As Europe’s population ages, the places where care is delivered – medical centres, assisted living communities, and outpatient clinics – are becoming increasingly relevant. Supported by strong demographic demand, healthcare real estate in Europe is regaining momentum through selective, quality-driven investment and a shift toward more flexible care formats.

Entering 2026, it has become clear that Europe’s healthcare real estate comeback is not market-wide. Instead, it is a moment of choice where quality is rewarded. Transaction activity has picked up comparedto 2024, but – excluding large platform transactions – volumes remain below long-term averages. Pricing discipline, operator quality and regulatory exposure continue to be central themes as investors reassess risk across the sector.

This more cautious environment is also reflected in the way institutional investors are returning. The sector has clearly shifted away from yield-driven strategies towards a stronger focus on operators and scenario-based risk analysis. Properties that demonstrate operational resilience, stable cashflows and alignment with long-term demographic demand are at the centre of investor interest.

Strong demand meets limited supply

Healthcare real estate is no longer perceived as a niche, but as part of the broader living investment universe. Around one quarter of institutional investors are showing interest in allocating capital to the

sector. This elevated demand contrasts with the limited availability of investment-grade assets. As a

result, pricing remains disciplined for high-quality properties, while acquisition processes are

characterised by extended due diligence and selectivity.

Nursing homes continue to represent the sector’s core liquidity pool, but investors have become more cautious. Greater attention is being paid to who operates the asset, the stability of the operator, the

ability to absorb rising costs over time, and potential future capital expenditure requirements. Assets

lacking operational resilience are facing longer marketing and extended closing timelines.

Capital shifts towards lower-risk care formats

Across Europe, investment activity is gradually shifting towards care formats with lower regulatory risk

and less reliance on a single tenant or operator. Assisted living, in particular, has emerged as one of the

most dynamic healthcare segments. This is supported by scalable concepts, growing demand from an

ageing yet still largely independent population, and comparatively lower regulatory exposure.

Medical office and outpatient care formats are also attracting increasing interest. These assets benefit

from predictable cashflows, diversified occupier services and lower dependency on public reimbursement systems than inpatient care. The steady growth in transactions within this segment points to a structural change in investor preferences.

Demographic tailwinds remain intact

Demographic trends remain the most consistent long-term driver of healthcare real estate. Europe’s population is ageing rapidly, with strong projected growth in the 75+ and 80+ age groups across major markets. Life expectancy continues to rise, supporting sustained demand for healthcare services and appropriate real estate solutions.

At the same time, care preferences are evolving. Ageing populations increasingly favour outpatient care, assisted living and medical service formats over traditional institutional nursing care. This shift reinforces demand for adaptable, service-oriented healthcare properties.

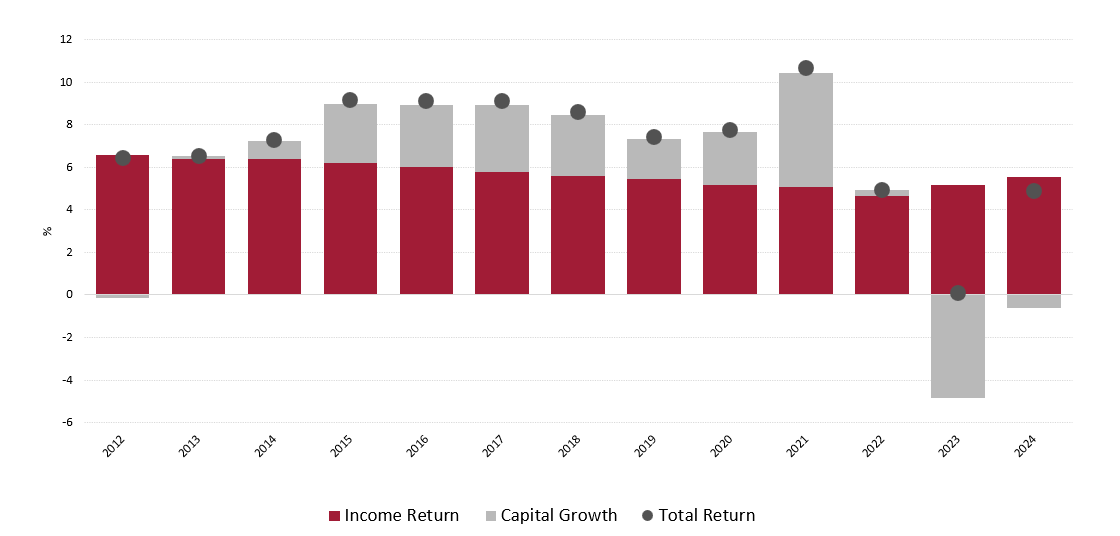

A resilient risk-return profile over time

European healthcare real estate has delivered stable income returns over the past decade. They

have remained positive even during periods of macroeconomic volatility, underlining the defensive

characteristics of the sector. Over the same period, healthcare has outperformed living and office

assets in terms of income returns while maintaining a comparable risk profile.

On a total return basis, European healthcare real estate achieved average annual returns of around six to eight percent p.a. over the past decade, with comparatively lower volatility than the office or residential sector, reinforcing its role as a durable, income-oriented allocation within diversified portfolios.

European healthcare real estate has delivered stable returns

Source: MSCI, 2024 latest available data point

Strategic implications for investors:

- European healthcare strategies are increasingly focused on outpatient, medical office and assisted living formats.

- Nursing homes remain investable but require strict selectivity, focusing on strong operators, transparent cost structures and manageable refurbishment needs.

- Given current construction costs and regulatory constraints, acquisitions offer more attractive near-term risk-adjusted returns than development. Despite favourable demographic tailwinds, successful healthcare investments require precision, operational insight and active asset management.

- Selectivity, local market expertise and operator engagement will remain key success factors in 2026 and beyond.

Find out more about healthcare real estate

Demographic trend provides impetus in the healthcare sector

Demand for healthcare properties in Europe is growing in line with demographic trends. Innovative forms of housing and adaptive care facilities are in demand. Despite temporary challenges, the healthcare sector is proving resilient and keen to invest.

Swiss Life Asset Managers has a long investment horizon in reale estate and combines industry knowledge with reliability and sustainability.