly discussed concept here is the “mid and small cap premium”, which indicates the potentially higher returns that these equity categories can achieve compared to large-cap stocks.

Premium: definition and reasons

The mid and small cap premium refers to the historical observation that equities of companies with a smaller market capitalisation tend to generate higher returns than their larger counterparts. This phenomenon can be explained by several factors:

- Growth potential: Smaller companies often have higher growth potential. They are often in the early stages of development or serve niche markets, which can lead to above-average growth rates.

- Market inefficiencies: Mid-cap and small-cap stocks are often tracked less intensively by analysts than large-cap stocks. This under-analysis can lead to inefficient valuations, which can be exploited by experienced investors or in quantitative models.

- Risk premium: Investments in smaller companies are often associated with higher risks, due to market volatility or limited resources, for example. To compensate for these risks, investors demand higher returns.

Multi-factor strategies and a quantitative investment approach

Combining multi-factor strategies with a quantitative investment approach can further maximise the benefits of these market segments. Multi-factor strategies are based on identifying and combining multiple factors that have historically been associated with above-average returns. Commonly used factors include:

- Value: Equities of companies with a low price-to-earnings (P/E) ratio, price-to-book (P/B) ratio or price-to-sales (P/S) ratio.

- Momentum: Equities that have experienced strong price increases in the past 6 to 12 months.

- Quality: Equities of companies with stable earnings, high profitability and low debt.

A quantitative investment approach uses mathematical models and algorithms as the basis for investment decisions. The advantage of this approach is the high degree of objectivity it offers, as decisions are based on data and clearly defined rules. This minimises subjective influences and ensures consistent application.

In addition, quantitative models are highly efficient as they can analyse large amounts of data and, unlike manual subjective analyses, react to market changes without bias. This reproducibility and reliability of strategies can lead to an improved basis for investment decisions, which can be particularly beneficial in volatile markets. Overall, the quantitative investment approach is a modern and precise method for making informed and efficient investment decisions.

The process for combining multi-factor strategies with a quantitative approach when considering investments in mid-cap and small-cap stocks might look something like this:

- Data analysis: Collect and analyse historical data on the identified factors (value, momentum, quality, etc.).

- Modelling: Develop a quantitative model that weights the selected factors and creates a ranking of the most attractive mid-cap and small-cap stocks.

- Portfolio construction: Build a diversified portfolio based on the modelling results, selecting the best equities from the ranking list.

- Risk management: Implement risk management strategies and regularly review portfolio composition to minimise risks.

- Performance monitoring: Continuously monitor performance and adapt models based on new data and market changes.

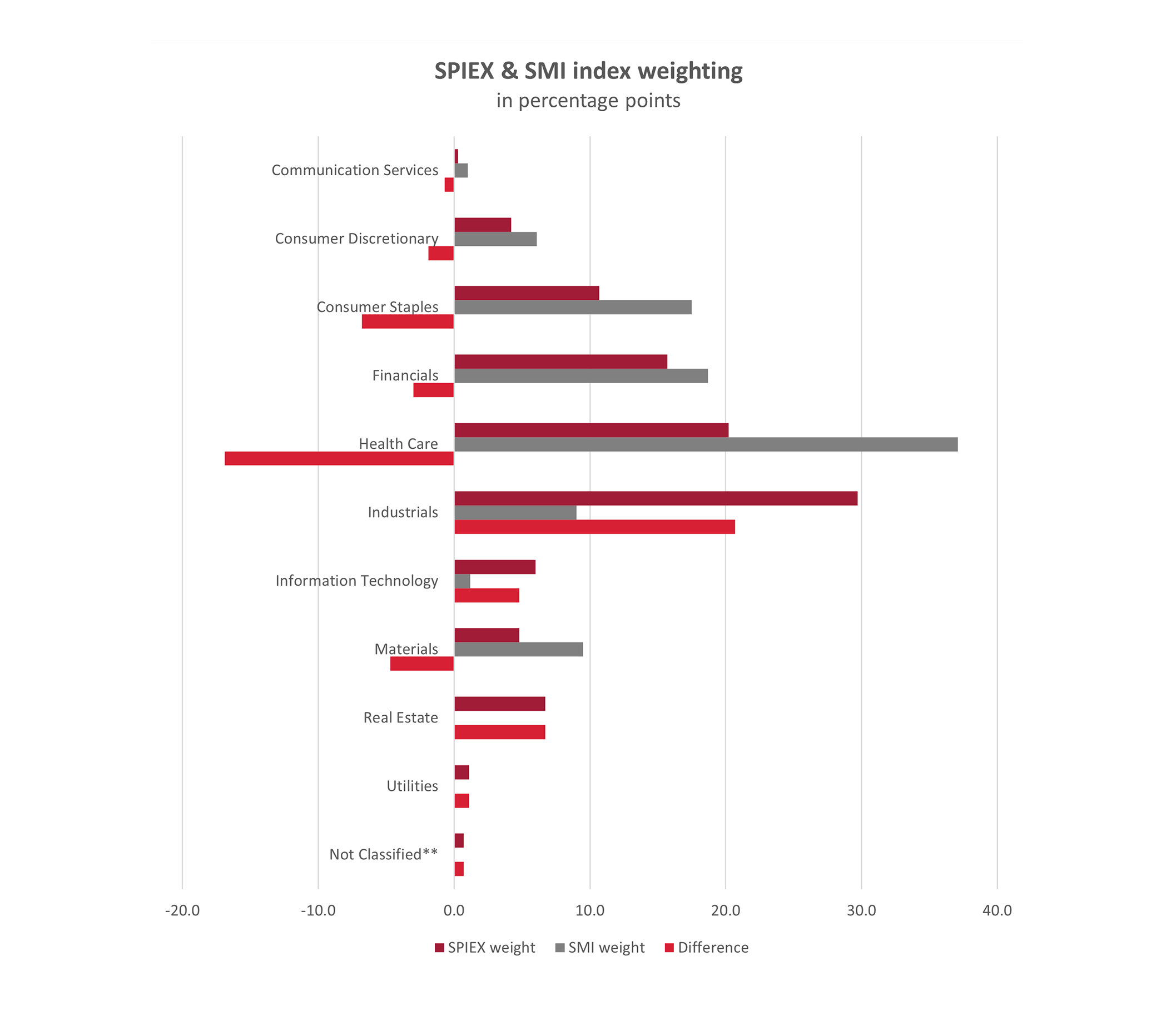

Swiss small caps and the SMI compared

It makes sense to include Swiss small caps for reasons of diversification. As their sector structure differs from that of the Swiss Market Index (SMI), they help reduce that well-known dependence on the SMI heavyweights. In addition, valuations of small and mid caps have become significantly more attractive after years of underperformance against the SMI. These segments can therefore offer attractive return potential in the medium term.

Swiss Life Asset Managers, Bloomberg, 28 June 2024

Conclusion

Swiss Life Asset Managers believes that integrating multi-factor strategies and a quantitative investment approach into mid and small cap investing offers an attractive opportunity to leverage the benefits of these market segments. By combining different factors and using data-driven models, investors can maximise their returns while effectively managing risks. To ensure long-term success, it is vital to implement the process carefully and professionally and continuously review and adapt the strategies. Particularly in Switzerland, it makes sense to include small caps, and the current market environment is favourable.

Swiss Life Asset Managers is a leading asset manager and provider of equity funds – strategically responsible and with consistently solid performance.